Retail sales of plant-based food in Europe grew by 2% in 2024, thanks in large part to inexpensive private-label offerings from supermarkets.

Over the last year, a wave of retailers in Europe has pledged to increase the share of plant proteins sold in their stores. To do so, some have fine-tuned their lineups to meet consumer preferences, some have put meat alternatives in the meat section, and some have slashed prices to make them cheaper than animal proteins.

The impact has been tangible. The double-digit growth in low-cost vegan food from supermarkets’ private labels has spurred the category’s rise in several key European markets, Circana data released by the Good Food Institute (GFI) Europe shows.

Value sales of six categories reached €4.7B in the region’s six largest markets in 2024, up slightly by 1.7% from 2023. Meanwhile, volumes rose by 4.5% and units by 4.3% year-on-year.

Own-label products drove volume growth in Germany, Italy, France and Spain between 2022 and 2024. That said, people in the UK still exhibited an affinity for branded products, and their counterparts in the Netherlands embraced meat alternatives that could be added to existing recipes, despite a drop in volumes.

“It’s great to see that Europe’s plant-based retail market remains resilient, with increasing sales volumes across four major countries last year. These foods are becoming ever more mainstream as retailers invest in more affordable products,” said Helen Breewood, senior market and consumer insights manager at GFI Europe. “However, the ongoing success of more expensive products in some categories shows that price is not the only factor.”

Here’s a country-by-country breakdown of plant-based sales in European retail.

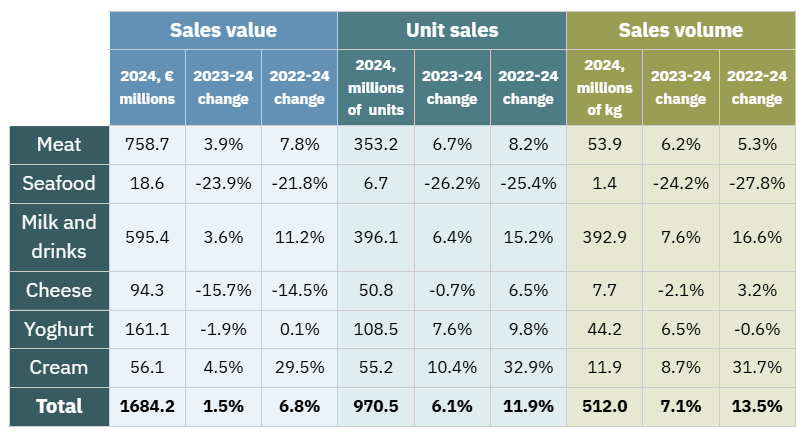

Germany benefits from price parity

In Europe’s largest market, value sales of plant-based food grew by 1.5% in 2024, reaching €1.68B. This levelling off reflects falling prices, given that sales volume was up by 7% during the same period. Germany also had the highest per capita spend (€19.92) in 2024.

The country saw sales rise across meat analogues (4%), plant-based milk (3.5%), and non-dairy cream (3.5%), though seafood (-24%) and cheese (-16%) suffered from major declines.

The overall performance was a result of the lower prices of plant-based alternatives, with many dairy-free milks now on par with cow’s milk, and vegan cream 5% cheaper than the conventional version.

This itself is driven by private-label offerings: Lidl spearheaded the shift by achieving price parity for its Vemondo line. While sales of branded products fell by 0.4% in 2024, private-label offerings witnessed a 5.5% hike.

Further, 37% of German households bought plant-based milk at least once last year, and 32% purchased a meat alternative, in line with the previous two years.

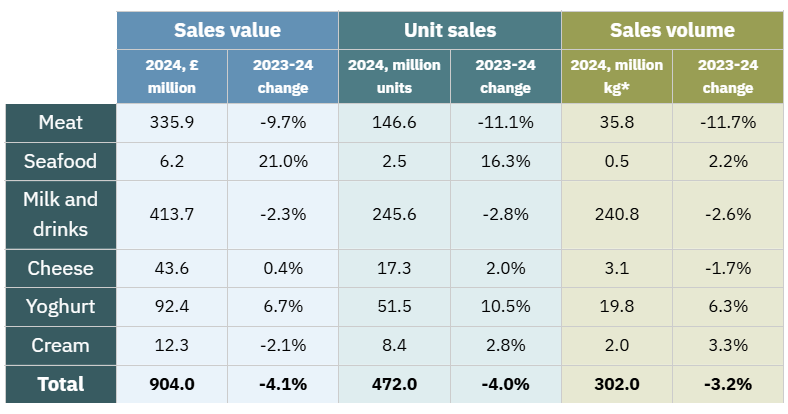

UK embraces tofu over veggie burgers

Despite a 4% drop in sales and a 3% dip in volumes, the UK held its position as the second-largest plant-based market in Europe with a value of €1.07B.

Even though they’re more expensive, branded products were more resilient than private-label options: sales of the former declined by 3%, compared to a 12% decline for the latter. Several innovative companies bucked the trend with significant growth. This suggests that Brits value taste and quality more than price (which is still critical), and may point to the need for better own-label vegan products.

The sales value of meat alternatives fell hard (-10%), with household penetration dropping by four percentage points (reaching 31.5%). Still, their volumes were five times higher than that of veggie burgers, showing the “continued importance to consumers of alternatives that look, taste and cook like meat”, GFI Europe said.

Separately, the volume of tofu sold was 10% higher in January 2025 than 12 months prior, possibly due to its affordability and tempeh and seitan also enjoyed an 85% hike (albeit from a tiny base). In the ensuing months, products like Oh So Wholesome’s Veg’chop and This’s Super Superfood have rolled out in a bid to rival both meat analogues and tofu.

“The relative performance of these foods in percentage terms may be a response to widespread media concern over ultra-processed foods in the UK, although the absolute increase in uptake of tofu, tempeh and seitan was far smaller than the corresponding drop in plant-based meat sales,” the report noted.

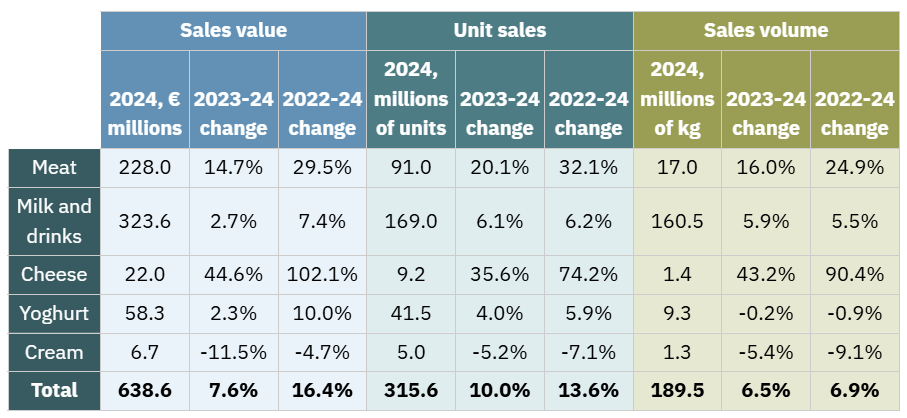

Italy goes big on vegan cheese

In the home of mozzarella and parmesan, sales of plant-based cheese doubled between 2022 and 2024, thanks to a rise in branded products.

It wasn’t just cheese that witnessed growth. Three other categories performed better in 2024 than the year before: meat analogues (a 15% growth), milk (3%), and yoghurt (2%). The overall market was valued at €639M, with only plant-based cream suffering a drop in sales.

That being said, vegan cheese was an outlier, as high inflation in Italy’s food sector led to a strong growth of affordable private-label plant-based products, whose sales were up by 16% last year. In comparison, sales of branded offerings grew more modestly, at 3.5%.

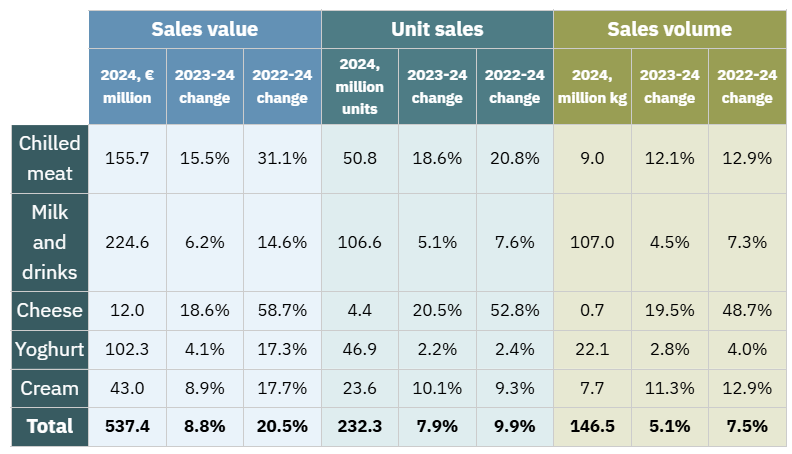

France happy to spend on better-tasting brands

The country that lost its attempt to restrict the use of terms like ‘veggie burger’ saw growth in all five plant-based categories analysed by GFI Europe, led by cheese (19%) and chilled meat (15.5%). The overall market recorded €537M in sales, a 9% increase from 2023.

Private-label products dominated the growth with an 11% hike in sales value, compared to an 8% rise for branded offerings. Supermarket ranges were particularly important for plant-based milk, the largest segment in the country.

Own-label brands were particularly important in the plant-based milk and drinks category, overtaking the sales of branded options and undercutting their price by 30% on average.

At the same time, the relatively expensive branded products gained market share in the vegan meat and yoghurt segments, and made up the majority of sales for plant-based cheese. This suggests that consumers are strongly driven by the taste and quality of animal-free products, not just their cost.

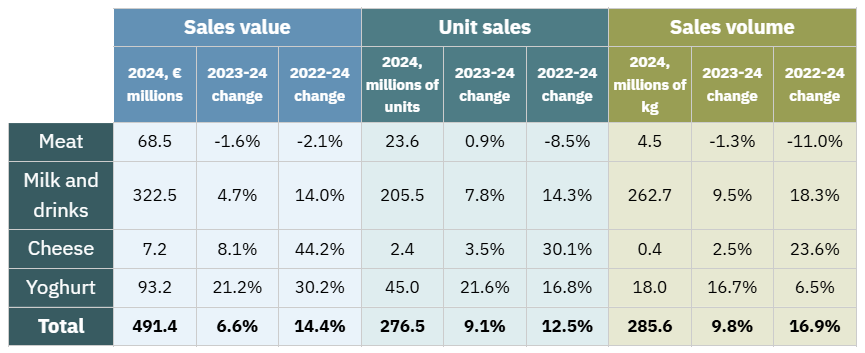

Spain increased adoption of plant-based milk

Plant-based meat was the only category that underperformed in Spain last year, where overall sales of vegan food grew by 6.5% to reach €491M. Still, meat analogues only fell by 1.5%. On the other hand, plant-based yoghurt enjoyed a 21% increase in value sales, cheese grew by 8%, and milk by 5%.

Plant-based milk, in particular, has made major strides, making up nearly 10% of all milk sold in Spain in 2024. Household penetration climbed from 42% to 46% between 2022 and 2024. The success is down to the cost reductions achieved by milk alternatives, thanks in large part to cheaper private-label options.

When looking at sales value alone, the gulf between the sales growth in own-label (5%) and branded products (8%) isn’t that high, but volume sales show a different picture. In terms of weight, plant-based items sold 3% more in Spanish supermarkets last year and private-label products shot up by 13%.

Netherlands chooses pieces over whole cuts

The Netherlands was the only other market apart from the UK that suffered a decline in overall sales of plant-based food in 2024, which plunged by 6% to reach €288M.

This was punctuated by a decline in value sales across all categories analysed, with meat analogues hit hardest (-7%), followed by cheese (6%) and milk (5.5%). Still, the Dutch spent more per person (€15.78) than all countries bar Germany.

According to GFI Europe, the 6% fall in volume sales of plant-based milk stemmed from significantly lower sales of chilled options – sales of ambient versions were stable. This is due to a rise in prices of chilled milk alternatives, against a levelling off of shelf-stable product prices.

Centre-of-plate meat alternatives like burgers and fillets suffered from a decline, but products more likely to be used as part of home-cooked recipes (like mince or strips) remained relatively resilient.

“There is a huge potential market for sustainable and healthy plant-based foods, and companies have a real opportunity to reach more people by developing tastier, nutritious and affordable products that can fit into their lifestyles,” said Breewood.

The post Cheap Private-Label Products Drive 2% Growth of Plant-Based Sales in Europe appeared first on Green Queen.

This post was originally published on Green Queen.