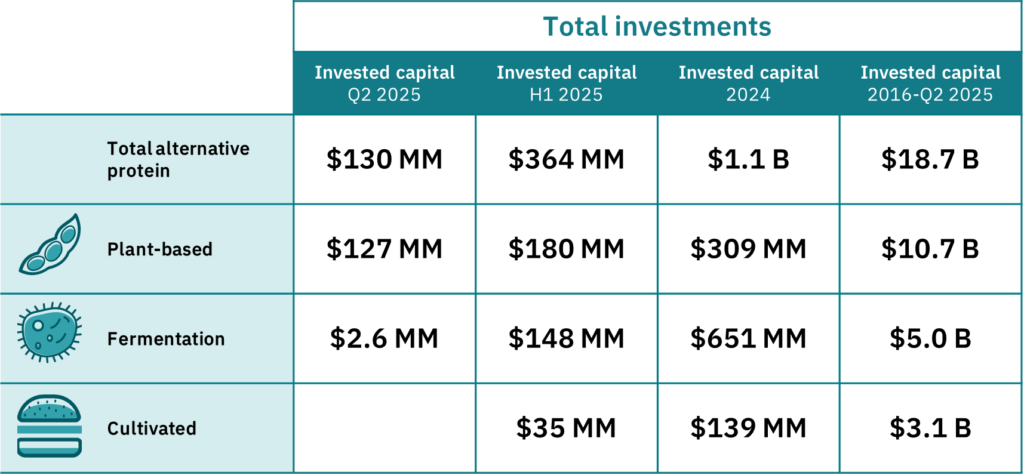

Investment in plant-based, fermentation-derived and cultivated proteins declined by half in the first six months of 2025, outlining continued headwinds for the sector.

Alternative proteins haven’t had the same pull with investors as they did at the turn of the decade, and the consistent downturn in funding has reached a new low in 2025.

In the first six months of this year, funding for plant-based, fermentation-derived and cultivated proteins fell by 49% compared to the same period in 2024, according to the Good Food Institute’s (GFI) analysis of data from Net Zero Insights.

This is after alternative protein companies raised just $129.5M in Q2, a 45% decline from the previous quarter. It took total funding for the first half of 2025 to $364M.

Unlike recent quarters, where fermentation companies have gone the opposite way of the otherwise declining trend, they only raised $2.6M in Q2 (down from $146M in Q1). And while there were three investments announced for cultivated meat, the amount of each deal remained undisclosed.

Plant-based food companies received $127M in the April to June period. However, a large chunk of that was thanks to Beyond‘s $100M debt financing deal. Without this, the plant-based category would have received just half of its Q1 total in this period.

AI a threat and an opportunity for alternative protein funding

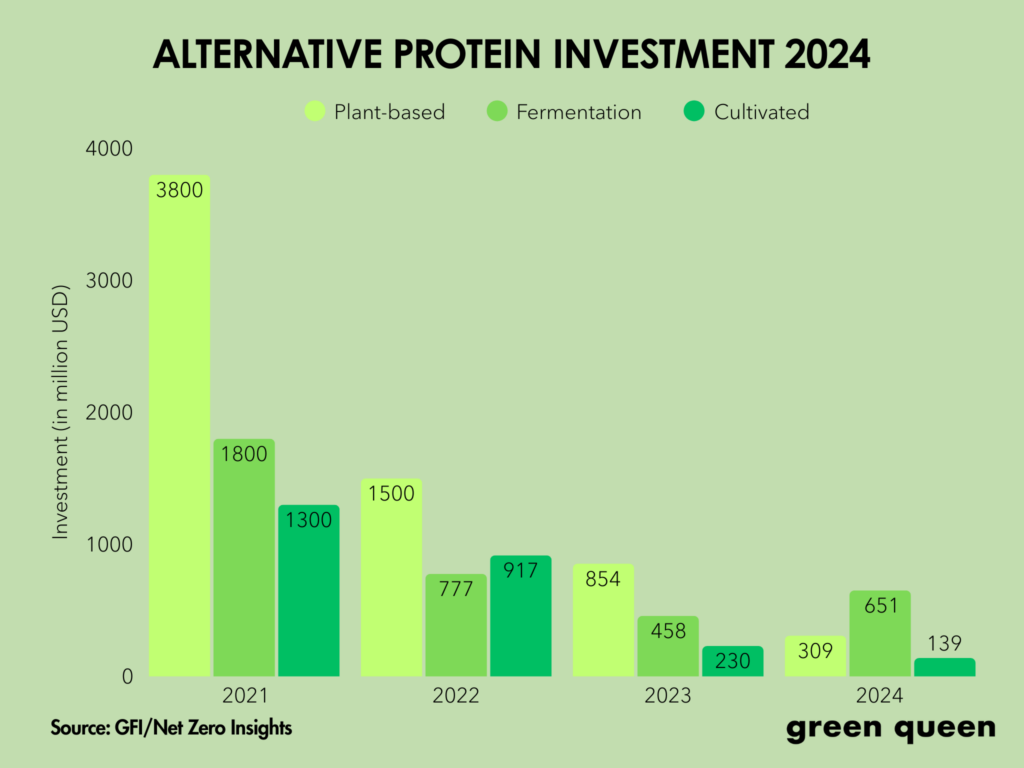

For context, investment in the future food sector has been slowing for a few years now. After attracting nearly $7B in 2021, there has been a constant drop, to $3.2B in 2022, $1.5B in 2023, and $1.1B in 2024.

The trend was already worsening in Q1 2025, when alternative protein investments declined by 28% year-on-year. But the subsequent performance in Q2 has left more questions for the sector for the rest of the year.

VCs, in general, are a conscious class right now. It’s not just this sector that has seen a downward trend in funding, agrifood tech (a 37% year-on-year decline), biotech (-35%) and climate tech (-19%) have all suffered similarly.

With alternative proteins, the hesitance in investing stems from a range of factors, including geopolitical uncertainties, President Donald Trump’s tariff war, Robert F Kennedy Jr’s MAHA policies, the constant attacks on ultra-processed food, legislative bans on cultivated meat, and a resurgence of animal proteins amid continued sales declines for plant-based proteins in several markets.

“Recent investment levels in alternative proteins reflect a market-wide slowdown in food and climate tech funding, driven in part by the reallocation of investor capital toward artificial intelligence,” Daniel Gertner, GFI’s lead economic and industry analyst, told Green Queen.

“These conditions present headwinds for alternative protein startups seeking to raise capital. Topline investment totals fluctuate from quarter to quarter, but the broader trend points to a more cautious capital environment in the near term,” he added.

Like in 2024, there’s one area that has dominated the share of investment and presented additional headwinds for food tech: artificial intelligence. These companies received 53% of all venture capital flows in the first half of this year.

That said, the tech is driving innovations within the alternative protein industry. Companies and researchers are using it to discover ingredients, optimise processes and develop better products.

So for alternative proteins to keep investor interest piqued, a focus on using AI for practical and industrial applications may be the best way forward for now.

De-risking events could usher in more renewed investor interest

Despite the doom and gloom, there were some signs of progress, according to GFI. At least five M&A deals took place in Q2, while partnership activity remained robust. Businesses have been looking to consolidate or collaborate to share costs, strengthen distribution networks, and accelerate regulatory pathways.

Speaking of which, it has been a milestone year for cultivated meat and seafood regulation. In Q2, US startups Mission Barns and Wildtype received the green light from the FDA, with the latter’s salmon going on sale since it doesn’t require USDA approval. Sydney startup Vow, meanwhile, gained final authorisation in Australia and New Zealand, and began selling its cultured quail in the former’s restaurants.

This month, Mission Barns obtained USDA approval, clearing the way for market entry, while Israel’s Believer Meats got the FDA nod for its cultivated chicken. And Friends & Family Pet Food Company secured clearance to sell cultivated chicken for cats and dogs in Singapore.

Public investment is also on the rise. The EU announced €350M in funding to scale up biomanufacturing, which could advance the fermentation sector and support the development of sustainable food ingredients. That said, a recent report showed that the fermentation industry needs $500B to meet its true potential.

According to GFI, companies would need to deliver commercialised technologies and successful exits to kickstart a sustained turnaround in funding. But the increase in strategic deals and regulatory wins could be early signs of a resurgence in investment.

“Several de-risking developments have occurred in recent months, including regulatory approvals for multiple cultivated meat companies and growing momentum in mergers, acquisitions, and strategic partnerships,” Gertner said.

“While still early, these developments may help lay the groundwork for a more favourable investment climate and renewed investor interest in the months ahead.”

The post Alternative Protein Funding Down by 50% in the First Half of 2025 appeared first on Green Queen.

This post was originally published on Green Queen.