TAIPEI, Taiwan – Hong Kong plans to eliminate 10,000 civil service jobs and freeze public sector salaries as part of an effort to curb a growing fiscal deficit, its top finance official announced on Wednesday, as the city grapples with its third year of budget shortfalls.

Hong Kong’s deficit for the fiscal year ending in March 2025 stands at an estimated HK$87.2 billion (US$11.2 billion), following deficits of HK$122 billion in 2022/23 and HK$101.6 billion the previous year.

Hong Kong Financial Secretary Paul Chan outlined in his 2025 budget speech on Wednesday measures to address the financial challenges, including a 7% reduction in government spending over the next three years.

As part of the initiative, the government will cut 10,000 civil service positions by April 2027, representing a 2% workforce reduction per year over the next two years, said Chan.

“The spending cut will establish a sustainable fiscal foundation for future development,” said Chan. “It provides a clear pathway toward restoring fiscal balance in the operating account in a planned and progressive manner.”

Chan added he had also instructed all government bureaus and departments to reassess resource allocation and work priorities. He emphasized the need for streamlining procedures, consolidating resources and leveraging technology to deliver public services more effectively.

Challenges after National Security Law

Since the introduction of a National Security Law in 2020, in response to sometimes violent pro-democracy protests the year before, Hong Kong’s economy has faced mounting challenges, including U.S. and Western sanctions, capital outflows, and shifts in investor confidence.

Gross domestic product contracted by 6.1% in 2020 before rebounding to 6.4% in 2021, but growth has since slowed to 3.2% in 2023 and 2.5% in 2024.

The real estate sector has been hit hard, with property prices dropping nearly 30%, significantly reducing government revenue from land sales, which once contributed over 20% but now make up only about 5%.

The city’s financial sector has remained a cornerstone of its economy, attracting Chinese company listings.

In 2024, funds raised through initial public offerings, or IPOs, in Hong Kong more than doubled in the first three quarters, despite a global downturn in IPO activity. This surge is attributed to market efficiency improvements and enhanced access to mainland financial markets.

However, the landscape has shifted, with multinationals increasingly reconsidering their presence in the city. Western banks play a diminished role in major IPOs, leading to layoffs and a strategic pivot towards wealth management over investment banking – a trend reflecting Hong Kong’s closer alignment with Beijing and a retreat of Western financial players.

The retail and tourism sectors, once vital to the city’s economy, have faced significant challenges due to pandemic restrictions and a decline in mainland Chinese visitors.

In November 2024, retail sales fell by 7.3% year-on-year, marking the ninth consecutive month of decline. Notably, 53% of mainland visitors were day-trippers, spending about HK$1,400 each – 42% less than in 2018.

Edited by Mike Firn.

This content originally appeared on Radio Free Asia and was authored by Taejun Kang for RFA.

Did you know that the government can never run out of money, taxes don’t fund its spending, the national debt isn’t a debt, and printing money doesn’t cause inflation? Probably not, because your parents, teachers, politicians, and favorite journalists have always told you the opposite.

For most of my life, I didn’t know either. I have two PhDs, and if one of them were in economics, it wouldn’t have helped. The only people who know how government finances work are central bankers (who won’t tell you), traders with hands-on experience of the failure of economic norms, and those who stumble across their work (which I explain below).

Everyone else, from New York Times economists to the leaders of both major parties, reinforce common falsehoods, which may be why the economy is brutal and crashes every ten years. Some of these experts lie, others don’t want to rock the boat or jeopardize their careers, but most don’t have a clue.

That is why, if there is a conspiracy to stop us learning “why the government can never go broke,” for example, so that we don’t ask for nice things like public healthcare, climate action, and a basic income, it is almost effortless. Most people automatically treat the government like a big household that is subject to the same financial rules as themselves—balance income with spending, save for a rainy day, and avoid debt.

As responsible adults, that is our lived experience—the hard truth of budget living that accompanies adulthood—and it continues to guide every financial decision we make. When analogized to the government, disagreement appears infantile to us “adults in the room” who assiduously calculate how to pay for government programs with taxes and cuts.

What eventually caused me to stop basing my beliefs on assumptions, hearsay, and intuition were questions like “where does money come from?” And, how did the trillions of dollars that exist today actually get here? My intuition had only supported the ridiculous notion that money is an eternal object that circulates in the economy and cannot be created or destroyed.

In my examination of what seemed like a scholarly question, I discovered what may be the greatest cause of suffering in the developed world— politicians who falsely declare that a government “cannot afford” something or has “reached its debt ceiling” are creating opposition to social spending that would save lives and could save the planet we live on.

The remainder of this article will provide you with the knowledge to reject their misinformation and, I hope, facilitate the greatest societal change of the 21st century.

Where Does Money Come From?

Take the United States as an example. Every U.S. dollar in existence was created by the U.S. government (or by banks with government licenses), and this exclusive right to create the dollar is enshrined in the U.S. Constitution. It is even called a Federal Reserve Note to tell you it was created by the government’s bank.

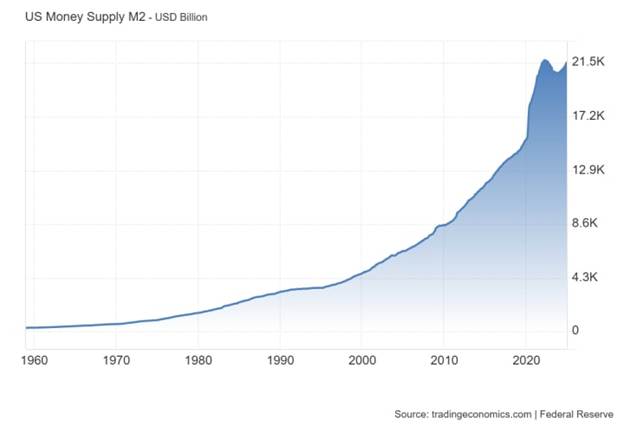

The first dollar was created in 1792 and trillions have been created since then. In fact, there are twice as many dollars in existence today compared to ten years ago (see graph). Although much of the new money is bank credit, the rest is created when the government passes spending bills.

Most national governments are currency issuers, including the U.K., Australia, and Canada, although some are not (e.g., European Union states such as Greece). Localities such as U.S. states also do not create currency and require some form of income.

This power to issue currency means that every statement from a politician, economist, or media personality about the government “running out of money” or being “unable to pay its bills” is a lie.

The Government Can Never Go Broke

In a rare and unreported admission, the Federal Reserve confirmed that the U.S. government issues the dollar and can never run out.

As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. — Federal Reserve Bank of St. Louis

Alan Greenspan also said the following under oath in front of Congress (see video for context).

There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. — Alan Greenspan (Federal Reserve chairman, 1987–2006)

Another Fed chairman, Ben Bernanke, said something similar when he described how the government bailed out the banks after the 2008 financial crisis (see video below). As I said in the introduction, central bankers know how it works. They just almost never tell you.

Taxes Do Not Fund Spending

In the previous video, Bernanke explained that tax money was not used to bail out the banks, and, logically, a currency-issuing government does not need taxes to fund itself.

The proceeds from taxation and bond sales are technically incapable of financing government spending […] modern governments actually finance all of their spending through the direct creation of high-powered money. — Professor Stephanie Kelton

It makes no practical sense for governments to wait until they have accumulated enough in taxes. Or did you think the Treasury was waiting for your grandmother’s taxes to arrive before they could buy a warship?

Rather, they create money as they spend. As Bernanke explained, the government makes a payment by instructing the Federal Reserve to increase the number of dollars in a bank account. This happens by keystrokes on a computer. It doesn’t even need to be printed.

Taxes Are Deleted

There is a veiled admission from the Federal Reserve about the fate of our taxes. Essentially, they acknowledge in footnote 1 here that taxes paid to the U.S. Treasury are no longer part of the money supply (i.e., deleted).

Governments create money by spending and extinguish it via taxation. — Professor James K. Galbraith (former executive director of the Joint Economic Committee of Congress)

Why Tax At All?

Unfortunately, taxation is necessary. When the government creates dollars, it needs you to value and accept those dollars as payment for your goods and labor. The government does this by forcing you to pay taxes only in dollars, which means that you have to obtain dollars from somewhere.

In other words, giving value to the government’s currency is the core reason for taxes, but there are other reasons, such as to reduce the money supply and to punish problematic industries (e.g., polluters). Funding government spending is not one of the reasons. Indeed, governments have to create and spend money before anyone can even pay their taxes.

Printing Money Does Not Cause Inflation

Intuition tells us that creating money reduces its value by the same amount, but this leads to the ridiculous notion that the first dollar ever created was as valuable as the collective trillions in existence today. It also forgets that the money supply is increasing all the time, usually without noticeable inflation.

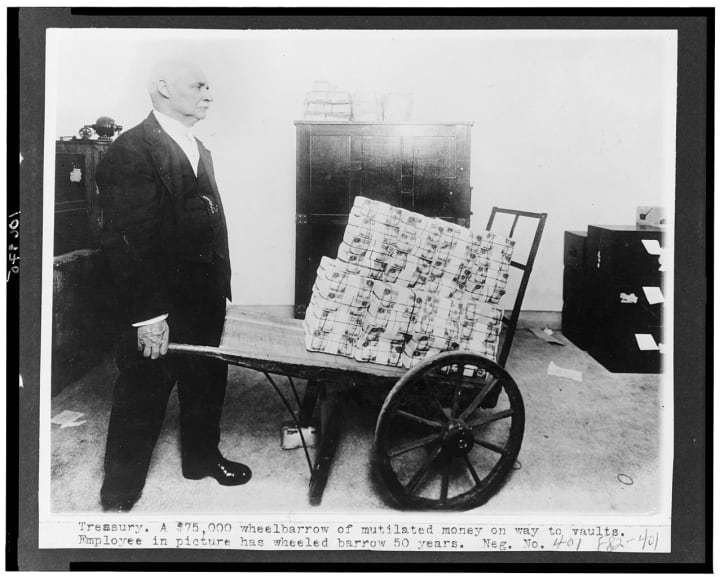

In my case, I held this myopic belief about inflation because I saw a photograph of a wheelbarrow of money in a 7th grade history class about Weimar Germany and I assumed that correlation means causation.

The conventional wisdom that printing money causes inflation is not true. — Professor John T. Harvey

Public domain photo

Although money creation could expedite inflation, it was not the cause of the historical examples that most people cite, such as Weimar Germany and Zimbabwe. Rather, the inflation was caused by supply shortages, or foreign debt, and money was created after to maintain the public sector.

The causation is that inflation increases the nominal need for cash and reserves, not that increased cash causes inflation. — Warren Mosler (hedge fund executive and professor of economics)

We can describe inflation with the equation, MV = Py. While increasing the money supply (M) could increase prices (P), the money may be saved, reducing the rate of spending (V). Alternatively, if the money is spent, businesses will seek to accumulate it by hiring workers and producing more goods and services (y). In either case, prices do not increase.

Inflation can occur if there is a lack of resources or labor, which is why it’s usually a supply issue, and why quintupling the money supply in the past thirty years has not brought about Armageddon.

The National “Debt” Is Not Debt

A national “debt” of more than $35 trillion sounds scary. So scary that people are paid great deals of money to tell you how scary it is. The more afraid you get, the less likely you are to want public healthcare or climate action. How could we possibly afford that?

Much of this “debt” is Treasuries, which are savings accounts with the U.S. government that earn interest. Countries like China and Japan buy Treasuries because they earn dollars through trade and have nowhere better to put them. What this tells us is:

Holders of U.S. “debt” do not want it repaid for the same reason that you don’t want your bank to close your savings account.

The government does not need the money. It creates all that it needs, and it created every dollar that has since been used to buy Treasuries.

If the government wants to eliminate this “debt” it can phase out Treasuries and deposit the money into checking accounts.

If anyone wants to withdraw their money, the government can create/print the withdrawal amount and give it to them (see video).

So the national “debt” is not a debt. When the government creates money, it offers people the chance to buy Treasuries of equal value. These Treasuries, plus cash left in the economy, are the money supply (the total of every budget deficit in history). Eliminating it, such as with less spending and more taxation would eliminate the money supply.

Nevertheless, fear-mongering about the “debt” has persisted for at least 88 years, when it was a thousand times smaller (see video). Normally, when someone predicts the apocalypse, they are discredited when their prediction fails.

Budget Surpluses Cause Recessions

A budget deficit occurs when the government has created and spent more money into the economy than it has removed in taxes. A budget deficit therefore puts more money into your pocket than it takes out.

A budget surplus occurs when more money is taxed out of your pocket than is spent in. This is not good for you, and it doesn’t help the government either because taxes are not saved. But that doesn’t stop corrupt politicians from appealing to popular intuitions about “saving for a rainy day” or the fact that surplus sounds positive and deficit sounds negative.

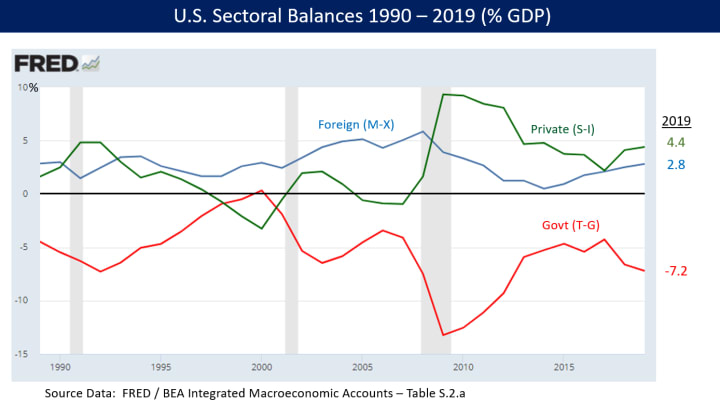

Politicians do this to discourage social spending. Furthermore, attempts to “balance the budget” or have a budget surplus cause cash-strapped people to accumulate private debt (i.e., realdebt) that is held by the wealthy donors of these politicians. Unfortunately, this situation (see graph when the green line drops below zero) almost always triggers a recession (shaded areas of the graph).

Historical data shows that a government deficit (the red line, below zero) is a private sector surplus (the green and blue lines, above zero). Basic accounting tells us that the lines balance out every year and sum to zero.

Why Learning Economics Is Important

Every time a policy is proposed that could save lives, such as public healthcare or climate action, it is belittled with the following eight words: “how are you going to pay for it?”

Liberals propose taxes or cuts that conservatives disagree with, and the two sides have argued about these imaginary financial constraints for decades while millions have died.

The truth is that the government has no financial constraints. It only has resource constraints and the risk that its spending might cause a demand for resources that exceeds the economy’s productive capacity (inflation). However, there is nearly always room to expand that capacity with construction, imports, education, and innovation.

In recent years, Modern Monetary Theory (MMT) and its advocates have popularized and informed people about the ideas presented here. Eventually, these ideas could transform society, causing it to focus less on the importance of money and more on what can be achieved with the real resources at its disposal.

It is no coincidence that every modern historical triumph, from reaching space to winning WW2, acknowledged the triviality of money. We did not say “we can’t afford to fight Germany.” Rather, we looked at what we could do with the resources we had and used money to incentivize people to contribute. A government can create as much incentive as it wants.

In my view, our collective understanding of these paradigm-changing ideas will bring about the greatest societal change of the 21st century. The imaginary financial constraints that our leadership class places upon itself will be removed. Instead of “we can’t afford that” we will say “how do we resource that?” and reduce suffering on a massive scale.

Of course, MMT already has its critics. Typically, they either do not understand the theory or do not want you to understand it. They create straw man versions to make it appear unreasonable, uncomplicated, and not the work of highly-credentialed academics and economists.

For example, you may have heard that MMT is “just about printing money,” that the theory does not consider inflation, or that it can only work while the dollar is the world’s currency (the framework applies to any currency-issuing nation).

Many of these critics have careers or ideologies that have been sustained by their support for economic models that cause a recession every ten years. Other critics have reservations about what will happen to human society if these ideas become popular. Others are wedded to conspiracy theories that impede their ability to process the information.

Dispensing with the intuitive economic falsehoods that you have grown up with should not be entrusted to people whose careers or egos are sustained by them. Rather, MMT should be learned from the academics who developed the theory, such as those listed below.

President Joe Biden’s State of the Union speech failed to discuss a critical matter — the administration’s funding for the upgrading of all three legs of the nuclear weapons triad: Intercontinental Ballistic Missiles (ICBMs), submarines and bomber aircraft. The upgrades, new weapons systems and production of new nuclear warheads are estimated to cost taxpayers over $2 trillion dollars over the…

Question:I heard a news report that the US Government is issuing bonds to finance its budget deficit, and that this will drive up interest rates and might even threaten government solvency. Also I have heard that the US Government has to rely on China to finance our deficit. Isn’t that why the stock and bond markets are bearish?

Answer: This news report reflects two related misunderstandings: first, that government “funds” its deficit by borrowing; second that a large deficit threatens government with insolvency. Let me first deal with those fallacies, then move on to what is happening in markets.

Government spends by crediting bank accounts (bank deposits go up, and their reserves are credited by the Fed). All else equal, this generates excess reserves that are offered in the overnight interbank lending market (fed funds in the US) putting downward pressure on overnight rates. Let me repeat that: government spending pushes interest rates down. When they fall below the target, the Fed sells bonds to drain the excess reserves—pushing the overnight rate back to the target. Continuous budget deficits lead to continuous open market sales, causing the NY Fed to call on the Treasury to soak up reserves through new issues of bonds. The purpose of bond sales by the Fed or Treasury is to substitute interest-earning bonds for undesired reserves—to allow the Fed to hit its interest rate target. (In the old days, these reserves earned no interest; Chairman Bernanke has changed that, effectively eliminating the difference between very short-term Treasuries and bank reserves. It also entirely eliminates the need to issue Treasuries—but that is a topic for another day.) We conclude: government deficits do not exert upward pressure on interest rates—quite the contrary, they put downward pressure that is relieved through bond sales.

On to the question of insolvency. Let me state the conclusion first: a sovereign government that issues its own floating rate currency can never become insolvent in its own currency. (While such a currency is often called “fiat”, that is somewhat misleading for reasons I won’t discuss here—I prefer the term “sovereign currency”.) The US Treasury can always make all payments as they come due—whether it is for spending on goods and services, for social spending, or to meet interest payments on its debt. While analogies to household budgets are often made, these are completely erroneous. I do not know any households that can issue Treasury coins or Federal Reserve Notes (I suppose some try occasionally, but that is dangerously illegal counterfeiting). To be sure, government does not really spend by direct issues of coined nickels. Rather, it spends by crediting bank accounts. It taxes by debiting them. When its credits to bank accounts exceeds its debits to them, we call that a budget deficit. The accounting and operating procedures adopted by the Treasury, the Fed, special deposit banks, and regular banks are complex, but they do not change the principle: government spending is accomplished by crediting bank accounts. Government spending can be too big (beyond full employment), it can misdirect resources, and it can be wasteful or undesirable, but it cannot lead to insolvency.

Constraining government spending by imposing budgets is certainly desirable. We want to know in advance what the government is planning to do, and we want to hold it accountable; a budget is one lever of control. At this point, it is impossible to know how much additional government spending will be required to get us out of this deep recession. Whether the Obama team finally settles on $850 billion worth of useful projects, or $1.5 trillion, voters have the right to expect that the spending is well-planned and that the projects are well-executed. But the budgets ought to be set with regard to results desired and competencies to execute plans—not out of some pre-conceived notion of what is “affordable”. Our federal government can afford anything that is for sale in terms of its own currency. The trick is to ensure that it spends enough to produce sustainable growth and other desired outcomes while at the same time ensuring that its spending does not have undesirable outcomes such as fueling inflation or taking away resources that could be put to better use by the private sector.

Our federal government can afford anything that is for sale in terms of its own currency. The trick is to ensure that it spends enough to produce sustainable growth and other desired outcomes while at the same time ensuring that its spending does not have undesirable outcomes such as fueling inflation or taking away resources that could be put to better use by the private sector.

L. Randall Wray

Why do stock markets and bond markets react the way they do, given that insolvency is out of the question? Sophisticated market players do recognize that government cannot go insolvent and that government will always make all interest payments as they come due. Markets are, however, concerned that all the government spending plus the Fed bail-outs (lending reserves and buying bad assets) will be inflationary. In the current environment, that is quite unlikely. Even if oil prices stabilize at a higher level, that will not compensate for all the deflationary pressures around the world as firms cut prices to maintain sales in the face of plummeting demand. Still, it is not really inflation that bond markets are worried about, but rather future Fed interest rate hikes. (Again, that will not happen in the near future, and might not happen for several years—but there is little doubt that the Fed will eventually raise rates when the economy finally recovers.) Rate hikes lead to capital losses on longer-maturity bonds (interest rates and bond prices always move in the opposite direction). The Treasury persists in issuing bonds with a range of maturities (although the maturity structure in recent years has shortened). This is evidence that the Treasury does not fully understand the purpose of bond sales (since bonds are simply an alternative to bank reserves, it makes most sense to offer only overnight bonds)—but, again, that is a topic for another day.

The Treasury is having some trouble selling the longer maturity bonds (so their price is low and their interest rate is high). China is probably playing a role in this because they are shunning longer maturity debt out of fear of capital losses; they have also shifted some of their portfolio to other currencies (partly to diversify so that they will not lose if the dollar depreciates, and perhaps to pressure US authorities to keep the dollar strong). The solution is that the Treasury should shift even more strongly to shorter maturities—something it will do even if it does not fully understand why it should: Treasury sees that short term interest rates are much lower, hence, will sell short term debt to reduce the “cost of funding the deficit”. If Treasury really understood what it was doing, it would simply offer overnight deposits at the Fed, paying the Fed’s target interest rate. Then it would not “need” to sell bonds at all, and we could stop worrying about government “borrowing from the Chinese”. If the Fed wanted to control interest rates of longer term debt, it can offer interest on deposits of different maturities—for example, it can offer an overnight rate, a 30 day rate, a 90 day rate, and so on, for deposits held at the Fed.

House Republicans unveiled a budget blueprint on Tuesday that proposes trillions of dollars in federal spending reductions over the next decade, specifically targeting Medicaid and federal nutrition assistance for steep cuts. House Budget Committee Republicans’ new resolution also calls for the establishment of a “bipartisan debt commission” to examine and propose changes to “the drivers of U.S.

After threatening to force the government into default over the debt ceiling, Republican lawmakers Friday introduced new tax cuts that could add at least $21 billion to the national deficit over the next decade. Three new GOP-backed bills would cut taxes for large companies, small businesses, and individual families while reducing clean energy tax incentives to pay for it.

It is difficult to believe that our economy can continue to grow robustly as the government sucks disposable income and wealth from the private sector by running surpluses.

“By what process, I wondered, have we convinced ourselves that we do not have enough U.S. Dollars to pay ourselves to create the goods and services we need to prosper as a society?”

Its influence is felt even in liberal or progressive organizations, and among progressive commentators and writers, who all share ideas like fiscal policy discipline and tax reform.

After a week-long scuffle over the House speakership, House Republicans held their first vote with their new majority on a bill to slash over $70 billion for the Internal Revenue Service (IRS) — funding that was pegged to allow the agency to go after wealthy tax cheats. Republicans have specifically targeted the IRS funding that Democrats passed in last year’s Inflation Reduction Act…

Progressive U.S. lawmakers on Monday took House Republicans to task after the Congressional Budget Office said the erstwhile deficit hawks’ first bill before the 118th Congress—a measure critics say is meant to “protect wealthy and corporate tax cheats”—will swell the federal deficit by more than $100 billion.

“They all run on reducing the deficit and now the House GOP’s first… bill will increase the deficit by $114 billion,” tweeted Rep. Ilhan Omar (D-Minn.). “Make it make sense.”

Increasing the federal deficit can help people and the economy. Republicans have been criticized for hypocritically pushing cuts to social safety net programs in the name of fiscal responsibility while being willing to raise the deficit to help corporations and the rich.

The nonpartisan Congressional Budget Office (CBO) estimated that the euphemistically named Family and Small Business Taxpayer Protection Act—which faces a vote as soon as Monday evening—would “decrease outlays by $71 billion and decrease receipts by $186 billion over the 2023-2032 period.”

\u201cThe @HouseGOP preaches about the deficit. Well here’s their first bill \ud83d\udc47https://t.co/OujTofeKS0\u201d

That’s because the legislation would rescind $72 billion of $80 billion worth of new Internal Revenue Service (IRS) funding authorized under the Inflation Reduction Act (IRA) passed by the Demorcat-controlled 117th Congress and signed into law last year by President Joe Biden.

In a December 30 letter to colleagues, House Majority Leader Steve Scalise (R-LA) said the proposed bill “rescinds tens of billions of dollars allocated to the IRS for 87,000 new IRS agents” under the IRA, a GOP talking point that has been widely debunked.

“Today, Republicans in Congress demonstrated their commitment to ‘fiscal responsibility,’” Sen. Elizabeth Warren (D-Mass.) sardonically tweeted. “The first bill advanced by the GOP adds $114 billion to the deficit—by allowing the super-wealthy to cheat their taxes while everyone else pays. Corporate lobbyists are popping champagne.”

Congressional Progressive Caucus Chair Pramila Jayapal (D-Wash.) lamented that the “first order of business in the GOP House of Representatives” will be to “vote to increase the deficit $114 BILLION by letting tax cheats dodge paying what they owe.”

“Once again,” she added, “they’re putting politics over poor and working people.”

Advocacy groups also questioned GOP lawmakers’ motives for introducing the bill, with Americans for Tax Fairness tweeting that “House Republicans are using their new majority to try and repeal IRS funding that will make rich and corporate tax cheats pay what they owe.”

“The GOP wants to let their rich friends keep cheating the rest of us,” the group added.

This post was originally published on Common Dreams.

On the Senate floor on Wednesday, Sen. Bernie Sanders (I-Vermont) had harsh words for fellow members of Congress who have been crafting a bill to give major microchip companies $52 billion in corporate welfare while ignoring pressing issues that are faced by the middle and lower classes in the U.S.

“At a time of massive income and wealth inequality, the American people are sick and tired of the unprecedented level of corporate greed that we are seeing right now,” Sanders said. “In other words, we’re looking at two worlds. People on top never did better. The middle class continuing to decline, and the poor living in abysmal conditions.”

Instead of focusing on things like renewing the expanded child tax credit, passing Medicare for All, upping teacher pay, or making higher education affordable, the Senate is focused on corporate handouts, Sanders said.

“The last poll that I saw had the United States Congress with a 16 percent approval rating, 16 percent. To me, this was shocking — really, quite shocking — because I suspect that the 16 percent who believe that Congress was doing something meaningful really don’t know what’s going on,” he said.

“So what is Congress doing right now, at a time in which we face so many massive problems?” he continued. “The answer is that, for two months, a 107 member conference committee has been meeting behind closed doors to provide over $50 billion in corporate welfare, with no strings attached, to the highly profitable microchip industry.”

Sanders pointed out that the bill also includes a $10 billion “bailout” for Jeff Bezos’s space flight company. The Vermont senator has been decrying this funding for months, saying that Bezos is one of the last people who needs an infusion of cash from taxpayers.

Sanders went on to condemn the glaring hypocrisy of conservatives like Sen. Joe Manchin (D-West Virginia), who cry endlessly about the deficit when it comes to helping the American public, but pass massive spending bills for corporations with no questions asked.

“For all of my colleagues who tell us how deeply, deeply concerned they are about the deficit… ‘Bernie, we don’t have the money to do that! We’ve got a big deficit!’ Well, what about the deficit when it comes to giving $52 billion in corporate welfare to some of the most profitable corporations in America?” he said. “I guess when you’re giving corporate welfare to big and powerful interests, the deficit no longer matters.”

While Sanders acknowledged that the microchip shortage — which is raising prices and costing workers their jobs, he said — does pose problems for regular Americans, he maintained that handing corporations money with no strings attached isn’t the way to solve it.

Semiconductor companies have made huge profits over the pandemic and are turning around to pay their executives massive compensation packages and spend tens of billions on stock buybacks — all while shipping manufacturing jobs abroad to exploit workers in poor countries. Instead of focusing on upping production and preserving jobs, the semiconductor industry is shutting down over 780 manufacturing plants in the U.S. and eliminating 150,000 jobs, Sanders said.

For instance, Intel, one of the companies set to benefit from the bill, made nearly $20 billion in profits last year while giving its CEO Pat Gelsinger nearly $180 million. In the meantime, microchip companies have spent $100 million over the past decade in lobbying and campaign contributions — an investment that has evidently paid back in spades.

Sanders suggested that Congress should work with microchip companies to address workers’ and taxpayers’ concerns, instead of giving companies handouts. He also said companies should agree not to outsource jobs, union bust, or do stock buybacks.

As it stands now, with no-strings-attached handouts to corporations, the government is willingly perpetuating “crony capitalism,” he said.

The response to COVID-19 proved that the federal government is far more capable of managing the economy than many people thought. What happens now that Bidenomics faces rising headwinds?

After a press conference held by Sen. Joe Manchin (D-West Virginia) on Monday, Sen. Bernie Sanders (I-Vermont) pointed out that the right-wing Democrat’s grievances against the reconciliation bill are hypocritical and based on pretense.

In the brief press conference, after which he took no questions, Manchin complained about the potential cost of the reconciliation bill, urging his colleagues to postpone consideration of the bill until its impact on the deficit — if any — is scored. “I will not support a reconciliation package that expands social programs and irresponsibly adds to our $29 trillion in national debt,” he said. He also said that the bipartisan infrastructure bill that he helped negotiate should come to a vote soon.

Sanders, who is Senate Budget Committee chair, pointed out to reporters after the conference that Manchin’s own infrastructure bill would add to the national debt. “The infrastructure bill runs up a $250 billion deficit over a 10-year period,” Sanders said, citing the Congressional Budget Office’s estimate that the bill would add $256 billion to the deficit. “It’s not paid for.”

On the other hand, the reconciliation bill is fully paid for, according to legislators’ estimates. “The legislation that I want to see passed, which includes lowering the cost of prescription drugs, expanding Medicare, including paid family and medical leave, is paid for in its entirety,” Sanders said. “It will not have an impact on inflation.”

The latest draft of the reconciliation bill from the White House contains $1.75 trillion in childcare, health care and climate investments. With almost $2 trillion in offsets like a minimum corporate tax and investments in the Internal Revenue Service (IRS) to prevent tax cheating, the government would actually come out ahead.

Ironically, the reconciliation bill is estimated to bank around $250 billion over the next 10 years, which is nearly enough to pay for the deficit that the infrastructure bill would add. The original draft of the bill that Manchin so vehemently opposed, valued at $3.5 trillion, was also fully funded. Of course, Manchin still won’t commit to voting for the Build Back Better Act, despite getting nearly everything he demanded in negotiations.

Rep. Katie Porter (D-California) has condemned Manchin’s opposition to the bill’s price tag, saying, “I think it’s dead-on fiscally irresponsible for Senator Manchin to refuse to raise revenue and at the same time out of the other side of his mouth — maybe the side of his mouth that he uses to talk to his corporate donors — complain that we can’t pay for the things that American families desperately need.”

With the inclusion of key provisions, the reconciliation bill has the potential to be transformative for the country’s social safety net and in reducing carbon emissions — and considering Manchin’s support of other costly proposals, his stance on the bill is hypocritical.

Manchin has voted to approve over $9 trillion in defense spending over the past ten years and is fighting to include at least $121 billion in subsidies for the fossil fuel industry. He’s also opposed key proposals like raising taxes on corporations, a billionaire tax and IRS reform plans, all of which would help offset the cost of the reconciliation bill.

Under his leadership, the bipartisan group that was negotiating the infrastructure bill nixed nearly all of the measures that would have funded the infrastructure bill, leaving half of the new spending unaccounted for.

As some commentators have noted, by focusing on taxation and the deficit, rather than the massively popular and transformative proposals contained in the bill, Manchin has sidestepped having to announce his opposition to many of the bill’s most sought-after proposals.

On Monday, Sen. Joe Manchin (D-West Virginia) held a press conference airing his grievances surrounding negotiations over the reconciliation bill, which he has held hostage for months and successfully slashed in half.

In the conference, the right-wing senator said he wanted the bipartisan infrastructure bill that he worked on to pass immediately, and that he wanted Congress to hold off on moving forward with the reconciliation package. Despite Manchin largely getting his way on the reconciliation bill, cutting it down from what the public, the president, and most of the Democratic caucus wanted, he wouldn’t commit to voting for the bill.

“In my view, this is not how the United States Congress should operate,” Manchin said, adding that “the political games have to stop.” He also said that waiting to pass the bipartisan infrastructure bill until after the reconciliation bill passes the Senate would not sway him toward voting for the reconciliation bill.

Congress has been engaged in months of deadlock over the reconciliation and infrastructure bills that were originally proposed by the White House in the spring — a stalemate that has been driven almost entirely by Manchin.

Thanks to the work of a bipartisan group of senators led partly by Manchin, the infrastructure bill was cut from $2.25 trillion in new spending to a paltry $550 billion. The reconciliation bill, which was originally a $6 trillion bill, then a $3.5 trillion bill, has also been cut down; after fierce months-long negotiations, the latest White House draft has the price tag pegged at $1.75 trillion.

“I will not support a reconciliation package that expands social programs and irresponsibly adds to [the national debt],” the lawmaker said. “Simply put, I will not support a bill that is this consequential without thoroughly understanding the impact that it will have on our national debt.”

Manchin has said that he’s hesitant to vote for the bill when programs like Social Security and Medicare are underfunded — even though he didn’t cosponsor a recent bill that would modernize Social Security and fund the program for longer.

Despite the fact that the bill is now much closer to his preferred price tag of $1.5 trillion than it is to the $6 trillion or $10 trillion that progressives wanted, Manchin complained that his colleagues were not negotiating in good faith. “While I’ve worked hard to find a path to compromise, it’s obvious: compromise is not good enough for a lot of my colleagues in Congress,” he said. “It’s all or nothing. And their position doesn’t seem to change unless we agree to everything.”

Considering that progressive lawmakers have already compromised greatly on their priorities in the course of negotiations, this is perhaps the most ironic statement that the senator could make. While progressive lawmakers have had to compromise down from $8.25 trillion or $4.25 trillion for this new framework, Manchin only has to give up $250 billion — or about $25 billion a year, a mere drop in the bucket for the U.S. government.

Colleagues like Sen. Bernie Sanders (I-Vermont) have condemned Manchin’s opaque negotiating strategy, which has concealed his demands from both colleagues and the public.

Manchin’s statements about his desires for the bill have been riddled with inconsistencies. Though the West Virginia senator seems to be a deficit hawk when it comes to social or climate spending, that’s merely an excuse to work against whatever proposals he or his lobbyist allies want to kill.

After close collaboration with Exxon lobbyists, Manchin has carved crucial climate provisions out of both bills, and has fought to apply means testing to provisions that improve quality of life for everyday people, like the child tax credit — or to cut the programs entirely. He also attempted to add a work requirement for paid leave, even though the person claiming the paid leave would, by definition, have to have a job to take off from in the first place.

Now, the lawmaker is once again suggesting that the reconciliation bill be separated from the infrastructure bill, even though — or perhaps because — progressives have pointed out that delaying the reconciliation bill could lead to its destruction.

Of course, when provisions that Manchin favors have the potential to increase the deficit, he doesn’t say a word.

According to an analysis by the Congressional Budget Office (CBO), the infrastructure bill that Manchin wants to immediately pass would add about $260 billion to the deficit, or about half of the new spending that the bill proposes, an amount that the senator has yet to comment on. He has also opposed popular revenue raisers like raising taxes on the wealthy and corporations through the reconciliation bill, despite the fact that the proposals would raise nearly enough to pay for the entire $3.5 trillion framework.

The West Virginia coal baron has fought hard to include spending on coal and the fossil fuel industry. He recently got a $775 million oil and gas subsidy added to the bill, and has been fighting for at least $121 billion worth of subsidies for the industry — a move that has been praised by the coal industry. “I think the positive news for the people in the coal business, it looks like, Senator Manchin’s been successful [in cutting climate provisions],” a coal producer CEO said last week in an earnings call.

A declaration of war is a legal framework that sets in motion a process of “mobilization” in which the national government directs real resources—labor, engineering expertise, technology, material—toward the goal of defeating an enemy threat.

As amendments to the bipartisan infrastructure bill were being debated in the Senate, the Congressional Budget Office (CBO) said Thursday that only about half of the $550 billion in new spending proposed by the bill will be paid for and the rest will add to the deficit.

The CBO announced that the bill would add about $256 billion to the deficit over the next ten years despite the fact that the bipartisan group working on the bill had promised the entire bill would be paid for.

Republicans have warned for weeks that they may not support the bill if it wasn’t fully funded. Senate Minority Leader Mitch McConnell (R-Kentucky) said in June that might not support a bill that added to the deficit. Sen. Mike Lee (R-Utah) told The Hill on Thursday that, despite the good provisions in the bill, he believes half of the “pay-fors” in the bill are “fake.”

Sen. Rob Portman (R-Ohio) has evidently been warning his colleagues for weeks that the bill would likely not be fully covered. Sen. Kyrsten Sinema (D-Arizona) and Portman circulated a statement saying that the CBO score may not be fully accurate and that the bill would still be fully funded, in an attempt to assuage concerns for now.

Still, Sen. Bill Hagerty (R-Tennessee) is hesitant after the CBO report, falling in step with McConnell’s announcement in June that GOP lawmakers wouldn’t vote for a bill that added to the deficit. A spokesperson for Hagerty told Politico that the senator “cannot in good conscience agree to expedite a process immediately after the CBO confirmed that the bill would add over a quarter of a trillion dollars to the deficit.”

Senators, mostly Republicans, introduced a flurry of amendments on Thursday evening but Hagerty’s opposition held up a vote to end debate. Senate Majority Leader Chuck Schumer (D-New York) has rescheduled the vote for Saturday. The bill must receive at least 60 votes to advance, thanks to the Senate filibuster.

Though Republican opposition to adding to the deficit — and thus potential opposition to the entire infrastructure bill — is unsurprising, it comes after months of negotiations in which the GOP has rejected a wide swath of Democratic proposals that could have prevented any deficit issues at all.

President Joe Biden had originally proposed a modest tax increase on corporations and wealthy people to pay for his $4 trillion package. Republicans categorically rejected this proposal, not wanting to undo Donald Trump’s 2017 tax cuts. Instead, they offered to pay for the bill with user fees, a proposal that Sen. Bernie Sanders (I-Vermont) pointed out was really a tax on the middle and lower classes.

Republicans also rejected a proposal to enforce existing tax law on the rich. This pay-for would fund the Internal Revenue Service (IRS) to go after rich tax dodgers — many who often donate handsomely to the Republican Party. The IRS funding proposal in the bipartisan bill would have raised an estimated $100 billion over 10 years.

The GOP, then, has created its own catch-22 on the infrastructure bill. They won’t agree to a bill that would add to the deficit, but they also won’t agree to any of the pay-fors that would cover additional spending. It’s unclear if Hagerty or other Republicans could be swayed to support the bill — but as Republicans have been delaying the bill for months, Democrats and progressives are growing more impatient.

It has recently been pointed out to me by Karl Polanyi that we live in a market society with little chance we shall ever live in anything else and, as such, whatever we hope to accomplish will have to be accomplished within the framework of market society norms. I take this to mean it will …

The leadership of the Congressional Progressive Caucus iscallingfor permanent repeal of a notorious 2010 law that is threatening to inflict deep, automatic cuts to Medicare and other safety net programs followingpassageof the $1.9 trillion American Rescue Plan earlier this month.

On Friday, the House of Representatives — with the support of just29 Republicans — approved legislation that would exempt the coronavirus relief package from a law known as statutory Paygo, which requires deficit spending to be offset by cuts to government programs. The Statutory Pay-As-You-Go Act wasenactedin 2010 with thesupportof the then-Democratic Congress and former President Barack Obama.

While Paygo rules werewaivedin coronavirus relief bills approved during the Trump presidency, congressional Democrats’ use of the arcanebudget reconciliationprocess to pass the American Rescue Plan over unified Republican obstructionpreventedinclusion of a waiver this time around,setting the stagefor tens of billions of dollars in cuts to Medicare, farm subsidies, and other programs if the Senate fails to act.

“We’re pleased that the House voted today to waive statutory Paygo for the American Rescue Plan Act to prevent damaging, self-defeating, and wholly unnecessary cuts to Medicare and other programs,” Rep. Pramila Jayapal (D-Wash.), chair of the Congressional Progressive Caucus, said in astatement. “We urge the Senate to follow the House’s lead and act swiftly to waive statutory Paygo.”

But Jayapal stressed that the House bill — which alsopushes off a separate 2% cut to Medicareset for April 1 — is just a temporary solution to a problem that will continue cropping up without complete repeal of the 2010 law.

“It’s long past time for Congress to end statutory Paygo permanently,” said Jayapal. “The austerity politics of the last several decades have been an unmitigated failure — hollowing out programs that families rely on and leaving millions unable to afford the basics.”

“Congress should never have to choose between protecting programs like Medicare and lifting families out of poverty or providing urgently needed assistance to working people facing unprecedented economic hardship,” the Washington Democrat continued. “At the Progressive Caucus, we will keep fighting to end statutory Paygo for good so that Congress can focus on what really matters: empowering and investing in working people across this nation.”

While HR 1868 addresses the immediate problem, statutory PAYGO will keep standing in the way of legislation that matches the scale of our national crises.

— Progressive Caucus Action Fund (@WeAct4progress) March 18, 2021

To pass the House legislation, the Senate Democratic caucus will need to win the support of at least 10 Republicans as long as the60-vote legislative filibusterremains intact. But judging by overwhelming opposition to the Paygo waiver bill among House Republicans — 127 membersof the GOP caucus voted no — Senate Democrats could have difficulty obtaining the necessary votes.

A spokesperson for Sen. Bernie Sanders (I-Vt.), chair of the Senate Budget Committee,toldNBC Newslast month that the Vermont senator will work to prevent theestimated $36 billion in Medicare cutsfrom taking effect. A fix must be passed by the end of the year.

“Trump and his Republican colleagues used deficit spending to pass $2 trillion in tax breaks overwhelmingly benefiting the wealthiest and large corporations and expanding a military budget with a Pentagon that has never been independently audited,” then-Sanders spokesperson Keane Bhatt said in February. “When it comes to feeding children who are hungry or treating people who are sick in the middle of a pandemic, funding cuts due to supposed concerns over the deficit would be unacceptable and immoral.”

Rep. John Yarmuth (D-Ky.), chair of the House Budget Committee,notedFriday that Paygo exemptions have in the recent past “been enacted with little dispute,” pointing specifically to the 2017 bipartisan passage of a waiver for Trump and the GOP’s tax cuts, which could have triggered$25 billionin automatic Medicare cuts.

“Enough House and Senate Democrats joined Republicans to prevent harmful across-the-board cuts to critical programs even though we opposed the short-term [government funding resolution in which the Paygo waiver was buried] and the massive tax giveaways to the wealthy,” Yarmuth said on the House floor.

“Even in the wake of contentious legislation,” the Kentucky Democrat continued, “Congress has come together to prevent sequestration and protect Medicare, farm supports, social services, resources for students and individuals with disabilities, and other programs Americans rely on. This time should be no different.”

Rather than bypassing the problem of power by putting our faith in MMT’s printing press, we need a strategy to rebuild the tax state and move toward economic democracy.

A long line of critical fiscal theorists has pointed to the limits of financing a politics of emancipation through levies on a regressive economy. We need to heed their warnings today.

Deficit hawks, like dive-bombing kamikazes, are out now again, circling the battleship of our collective efforts to save ourselves. Can we pay ourselves to produce, distribute, and administer the Covid vaccine to every American in six months? No! say the dive-bombing Kamikazes—we cannot collect enough taxes to pay for that. It would require the government to borrow hundreds of billions more, increasing our “deficit” and the national “debt.” Can we pay ourselves to design and build a low-carbon infrastructure that will help put a cap on global warming? No and No! say the circling deficit hawks—and here we can see clearly: they have been launched into the sky, and are being directed in their dive-bombing formations, by an elite, powerful group of people who are bankrolled by mining carbon (on public lands!) and sending it into the atmosphere. What are we to do about these Kamikaze politicians and pundits who have been sent into formation above our beleaguered battleship? How can we shoot them out of the sky so we can get on with the task of paying ourselves to do what is necessary for our collective wellbeing?

The only ammunition we have is factual truth-telling. We must forcefully call the bluff of their false “reasoning.” It is a falsehood to say that, for lack of tax revenues, we cannot pay ourselves to mobilize 800 million doses of the Covid vaccine—and begin mobilizing a green infrastructure at the same time. It is a falsehood to say that to address these desperate needs of collective society we must raise taxes on people and businesses, or that we must “borrow” from future tax revenues, requiring our grandchildren to pay higher and higher taxes to pay off the “debt.” These falsehoods must be forcefully repudiated by the logic of Modern Monetary Theory.

In my book Paying Ourselves to Save the Planet, there are many diagrams; in particular there are eight diagrams which demonstrate why the claims and admonitions of the deficit Kamikazes are, indeed, as false as they are dangerous to our collective well-being. What is at stake is not some imagined tax-burden for our grandchildren, but the existential quality of our grandchildren’s lives. We must pay ourselves to mobilize and administer the vaccine—and put in place the robust, free-to-the-public healthcare system that our common welfare requires. We must pay ourselves to rapidly begin designing and deploying a green infrastructure that will enable us to control and adapt to climate change. The eight diagrams—which I will now share, along with a narrative explanation—show us why we can afford to pay ourselves to do all these things (and more).

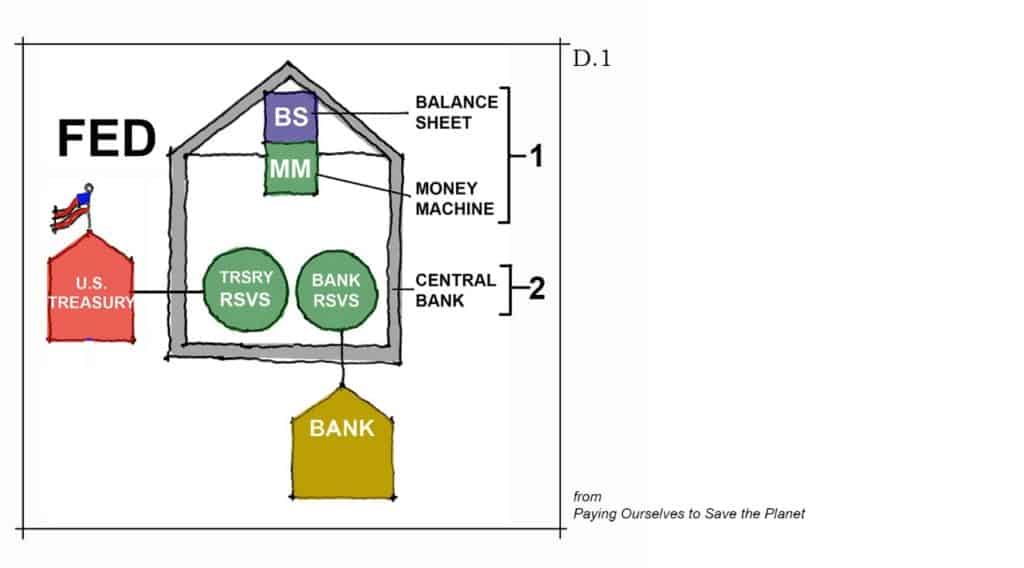

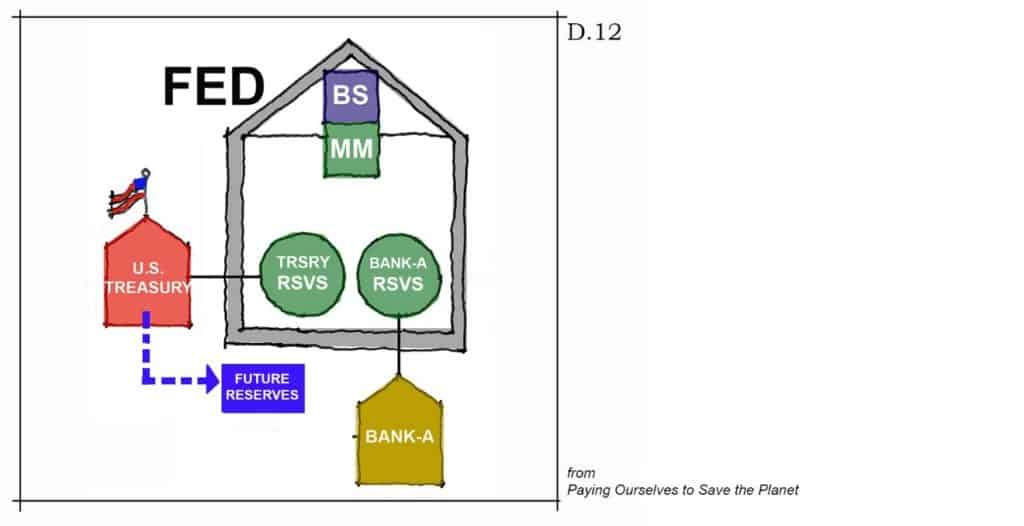

Generating Reserves for Public Enterprise

This is the “master diagram” we will build on. The U.S. central bank (the FED) is the grey house shape. The FED is the official, authorized, issuer of U.S. fiat money (called “Reserves”). The FED issues Reserves in exchange for collateral. Collateral is anything the FED itself decides is of equal value to the Reserves it issues. As illustrated in the diagram, the FED has a balance sheet where it keeps all the collateral it has been given in exchange for the Reserves (U.S. fiat money) it issues, with keystrokes, from its “money machine.” The Reserves it issues are kept in special accounts at the FED itself (the green circles). Each bank in the Reserve system has its own Reserve account at the FED—and the U.S. Treasury also has a Reserve account at the FED.

Up to this point, the book (Paying Ourselves to Save the Planet) has been explaining how Reserves (fiat dollars) are issued for profit-making private enterprise—and the important observation has been made that they cannot be issued unless a profit (or the likely advent of a profit) is involved in the transaction. This fact seems to create the following “reality”:

Fiat dollars (Reserves) to pay people and businesses to undertake not-profit-making enterprises (for the public benefit and well-being) can only be obtained by taxing the profits and wages of private enterprise. This apparent fact seems to put a limit on what public enterprise can do. If, for whatever reason, it becomes necessary for public enterprise to spend more fiat dollars than have been received in taxes, it appears those additional fiat dollars can only be obtained by “borrowing” from the after-tax profits (capital) of private enterprise—creating a “debt” that must subsequently be repaid with future tax revenues (i.e. our grandchildren’s money). These apparent facts are the ammunition of the deficit-hawk kamikazes!

Our ammunition, in return, is the following seven diagrams (building on the first) which demonstrate why the apparent facts, stated above, are false. The Federal Reserve system, it turns out, can and does create new Reserves, as necessary, to support the not-profit-making efforts of public enterprise. As the diagrams will show, it is not necessary to either tax or borrow from the profits and wages of private enterprise to pay ourselves to undertake whatever efforts Congress deems necessary for our collective well-being.

Here is the first step:

The U.S. Treasury issues certificates of future Reserves. These are commonly known as “treasury bonds.” Unfortunately, this is a misleading and confusing name because it incorrectly implies a similarity with a corporate or municipal bond. Any similarity, however, is profoundly superficial for the simple reason that the redemption of both corporate and municipal bonds depends on future corporate or municipal revenues (profits or local taxes on profits)—revenues which may, or may not, be forthcoming. U.S. Treasury future Reserve certificates, in contrast, do not require future revenues for redemption (as we will see) but only keystrokes by the Federal Reserve to create new Reserves when the certificates come due—an act which will always be forthcoming so long as the United States is a viable, sovereign, constitutional democracy.

Here is step two:

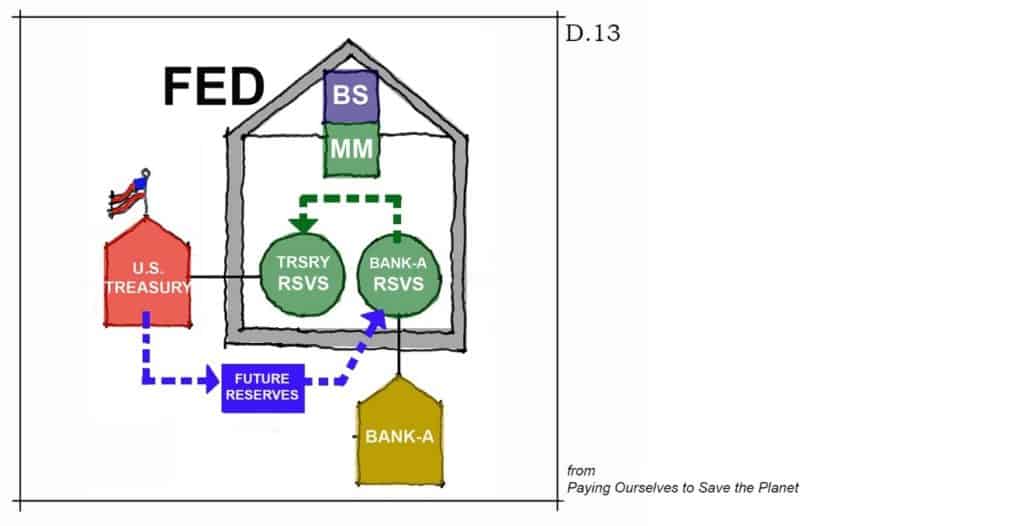

The Treasury trades its future Reserve certificates for existing Reserves in one of the Reserve accounts at the FED. The private businesses, banks, trust-funds, or people who own the existing Reserves (or claims on them) are happy to accommodate this transaction because they get more future Reserves than they give the Treasury in trade—and because this profit is made (unlike most of their other profits) with virtually zero risk.

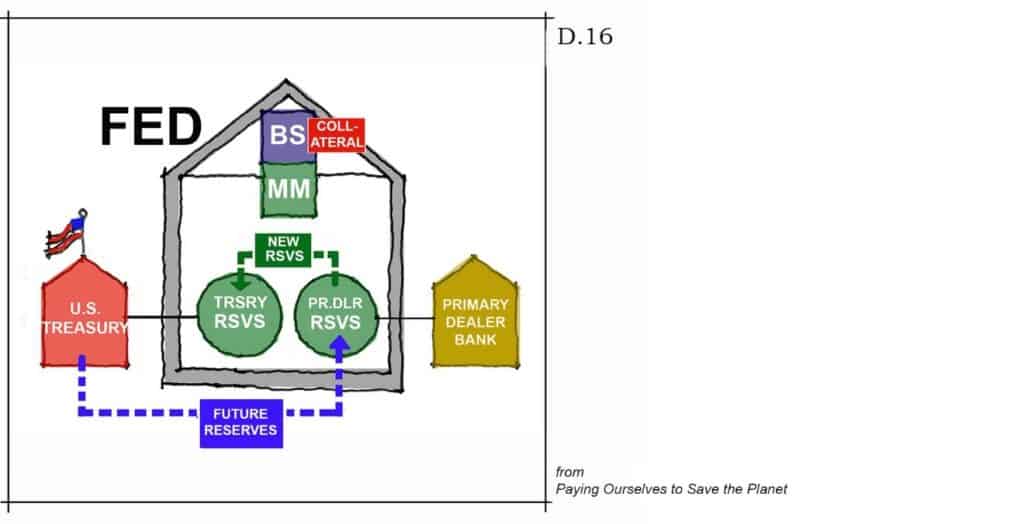

If private enterprise is unwilling, or unable, to trade existing Reserves for all the future Reserves the Treasury needs to trade (to meet its spending needs for the Public Enterprise) the FED initiates a special operation of its own to make up the difference.

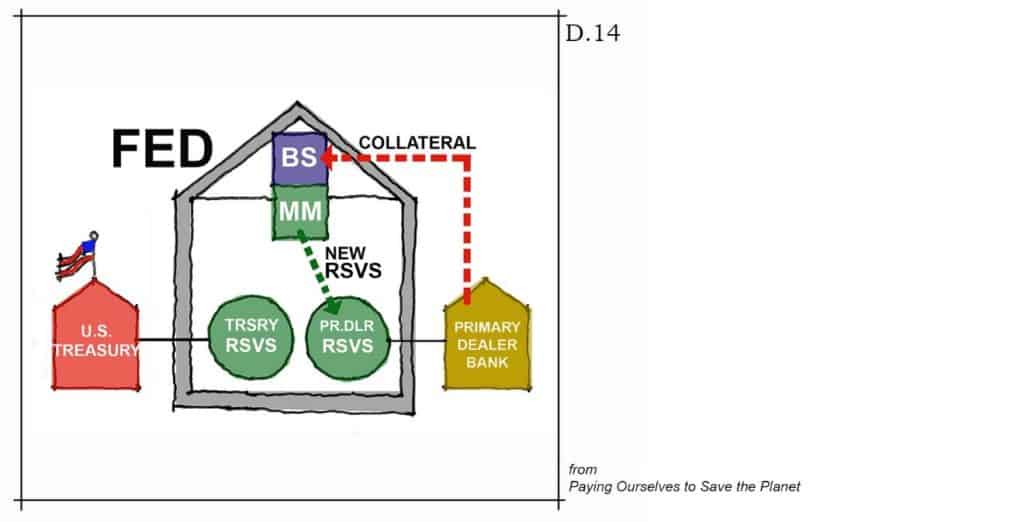

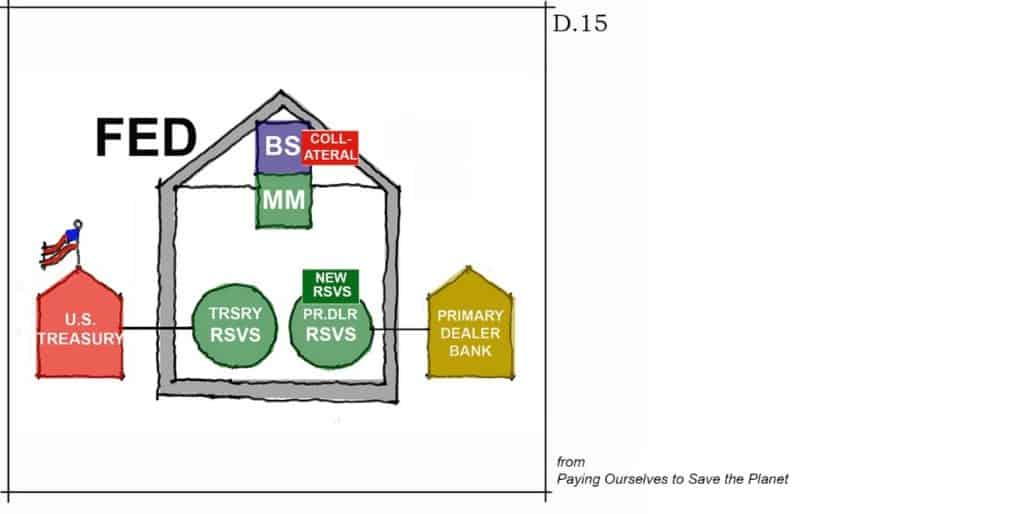

In the first step of this operation, the FED asks its “primary dealers”—certain very large banks in its system—to provide collateral to the FED in exchange for new Reserves which the FED then issues with keystrokes (the same as it does in the profit-making Reserve-issuing process).

The FED now has the collateral on its balance sheet and the primary-dealer bank has the new Reserves in its Reserve account.

Next, the primary dealer trades the new Reserves to the Treasury for the balance of the future Reserves certificates the Treasury has issued.

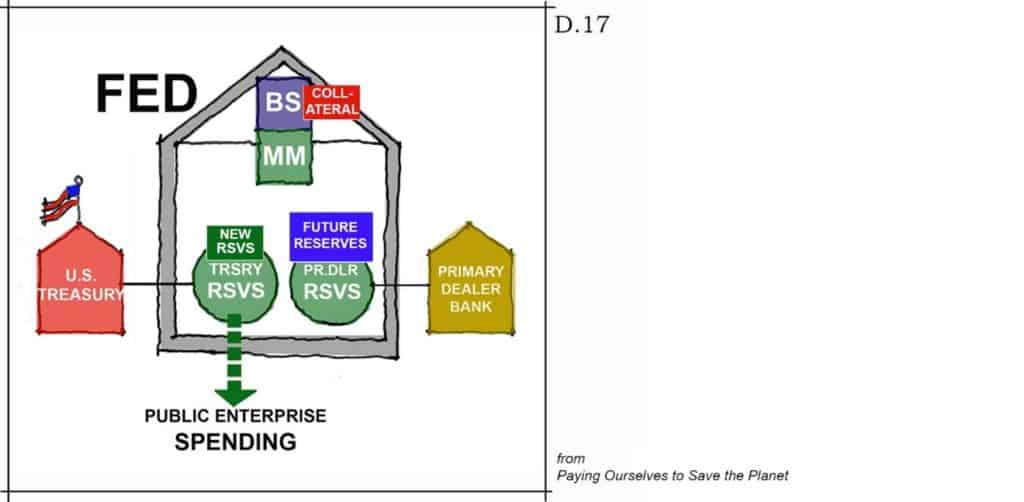

The primary dealer bank now has the future Reserves, the FED has the collateral, and the Treasury has all the Reserves it needs to pay for the not-profit-making goods and services of public enterprise that Congress, for the collective benefit, has directed.

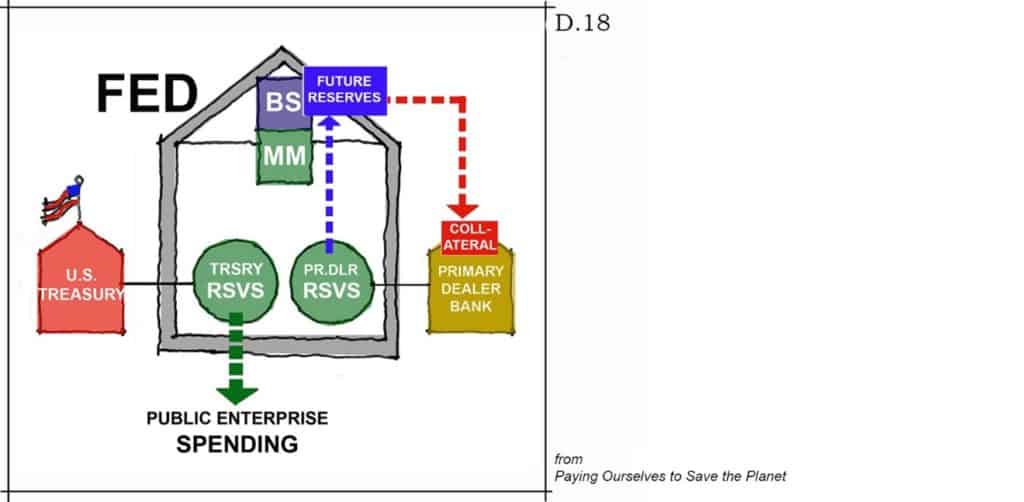

In the final step of the operation, the primary dealer bank takes the future Reserves it has acquired from the Treasury and trades them to the FED in exchange for the collateral it had first put forth. The primary dealer is thus restored to its original position—and the FED holds on its balance sheet the Treasury’s future Reserves.

What happens when the future Reserves certificate, held by the FED on its balance sheet, comes due? Does the FED issue new Reserves and pay them to itself? Obviously, the FED—which issues Reserves as needed with keystrokes—has no need to hold Reserves and, indeed, does not even have an account to hold them in! What happens is this: the FED simply erases Treasury’s certificate of future Reserves from its balance sheet. The money transaction comes to an end when the only actor who doesn’t need money ends up with it—like electricity going to ground.

The coordinated operations of the Treasury and FED, illustrated in these eight diagrams, establish the irrefutable fact that Reserves can be—and are—issued, as necessary, to pay for public enterprise. There is no need to raise taxes beyond what they are established to be for the purposes of creating incentives and disincentives to commerce. There is no need to “borrow” fiat dollars from private capital—and, indeed, there is no “borrowing” on the part of the Treasury, and there is no “national debt” that must be repaid by our grandchildren. What there is, instead, are the results of the public enterprise—the not-profit-making goods and services that provide substantial (and even existential) benefits to our collective wellbeing.