Yes, the dogs are barking that the latest CPI figures will deliver an interest rate cut this month after the election. Michael Pascoe is wondering about the dogs that didn’t bark earlier within the RBA.

The Australian Bureau of Statistics has shouted that the Reserve Bank of Australia was wrong not to trim interest rates at its April 1 meeting.

The funny thing is, the RBA itself back in February forecast that ABS verdict.

The dogs are barking that rates will be trimmed on May 20, a couple of weeks after the election. The mystery for me is why the dogs didn’t bark within the RBA much earlier.

The most impressive figure to come out of Wednesday’s ABS figures hasn’t been highlighted but it was quickly spotted by independent economist James Foster:

“In 6-month annualised terms, core inflation is sitting right on the midpoint of the RBA’s target band at 2.5%.”

As anyone other than the RBA board members can see, six-month annualisation of the trimmed mean has unsurprisingly proven to be a very nice guide to where the full year number is going.

A couple of major points about this:

Backward looking

Firstly, the RBA claims to be “forward looking”, as it should be given the lag with which monetary policy works. It also claims to be “data driven”. On the evidence of the data, I call bullshit.

Putting aside the way the bank has ignored its actual mandated target of the CPI, only caring about the trimmed mean measure, you’re not forward looking when you have inflation hitting the very exact target with monetary policy still restrictive, still tightening. It means you’re backward looking.

RBA “data driven” que?

As for being “data driven”, the bank has been ignoring the data. The best guide to what has been happening with inflation has been the monthly CPI numbers which have shown since September that the trimmed mean was within the two-to-three per cent range with the trend heading in the right direction.

Secondly, and this is the strangest bit, the RBA itself back in the February statement on monetary policy effectively forecast that the six month annualised trimmed mean would be 2.5 per cent now.

So the bank ignored the data and its own forecast in considering interest rates on April 1.

The conspiracy

I’ve been wary of giving any credence to suggestions of a political dimension to the RBA’s decision making, the idea of the bank not wanting to be seen to be giving Labor a hand by cutting rates at the meeting before an election. Back on April 1, Labor was not being tipped to win the election.

Could an institution that had been battered by Jim Chalmers’ dubious review be more than a little gun shy, be wary of doing anything that might put it offside with a new government, would prefer to play it safe by sitting on its hands until the next meeting, even if only subconsciously? After all, waiting for the next meeting is neither here nor there for the RBA board.

It’s not impossible, though I prefer to think it’s more a matter of the bank being timid. To use a phrase I think I might have coined, it’s a matter of the bank lacking the courage of having convictions.

Trumpmania syndrome

On top of its own February forecasts and fresh data, the bank’s last meeting also had forecasts from the world’s major economic bodies that Trumpmania was going to weaken the Australian and global economies. That’s the sort of thing that should have increased the call for a rate trimming, to actually look ahead rather than behind.

But, no, the RBA dogs didn’t bark. A mystery.

As posited here in February, if the election was to be a close-run thing, it would be rich if Chalmers’ RBA review was to cost Labor government, given how that review was obviously deficient on several fronts but enthusiastically adopted in full with undue haste. (https://michaelwest.com.au/pascoe-how-the-rba-got-it-wrong-on-interest-rates/ )

The economy in general and the cost of living in particular have been two of the main themes of the election campaign, with both major parties claiming to be the better managers. Alan Austin reports on what the IMF and the ABS have to say.

The latest half-yearly report from the International Monetary Fund (IMF) shows Australia climbing most global rankings, reversing the slide under the Coalition.

The IMF allows global comparisons by showing outcomes for 117 countries from 2016 to 2024 on twenty indicators. These include budget deficits/surpluses, tax revenue, government spending, national debt and net financial worth. It also shows projections through to 2030, although those were made before Trump’s tariff wars. So we shall see.

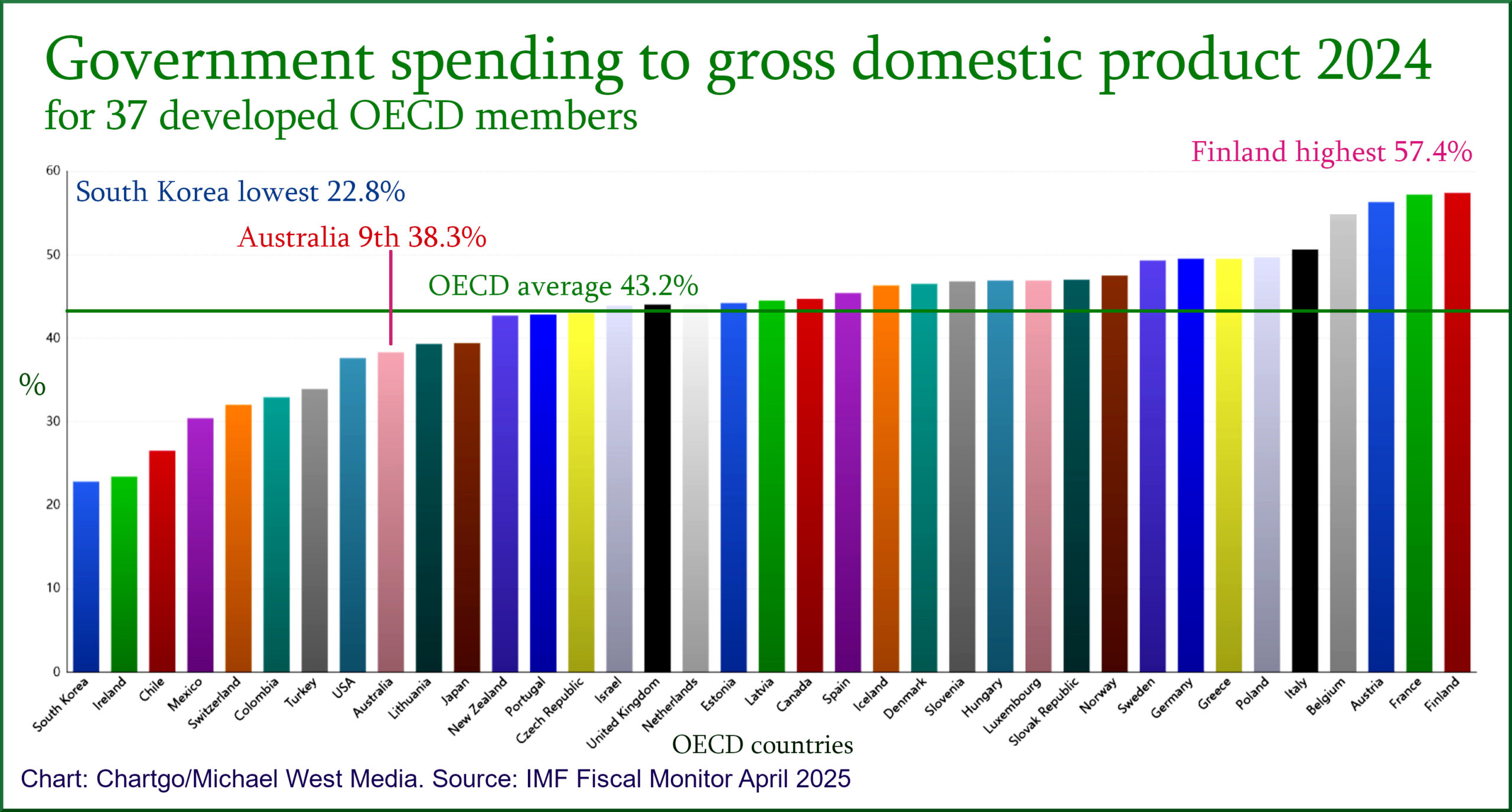

The tables on government revenue and expenditure confirm Australia is a relatively low-taxing and low-spending nation.

Australia ranked tenth on taxes collected relative to gross domestic product (GDP) among 37 wealthy OECD countries in both 2023 and 2024. That’s up from 11th or 12th between 2016 and 2019, pre-Covid, under the Coalition.

Australia ranked ninth out of 37 on government spending in 2024, up from 12th or 13th between 2016 and 2019. Government expenditure at 38.3% of GDP is well below the OECD average of 43.2%, and a far cry from the nine successful European economies spending more than 49.0%.

Debt declining

The IMF shows Australia’s net debt was just 30.1% of GDP in 2024, down 5.5% from the 2021 peak of 35.6% – in just three years.

Fewer than half the OECD reduced their net debt in that period – which was nowhere near as easy as the years 2014 to 2019 when all well-managed economies generated strong surpluses and repaid the debt stacked on in the global financial crisis.

The general picture the IMF paints is as positive for Australia as for any nation, along with Switzerland, Norway and Denmark. (Publisher’s note: Go Norway!)

This month’s pre-election economic and fiscal outlook (PEFO), prepared by the politically neutral secretaries of Treasury and the Finance Department, is highly instructive, especially when contrasted with the 2022 PEFO.

Deficits for the four years 2023 to 2026 were forecast before the last election to be $224.4 billion. After Labor changed Coalition budget settings, those deficits reduced to $31.9 billion, aided also by a strong global economy and higher tax income due to high commodity prices.

The department heads in 2022 forecast gross debt to reach $1,000 billion under Coalition policies in 2023-24. After the change of government, that did not happen. Debt is now forecast to hit the trillion some time in 2025-26, which may not happen either, depending on commodity prices and global conditions.

The boffins forecast gross debt at June 2026 would be $1,169.0 billion under the Coalition. They now predict $1,022.0 billion under Labor – $147 billion lower.

The Coalition’s interest payable on the debt for the three years 2024 to 2026 was to have been $57.3 billion. Labor has cut this to $45.7 billion.

Bureau bursts Coalition bubble

Several recent announcements from the Bureau of Statistics (ABS) undermine Opposition claims that most citizens are worse off now than in 2022.

The ABS has confirmed that the majority nay be better off with these reports:

Item #1. Employees in food and accommodation services have hit new records, confirming Australians are dining out and holidaying more frequently.

Item #2. Jobs in other areas of discretionary spending – arts and recreation, luxury retail sales – are also surging, in numbers and as a percentage of all jobs.

Item #3. Australian residents took 923,360 overseas trips in February, an all-time high for any February. Flights during the three months of December to February tallied a record 3,291,250, up 13.2% on the previous year.

Item #4. Total household spending in February reached a fresh all-time high of $75.6 billion. That’s five consecutive record months.

Item #5. Jobs outcomes for March, as reported last Thursday, continue to be close to the best-ever. The unemployment rate of 4.05% extends the streak of months below 4.25% to 40.

Item #6. Jobless Australians have been fewer than 650,000 for 40 months, another impressive milestone. Under the previous government, this exceeded 900,000 seven times, clicking over one million in July 2020, during the pandemic.

Item #7. The fortnightly age pension is up 12.2% since December 2022, when Labor’s first budget took effect, to $1,051.30; the adult unemployment benefit has risen 16.9% to $781.10; the living away from home youth allowance is 25.1% higher at $663.30.

Item #8. Wage rises have been above inflation for the last 16 months.

Many groups, including inner-city renters, may find all of the above irrelevant as they continue to feel the pinch of ever-increasing rents as housing supply remains well behind demand. But that’s another story.

It’s complicated. Nevertheless, may the best economic management team win on Saturday.

This post was originally published on Michael West.

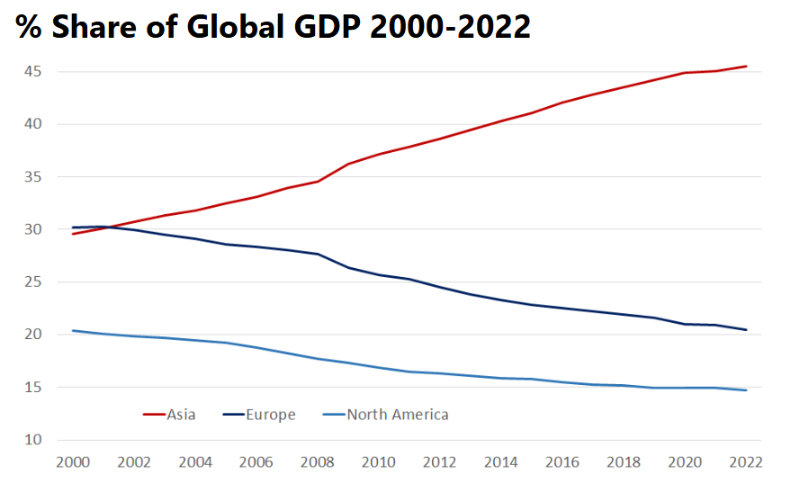

Poor old Donald Trump thinks the United States still dominates the global economy, but the ‘stable genius’ has lost touch with reality and is a couple of decades out of date, writes Michael Pascoe.

The US is important, the traditional consumer of last resort, but relatively speaking, it is no longer the colossus it once was. Other than in the fantasies of Emperor No Clothes, the US can no longer use economic heft to command the world.

You can quibble about what set of statistics you want to use and nominal versus purchasing power parity measures, but the reality eluding the Trump gang is in this World Economics graph.

Source: www.worldeconomics.com

It’s a mistake to concentrate too much on the “Chinah” part of Trump’s war on global trade. China, being America’s prime target, distracts from the totality of the mismatch Trump has chosen. (And it’s a bigger mistake to think China is most affected by the war, I’ll come to that.)

Long before Peter Navarro became Trump’s tariff capo bastone, he was a rabid Sinophobe, best known for his 2006 book, The Coming China Wars, and his 2011 tome, Death by China, subsequently turned into a quasi-documentary. A taste of the book is that it quotes a fictitious Harvard economics student, Ron Vara, (an anagram, geddit): “The Manufacturing Dragon is voracious. The Colonial Dragon is relentless. The American Eagle is asleep at the wheel.”

As for the “documentary”, Wikileaks offers the New York Times review observation that the “alarming and alarmist” film “undercuts its argument with an abundance of inflammatory language and cheesy graphics” and “is also unabashedly one-sided and short on solutions” but “its message, despite the hyperbole, certainly warrants examination and discussion”.

The LA Times found the “important political argument…was drowned out by xenophobic hysteria and exaggerations so rampant it becomes impossible to tell light from heat”.

In other words, it was exactly Trump’s kind of show, receiving a glowing endorsement, and 75-year-old Navarro is very much Trump’s kind of capo with a track record of promoting hydroxychloroquine as a COVID treatment, spreading conspiracy theories of election fraud and becoming the first former White House official to be jailed on contempt of Congress charges. Such is the quality of the man calling Trump’s tariff shots.

“Death by China”

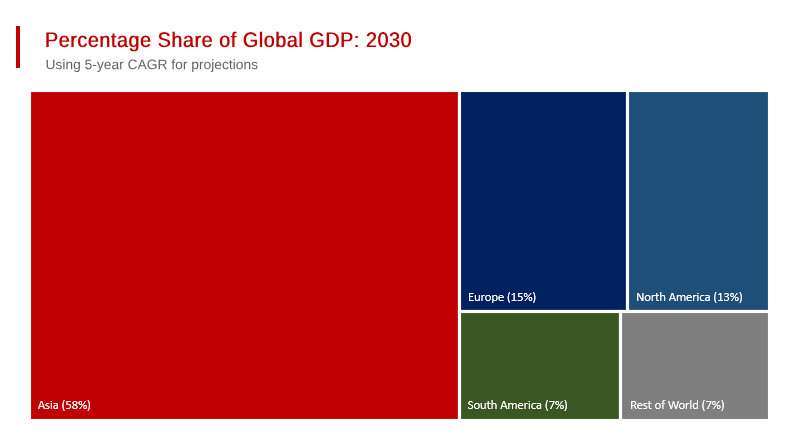

Whatever Death by China’s merits or otherwise, America has missed its chance to put China back in its box and keep it there, if it ever had such a chance once China decided to open up. The International Monetary Fund scores China’s share of the global economy at 19.3% on purchasing power parity (PPP) basis and the US at 15.6%.

World Economics research reckons the US share is 12.7% with China at 19.6 GDP and projected to rise to 22.1% in 2030.

(At current prices, the IMF counts America’s GDP as worth US$30.34 trillion and China’s as US$19.53 trillion, but PPP is generally considered a better basis for comparison.)

In any case, China is only part of the Asia story. World Economics’ 2030 projection will no doubt be changed by the Navarro/Trump tariffarama. I’d bet it will make the US share smaller than the forecast 13%, and Asia’s 58% will be larger.

Source: www.worldeconomics.com

America’s desire to bifurcate the world, putting China behind a tariff curtain and forcing other nations to choose “US or them” fails when the US is no longer the undisputed global economic superpower, let alone when it behaves like the proverbial pigeon playing chess – knocking over the pieces and shitting on the board.

Trump boasts of foreign leaders “kissing his arse” to get a tariff discount. What he ignores is the contempt he is held in and the destruction of any faith in America’s reliability. Insults and loss of face don’t go down well anywhere, but least of all in Asia.

The South China Morning Postcompiled a list of how dependent six major Asian economies are on the US market, dividing their GDP by their exports to the US. As the paper teased, China’s place on the list “could be surprising”.

Liberation Day stunt

On top of stopping USAID efforts to clean up Agent Orange and unexploded American munitions and landmines, Trump’s “Liberation Day” stunt included a 46% tariff hike on Vietnam, whose exports to the US are equal to 23% of its GDP.

The US is Vietnam’s biggest customer, accounting for nearly 30% of exports, followed by China at around 20%. Whatever goodwill the US might have been cultivating with Vietnam is gone.

Thailand was promised a 36% tariff. Its exports to the US equal 9.3% of its GDP. Malaysia’s US exports equal 8.9% of GDP. Have a 24% tariff. South Korea exports worth 6.2% of GDP, take a 25% “reciprocal tariff” threat.

Japan, a 24% tariff for 3.4% of GDP.

China’s exports to the US are now being threatened with, well, pick a number, any number, 145% last time I looked,

but those exports are the equivalent of “only” 2.7% of China’s GDP.

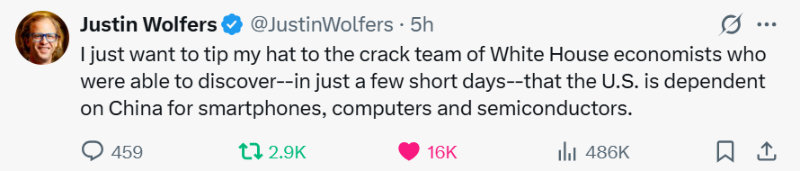

To lose it all would obviously hurt, though the Trump clowns have already realised that, d’oh, China makes stuff America needs. As American-resident Australian economist Justin Wolfers tweeted:

Professor Wolfers seems to have forgotten very few Americans speak irony.

China is prepared

China has been preparing for this trade war, its export markets diversified, America’s intentions well telegraphed. China has the advantage of high savings and an under-utilised domestic consumer market ready for priming if required.

At the same time, the US sinks further trillions into debt after decades of living beyond its means, something the bond market last week signalled may not be sustainable after all if fools run the place.

And China has the benefit of Donald Trump making it look more reliable and pragmatic and certainly less insulting than the US. Trump is providing China with an incredible opportunity to straighten up, fly right and win while the US loses.

Which is why Australia would be particularly stupid to fall in with Trump’s bifurcation plans, as Crikey’s Bernard Keane reasonably believes ($) the weak ALP/LNP leadership will.

How dumb would you have to be to pick this particular moment of historic turmoil to act all Trumpy and seize the Darwin port lease? The answer is as dumb as the ALP and LNP leadership.

Unreservedly sticking with AUKUS and what we pretend is the US alliance, signalling that we’re all the way with the USA even when the USA has gone crazy and worse, just means we’re picking the losing side instead of prioritising our own interests.

Donald Trump has declared a trade war, the share market is down, and US t-bond yields are rising. But how did it all start, and what’s next? Michael West and Kim Wingerei with the lowdown.

They say that truth is stranger than fiction, and when it comes to what Trump and his acolytes are doing to world markets, they are not wrong! Donald tanked the economy based on a book his son-in-law found on Amazon.

Donald Trump told Jared Kushner to find him an economic advisor – someone who could make him “look tough” and talk tough on China. Jared searched Amazon, saw a book called Death by China, and thought the title was “cool.” So he cold-called the author, Peter Navarro, and gave him a job.

It turns out that Navarro has no real economic credentials, except for an obsession with tariffs and a made-up expert named “Ron Vara” whom he cited repeatedly in his books. Who’s Ron Vara? A fictional economist, Navarro invented. It’s an anagram of his name.

This is not a joke. This is literally how the Trump administration created its trade policy – one that has so far wiped out $10 trillion in wealth, crashed markets, and has put the world at the brink of recession. A fake expert. A book cover. An Amazon search!

The China (bond) Syndrome

Earlier this year, the US imposed a 20% tariff on Chinese imports. On ‘Liberation Day‘, Trump added another 34%, and overnight, he vowed to up the ante and slap China with a 104% tariff on goods imported to the US.

The stakes are rising. China has yet to respond to the latest hike, but President Xi Jinping has made it clear he’s up for a “fight to the end”. According to The Economist, that may mean a “decoupling between the world’s two largest economies.” The cost of that on both sides of the Pacific is hard to measure.

China does, however, have another option: the ‘nuclear’ option of selling US treasury bonds, which would drive yields up and prices down and send the world into recession.

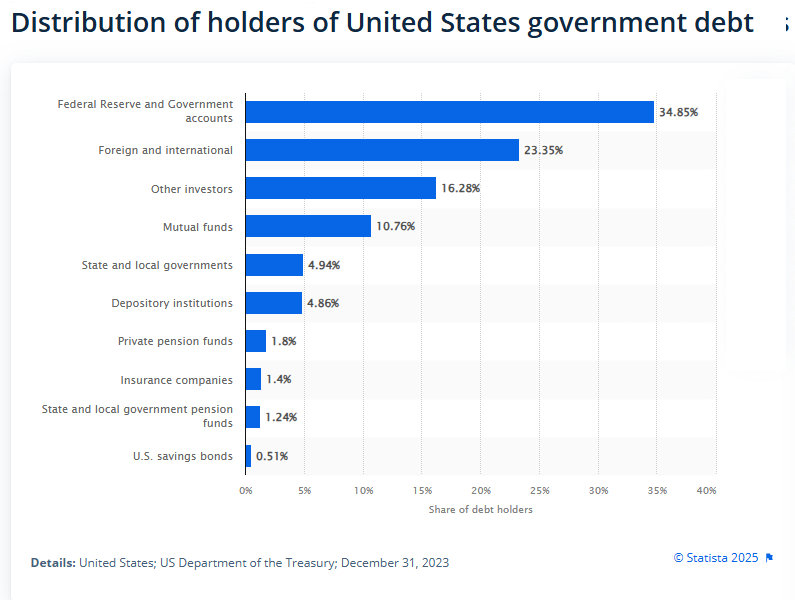

US Treasuries, or the US bond market, is the biggest market in the world, worth about $50 trillion, or around half of the world’s bond debt. Treasury bonds is how the US finances its deficit. Issuing bonds means borrowing money. But from whom? Who buys this stuff? Who owns most of the US Bonds?

Apart from the Federal Reserve and the US Government itself, the largest holders of US Treasury Bonds are Japan with US$1.1 trillion and China with US$868 billion (as of November 2024, Investopedia.).

China and Japan have had massive trade surpluses over the years, so what have they done with the money? A lot of it has been pumped into bonds, which are safe havens.

But it is no longer safe. This is the bit to understand. Bond prices are the inverse of yields, so when you sell a lot of bonds, you drive the price down. If the price goes down, the yield, or the interest rate, goes up. That’s what’s been happening this week.

And who knows if the Chinese are selling in quantity already? US 10-year bond yields are up by 10% since Liberation Day. It’s a heck of a lever to pull.

Tariffs are just a tax, so Donald is slamming massive taxes on imports.

That means prices for imports are going up, possibly at the same time there is upward pressure on interest rates because of people fleeing for the hills in the bond market. The knuckleheads in the US have hit their own voters the hardest.

But why would China want to flog its bonds, you ask? If they sell a whole lot, the price goes down for the rest they own, and they are simply hurting demand for their own goods in their biggest market, America. But Donald’s tariffs are doing that for them anyway. The just announced 104% simply doubles the price of everything from China.

Everything means all kinds of consumer goods, pharmaceutical ingredients, and electronics, including smartphones (9% of total). Hundreds of thousands of products with well-established supply chains are not easily replaced.

It is difficult to comprehend the scale of what is going on here, the sheer abomination which is US leadership in the world. Australia’s biggest export, iron ore, is tumbling, which means less money coming into our economy, which means less revenue for the Budget, which means fewer services for Australians.

Tariffs also mean less trade, which means lower economic activity worldwide. That is what is happening now, Trump’s aim is to boost US manufacturing to replace imports, but he is driving the world into recession.

Second, market turmoil means severe dislocation, like what happened during the GFC, so that will trigger further fallout.

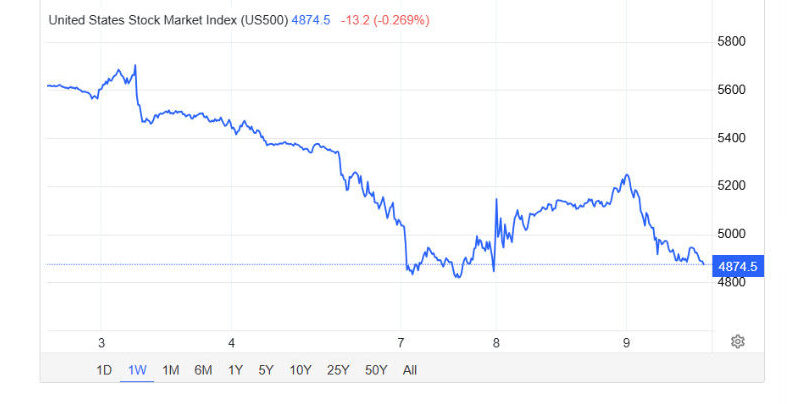

Along with the potential bond mayhem, there is a lot of stuff going on in the stock market, too: margin calls, short selling, funds in trouble, and forced sellers. What happens when share prices go down? The companies’ cost of capital rises.

US500 Index past week. Source: tradingeconomics.com

There is strong precedent for a tariff-driven disaster. When the US sharemarket crashed in 1929, the ‘Smoot-Hawley Act‘ hiked tariffs around the world, and trade dropped 20pc. A year or two later, we had the Great Depression, then hyperinflation in Germany, more debt defaults and the rise of Hitler, and World War II.

We are not saying this will happen again. As Mark Twain once said, “History never repeats itself, but it does often rhyme.” What we are saying is that it is impossible to predict what’s next, but in all likelihood it will get worse with one of the first effects being severe disruptions to world supply chains.

What about Australia?

Trump’s dopes claim they are trying to tackle trade deficits of the US, but they actually run a trade surplus with Australia, so the extra 10% imposed on Australian goods into the US makes no sense. Why don’t they buy Australian beef, they cry?

Because we are one of the biggest exporters of the stuff in the world. Do you want us to buy your iron ore and coal too?

How did Australia get locked into this giant stuff up, foreign policy completely rooted, allied to a bunch of dangerous morons engaged in genocide and destruction of the world economy. Time to get out of AUKUS, the greatest foreign policy hospital pass in history.

Housing affordability is a big issue for many Australians. Both the major parties claim to want to fix it, but neither has a plan to address the real causes of the crisis. Harry Chemay with the facts.

You know the housing market is in crisis when a high-flying investment banker and the CEO of an industry super fund make the same observations to the nation’s premier business publication.

Not natural allies by any stretch, one facilitates the pursuit of commercial profit-seeking, while the other represents some 3.5 million individuals hoping for a dignified retirement at some point in their lives.

Yet here they were, just days apart, with remarkably similar and profoundly disturbing insights into the woeful state of housing affordability in Australia today.

In early March, the CEO of Melbourne-based AustralianSuper, Paul Schroder, took to the stage at the AFR Business Summit and said this:

I think the big, burning productivity and cost of living problem is housing.

“I think we keep underestimating how worrying housing is. This is the crisis that is facing Australia.

“All we’ve done is pour all of this money into houses, which has deprived the economy of heaps and heaps of productive capital. We’ve got all this money in our domestic houses and we’re not backing business, we’re not creating new things, we’re not driving productivity.

“So, to me, all of our pants should be on fire about housing. Because, if our kids can’t live safely and securely, how can you be freed up to think positively about productivity or the future, if you don’t know where you’re going to live?”

About two weeks later, Jonathan Mott, a senior banking analyst at Sydney-based Barrenjoey Investment Bank, was on stage at the AFR Banking Summit and dropped more housing truth-bombs:

“Over the last three years, since we’ve started seeing rates go up, the lending to owner-occupier [households] who earn less than $120,000 per year (which is 60% of society) has fallen 66%. Only 8% of credit goes to owner-occupiers earning less than this.

At the same time, lending to investors earning more than $500,000 per annum is up 166%.

“This one percent of society is getting more credit [9% of mortgage lending] than the 60% who are owner-occupiers.

“This is not sustainable. If it doesn’t change and you live in Sydney, you’ll never know your grandkids, because they won’t be able to afford a house. They won’t live here.”

Both Schroder and Mott are experienced senior financial executives who can see today’s housing market for what it is: a brutal competition in which generally lower-to-middle income Australians are pitted against each other in a ‘housing hunger games’, either to rent from high-income investors or to buy from owner-occupiers (with the constant threat of being out-competed by better-funded investors).

Jonathan Mott’s concern about Sydney’s housing market has been validated by the just-released CoreLogic Home Value Index, which saw the median house price in the harbour city hit $1,472,393 during March, a new all-time high. Unit prices, meanwhile, rose to $851,934, 23% higher than the next most expensive capital city, Brisbane.

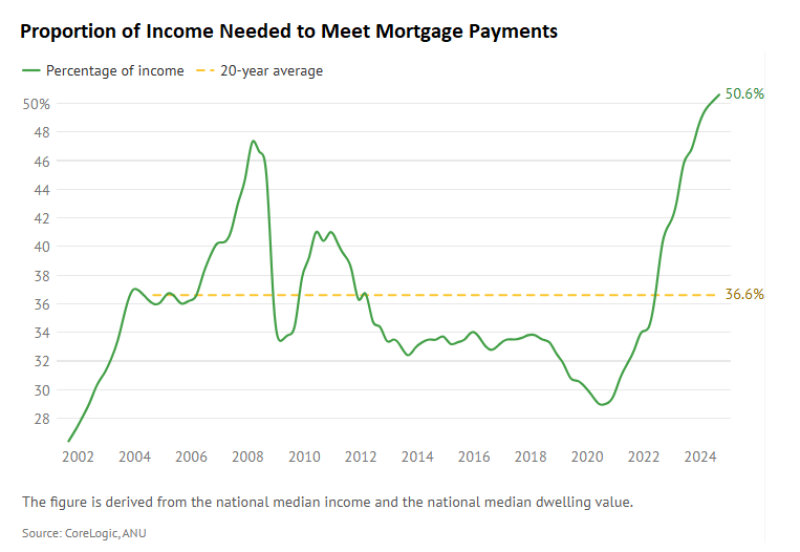

Mott is one of Australia’s most experienced banking analysts. He knows the role that mortgage lending plays in rocketing property prices, mortgage debt now sitting at some $3 trillion outstanding across homeowners and investors.

He would also undoubtedly be familiar with the current stats. The national average mortgage for a first-time home buyer is now around $520,000, while for existing owner-occupiers, it’s around $670,000 nationally and $811,000 in his home state of NSW.

Try servicing a 30-year $800,000 principal and interest mortgage at 6.25% pa on the median NSW household income of around $140,000. I make just under $5,000 per month on a household take-home pay of around $9,500.

It’s little wonder that mortgaged households were caught out by the 2022-23 spike in official rates from 0.1% to 4.35% (before last month’s 0.25% cut). The proportion of household income needed to service a mortgage rose from under 30% in 2020 to now accounting for more than 50% of a typical mortgaged household’s budget.

That’s been a key cost-of-living drain for many of Australia’s roughly 3.7 million mortgaged households, who collectively owe around $1.5 trillion, particularly lower-income and younger borrowers.

If you engineer a system where homeowners are forced to take on ever-increasing levels of debt relative to their household incomes, they invariably face more interest rate risk. Alas, such is life in the mortgage nation that is Australia today.

Paul Schroder’s focus at the AFR Business Summit was on productivity, that magical economic quantity said to drive our living standards. Productivity is, in essence, the amount of output each employee generates on average for each hour spent working.

More output per hour results, all else equal, in higher total national income and, in theory, the ability for employers to pay their workers higher salaries without consumer inflation becoming a concern ($).

Productivity is one of the ‘Three P’s’ in Treasury’s long-term GDP forecasting, alongside population and labour participation levels. Except productivity has essentially flatlined since 2016 and has actually been going backwards more recently.

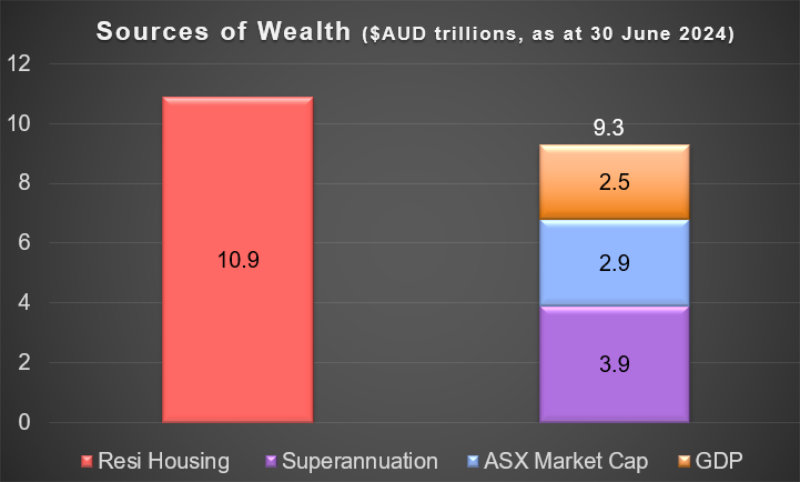

The AustralianSuper CEO identified a very likely contributor to the problem when he noted that our love affair with property sees Australia with a $11 trillion housing market and a $3 trillion GDP (almost 4X), versus a $50 trillion US housing market relative to its $29 trillion economy (about 1.7X).

Schroder’s argument that Australians over-save on residential property and deprive the productive economy of a domestic source of capital is valid. I made the same point in 2021 and again in a retirement conference last October to a room full of superannuation executives.

Source: ABS, APRA, ASX (author’s calculations)

You can take the entire Australian economy, add both the value of the ASX and the superannuation system,

and still be $1.6 trillion short of the wealth tied up in residential property.

That’s wealth currently held in non-productive land and buildings that could be used by Australian businesses to create Australian products and services, employ more Australians, and drive that elusive productivity lift.

Because even the Productivity Commission, in its recent deep dive into housing construction productivity, admitted that we get half as much house per construction hour worked than we did three decades ago. If productivity growth is indeed the path to economic prosperity for all Australians, then perhaps continuing to bank on residential property is not the long-term road there.

Trade tension impact

Something to think about in a post ‘Liberation Day’ world; a world where rising trade tensions will put the focus squarely back on productivity, and in finding ways to support Australian businesses to compete, grow, employ and generate rising incomes.

Being leveraged up to the eyeballs to own property might provide the illusion of wealth (the RBA itself accepts that a ‘wealth effect’ exists here), but it won’t do much to raise long-term living standards for working Australians.

And approaching retirement with mortgage debt, as one in two households aged between 55 and 64 now do, won’t help living standards thereafter either. That’s the legacy of real mortgage debt for those over 55 increasing by more than 600% between 1987 and 2015.

It’s a game of property snakes and ladders that Australia has played over the last 25 years. A game that, as Mott correctly asserts, is patently unsustainable.

As crazy as Trump’s tariff mania is, the world will keep turning with not as much damage as the headlines have us believe, Michael Pascoe writes.

Recession in America, global growth reduced by a third, China shrunk, Australia whacked, the earth splitting asunder spewing forth serpents…or maybe not.

Nobody needs further proof that the inmates are running the Washington asylum, a.k.a. the White House, but yes, add to the pile the Trump gang’s view that Europe’s VAT and Australia’s GST are protectionist levies. On the other hand, keeping the VAT/GST in mind helps lower the fever around “Liberation Day” headlines.

It’s a given that tariffs primarily work as a tax on consumption. America doesn’t have a federal consumption tax, just a patchwork of state and local sales taxes ranging from zero to 10.1 per cent.

Try looking at Trump’s new blanket base tariff of 10% as a partial federal consumption tax, and it is not quite so scary. Even with the “reciprocal” tariffs, averaging about 15% by Goldman Sachs’ estimate, they only cover a minority of Americans’ consumption.

Cars, steel, aluminium, and some other goods yet to be specified are different, but overall, tariffarama should have less immediate US consumer impact than the introduction of Australia’s GST did. At that time, our central bank agreed to “look through” the one-off hit to inflation, as the Federal Reserve might be tempted to, given the likely concurrent impact of weakening consumption.

Make no mistake, Trump and friends are idiots, while those who voted for him and continue to support him are worse. Cue the Sky After Dark gang. Just as Trump falsely promised to lower the price of eggs, he has claimed the tariffs will lead to lower prices for Americans. Not on this planet.

The tariff crusade is and will damage America, making it less, not great again.

(An anonymous White House official also has been quoted as saying quality wasn’t the reason Americans bought more European cars than Europeans bought American cars. Tell him he’s dreamin’, too.)

In very rough numbers, the US imported US$3.3 trillion worth of stuff in 2024, some of which is re-exported. And Trump doesn’t seem to have thought of services yet, perhaps because the US runs a services trade surplus, perhaps because he doesn’t think. US retail sales were 58% more than that – US$5.28 trillion.

Unintended consequences?

And then there is the reality of exchange rate movements and exporters and American importers shaving margins a bit to stay competitive. Goldman Sachs is guessing the tariffs, including the 25% on auto parts and vehicles, will add 0.5% to America’s “core personal consumption expenditures”, an inflation measure.

If the Fed thought the tariff thing would stabilise – a big “if” – the central bank could stay relatively calm and not try to damage the US economy any more than Trump is. Of course, the bald numbers only tell part of the story. A couple of percentage points less than a fifth of Americans’ food is imported, so divide the tariff impact by five, and it doesn’t look so bad.

But nearly 60% of America’s fresh fruit and nuts are imported along with 40% of vegetables. Obviously not a problem if your diet is based on McDonald’s, though the 45 grams of Australian meat in a cheeseburger might cost 30 cents more.

The US can no more re-industrialise overnight than Elon Musk can live on Mars. US industrial capacity is only running a percentage point or so below its long-run average.

There are not vast arrays of American factories ready or wanting to fill the country’s $2 shops.

US consumers will have to keep buying imported food as US farmers already produce about as much as they can produce, never mind what happens if their illegal crop pickers are deported.

The international beef market is deep. America exports nearly four times as much beef as it imports from Australia. Its main markets are, in order, Japan, South Korea, Mexico, Canada and China. They are all countries looking for retaliation that is relatively painless for their own consumers. Ditching US beef fits that bill.

Which means there might be more tasteless American grain-fed beef available for McDonald’s patties if our superior free-range beef is priced out of the market, but I doubt it. American cattle farmers are not efficient enough.

Trump’s latest trade war is old news for China. It is already exporting more to the global “South” than it is to all of the “West”. China knows its economic future does not lie in selling MAGA hats to daft Americans.

As a Bloomberg writer summarised it:

“Trump’s escalating tariffs are expected to raise the cost of trillions of dollars in goods shipped annually to the US from other countries, with most economists predicting American consumers will be among the hardest hit as a result. Trump’s latest salvo also turbocharges the worldwide trade war he began, a conflict likely to be marked by tit-for-tat strikes that destabilize supply chains, stoke inflation and encourage more countries to form alliances that exclude America.

“That dynamic presents a political problem for Trump, as his strategy may halt US economic growth in its tracks. And even if he’s eventually proven correct that his trade war will help re-industrialize the economy, that wouldn’t happen for a long time. In the interim, those Americans who elected him to lower inflation may very well find the opposite to be the case.”

And the rest of the world will be moving on, leaving the US to stew in its own corrupt plutocracy, becoming steadily less great. The American auto industry promises to be the prime example of that – heavily protected and thus sentenced to needing protection to cover for higher prices and lower quality.

The entrepreneurial drive, hopes, and needs of the 7.9 billion people living outside the US won’t be stymied for long by Americans’ turning to isolationism and nationalist populism.

Ironically, “Liberation Day” is most likely to mean greater liberty from the American hegemon we have been addicted to. As I’ve argued elsewhere, the tariffs don’t help, but they are the least of what should be our concerns with the United States.

Now what we need is a government prepared to face up to that.

The Reserve Bank continues to ignore market signals and runs the risk of once again leaving the brakes on for too long while being caught in the headlights of uncertainty, Michael Pascoe argues.

Inflation is printing within the target range, growth, both local and global, is expected to weaken, and the labour market’s perceived “tightness” is clearly not inflationary – yet the Reserve Bank of Australia is frozen, unable to make a decision other than to not make a decision.

We’ve hit a dud patch in monetary policy when the money market reckons there is next to no chance the RBA will trim rates at its meeting next week. If the RBA isn’t considering a further cut, what is it doing?

The answer is: dithering.

Despite the data, despite what has already happened to inflation, despite admitting there’s a nine-month delay between the bank lifting its foot a little off the brake and the economy gaining speed, the bank is caught in the headlights by Martin Place’s favourite word: “uncertainty”.

The certainty of uncertainty

Of course, there is “uncertainty”.

If there was “certainty” about the need to move rates, it would confirm that the bank had been too late to move.

The “uncertainty” about inflation rising meant the bank was too slow in lifting rates in 2022 – it waited until it was certain inflation was a problem and thus made it a bigger problem.

The “uncertainty” about the economy’s softness and contained inflationary pressures mean the bank is too slow now in easing rates somewhat closer to neutral and thus will make the economy weaker and unemployment higher.

The “uncertainty” about global trade and growth created by the Trump mobsters strengthens the case for getting ahead of the game instead of playing catch-up. Shallow local commentary suggesting tariffs lifting American inflation means we also need restrictive rates is simply bizarre.

The peanut gallery has trouble realising we are not part of the American economy, unable to move on from last century’s cliché of “if America sneezes, Australia catches a cold”. Happily, we are more part of Asia’s economy. In the GFC, America caught double pneumonia, and we only sneezed.

If the Trumpsters succeed in their punitive tariff folly, the impact on us is most likely to be deflationary as international trade turns away from the US in search of more reliable partners. A weaker economy with disinflationary pressures is a recipe for rate cuts before it comes to pass, not afterwards.

Since the February board meeting, the RBA Governor, Deputy Governor, and head of economics have all had a crack at explaining “uncertainty”, collectively leaving all but the doctrinaire hawks scratching their heads about why the money market should be convinced there will be no movement next month.

RBA and market perceptions are damaged by the national commentariat more interested in domestic political points than the overall economy. Repeating LNP talking points about “Labor spending causing inflation and requiring tight monetary policy” seems to be self-fulfilling with interest rates, such is the desire of the RBA to be at one with money market expectations.

Deputy Governor Andrew Hauser went closest to making the case for further easing rates when he unveiled ($) what the AFR called a “secret chart” showing inflation was in danger of falling below target. Yet the AFR persists with the line that there is “no realistic prospect of another cut in interest rates before the May election”. Why not?

The danger here is that the RBA lives in fear of being tarred with a political brush.

If it did cut rates next week, the usual suspects will claim it was pressured into doing Labor a favour. But pre-emptively ruling out a cut, which is the money market and commentariat’s understanding, means the bank has indeed compromised its integrity and mandate.

After the February meeting, Governor Bullock’s outlook was summarised by her declaring the bank just didn’t know. Of course, it never can know for sure but needs to make a judgement.

RBA chief economist Sarah Hunter last week went long on the “uncertainty” vibe despite spelling out the need for the bank to have a “forward-looking approach” to setting rates. This raises the question of which rear vision mirror the bank is concentrating on to obtain its forward view.

The dreaded “trimmed-mean” is all the rage in RBA land, despite the bank’s actual mandate stipulating the common-or-garden variety of Consumer Price Index.

As I’ve written here before, there seems to be a crazy idea that the trimmed mean somehow predicts the future instead of merely being another measure of the past. It lagged the CPI in picking up that inflation was picking up, a factor in the RBA being late to lift rates.

You would think anyone trying to be “forward-looking” would be most interested in the most up-to-date data, not the quarterly measures, the midpoint of which is months old when published.

The ABS monthly inflation series is proving to be a better guide to turning points that the trimmed mean. No measure is guaranteed to always be closest to the pin with the benefit of hindsight,

but it’s in delivering the vibe of the present that data should be prioritised.

Instead, the RBA gives the impression of ignoring the monthly figures – the figures that had been pointing to the need to cut ahead of the quarterly history.

The latest monthly release was on February 26 for January. It showed the CPI smack on the RBA’s new adopted target of 2.5 per cent and the annual trimmed mean at 2.8 per cent, within the actual mandated range of 2 to 3 per cent. It had been 2.7 per cent the month before.

The next, for February, will be published on Wednesday, nice and fresh for the RBA board meeting next Monday and Tuesday. Another low number around the target would have a responsible board very actively considering an immediate rate cut – unless it was made up of hopeless ditherers, caught in the commentary headlights.

At a glance it might seem a bit of monetary policy wonkery, but the real-world implications are huge, suggesting the RBA Review might cost Labor the election, Michael Pascoe reports.

When the RBA refuses to believe what has already happened over the past year and admits it doesn’t know what is happening now, a difference of 0.2% in its more-often-wrong-than-right inflation forecasting over the next two years should be about as vital for setting interest rates as last year’s wool price.

But thanks to Jim Chalmers’s dubious RBA review, on current polling, it looks like costing Labor the election.

Instead of the first-rate cut in December, the second this week, and indications of another on the horizon, giving Labor some real momentum in slaying the inflation dragon, Albanese will be campaigning on a single begrudged trimming and RBA warnings of no more to come.

A weakened RBA and triumphant Treasury saw Chalmers’ review swallowed without reservation, embraced with apparent enthusiasm even. The result is our central bank effectively ditching the flexible inflation target that had served it relatively well for three decades, replacing it with a straight jacket.

This pleases the doctrinaire hawks who want higher unemployment to push down wages, remembering the good ol’ days of previous administrations when wages suppression was official policy. Too bad that it retards our economic growth and all that flows from it.

Rate cut decision

As was made clear on Tuesday in the RBA governor’s media conference, the bank only pays lip service to its actual mandated target of keeping CPI inflation in the 2-to-3% zone over time. It’s now all about the precise trimmed mean at 2.5%, the midpoint target recommended by the review without any evidence of it being superior.

The result is the RBA being late to the rate cutting party, repeating the mistake of not believing what was in front of it when it was slow to start lifting rates in 2022.

The RBA now knows its precious trimmed mean inflation was running at an annualised rate nicely under 3% over the second half of last year. And, as printed in the Statement on Monetary Policy on Tuesday, the RBA thinks the trimmed mean measure is running at 2.7% cent now and is forecast to stay there for the next two years even if it cuts rates twice more this year.

But, thanks to Chalmers’ review, that’s not good enough to ensure more than this week’s trimming.

Tuesday’s was a most curious and somewhat frustrating Statement and media conference. The RBA is printing one thing but saying another. The bank claims to be “data driven” but it doesn’t believe the data in front of it, let alone the forecasts it publishes.

If it did, Tuesday was a great opportunity for the RBA to give itself a pat on the back.

Inflation was brought down within the target range, even within the forecasting margin of error of the silly 2.5%, with a strong labour market and unemployment steady around a lowish 4%. How good is a soft landing on a narrow path?

The outlook, what outlook?

And, thus, yes, the outlook would be for another rate cut on April 1, if only to make up for the one that should have happened in December. Alas, this RBA doesn’t have the courage of having convictions. Despite the data, it’s all too uncertain.

“I don’t know,” admitted Governor Bullock.

With respect, Governor, nobody ever “knows”. Yes, to repeat the cliché, forecasting is hard, especially forecasting the future. Nobody has a reliable crystal ball. Nonetheless,

it’s the RBA’s job to go with what it does have.

And you know what worries the RBA board the most, as explained in the final question of the media conference? The labour market that it is struggling to understand and simply doesn’t believe.

Governor Bullock said it was concern about the tightness of the labour market that was the strongest argument in the board meeting for not cutting rates, that made it a close decision before reaching “consensus”.

The past year has shown Australia can enjoy a strong labour market and unemployment of 4% and disinflation.

The RBA waffles about “full employment” because it doesn’t know what it is, ditto the NAIRU (the non-inflation-accelerating rate of unemployment) that it prefers not to talk about.

The RBA believes the labour market is “tight”, but what it can’t say is whether it is too “tight”. It doesn’t know.

And snap, right on cue, the December quarter wage price index yesterday prints at a low 0.7% for the quarter and 3.2% for the year, another slice of data showing it is not too tight. And snap again, Australia’s biggest business lender, the NAB, reports a profit fall with more borrowers falling behind in their repayments.

I put to Governor Bullock on Tuesday that a year ago, the bank’s statement said it was possible we were at “full employment” but not very probable. After 12 months of unemployment around 4% and inflation falling, the latest statement admits it is “possible” the bank got it wrong. I asked how many months would it take before the bank accepted it got it wrong.

The Governor answered that full employment was a very nebulous concept that you can’t put a number on. The bank was “surprised” that unemployment was still at 4% with a strong labour market and inflation was falling…and the jury was still out.

In the governor’s answer and within the statement document, it is surmised that some of the disinflation has come from profit margins being compressed. It was not stated that this was necessarily a bad thing, but for at least some board members to be pushing back on the “tight” labour market smells to me like a bias on the board towards capital having a greater share of profits rather than labour.

After all, that had been the trend in those good ol’ days.

The simple question for the RBA is that, as it says, monetary policy remains restrictive and if it keeps rates restrictive for too long to chase the review’s 2.5% precise target, a mere 0.2 below what’s happening and is forecast to happen … well, for the want of a nail the shoe was lost and so on.

The latest Productivity Commission report on government services underlines three decades of housing policy failure that the LNP promises to make worse while Labor attempts to maintain the deficient status quo. Michael Pascoe reports.

In a parliamentary fortnight awash with miserable politics, Senator Andrew Bragg tried his very best to land the title of asking the most inane question in either house.

The Coalition’s actual “shadow minister for home ownership”, Michael Sukkar, must have been too busy trying to gag Mark Dreyfus from speaking about the LNP politicising antisemitism, so it was left to Bragg, the shadow assistant minister, to waste the Senate’s time with a particularly dumb effort that he no doubt thought was smart, or perhaps even cunning.

Bragg engaged his full grasp of the housing crisis to pose, “How many houses have been built under the Housing Australia Future Fund agenda?”

Yes, Andy, we can all see what you did there. Of course, none have been built. Given that you partnered with the Greens to delay the necessary HAFF legislation for months in the Senate, you’d know the HAFF could not be established until November 1, 2023.

Only then could Housing Australia do the work of finding viable community housing projects, announcing the initial pipeline of 185 last September to deliver more than 13,700 social and affordable homes with the scheme’s first year of HAFF funding. The first 700 HAFF-financed affordable and social homes are scheduled to be finished by the end of this financial year.

And it is reasonably possible Bragg understands it takes time to get stuff built these days. So he knew the short answer to the question would be “none yet”.

Oh, such a gotcha! Indeed, Bragg was so proud he even posted it on his YouTube channel. Such is the Coalition’s dedication to the pursuit of image over substance.

What if the LNP wins?

A much more interesting question would be: “How many social and affordable homes will be built under the HAFF agenda if the LNP wins the next election?”

The answer is the same: none. One of Dutton’s extremely few announced actual policies is to scrap the HAFF.

And therein lies the core difference in what passes for housing policy between Labor and the LNP. Both sides of the party duopoly remain overwhelmingly and hopelessly committed to “the market” solving the Australian housing crisis that is leaving it to “the market” created. However, Labor will try to maintain the insufficient percentage of the affordable and social housing stock, while Dutton’s LNP will happily let it shrink further.

LNP lips curl at the thought of “houso”.

While the housing problem is multifaceted, I hold the unfashionable belief that it is the three decades of policy crime against social housing that has tipped us from “bad” to “crisis”, that our present shortage of housing pretty much equates to what wasn’t built to maintain our 1990s percentage of social housing.

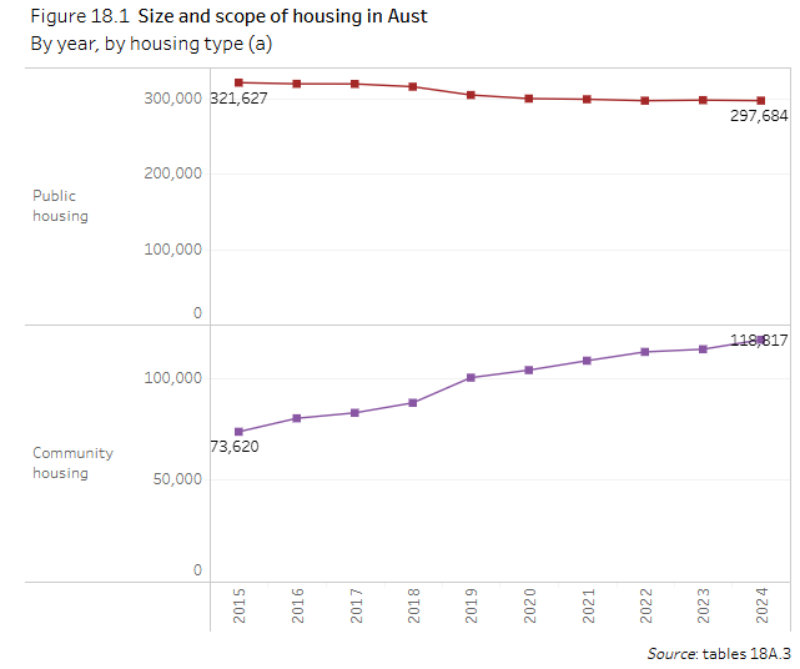

Each year, the Productivity Commission publishes a shame file on our neglect of social housing in its “Report on Government Services”. The 2025 report quietly dropped on January 30.

Leaving aside Indigenous housing in a separate category, the PC counted just 3,937 extra public and community housing dwellings last financial year.

That’s 0.95% growth, less than half the rate of population growth, not enough to stop the steady slide in social housing’s proportion of total housing stock, not enough to dint the growing waiting lists for social housing, a.k.a. desperate people in need of affordable shelter.

The latest deficient score is pretty typical of this century and actually considerably better than the nadir reached under the Morrison Government when Sukkar was housing minister. In 2019, there were only 2,325 public out of 202,306 total dwelling completions, 1.1 per cent.

Since 2015, our social housing supply has only risen by 5.4 per cent, an extra 21,154 dwellings. In technical terms, bugger all.

Source: Productivity Commission

The growth in community housing has slightly overtaken the reduction in government-owned public housing as governments have offloaded as much as they could of this difficult responsibility. Encouraging the offload is the ability of community housing to tap into Commonwealth Rental Assistance that public housing tenants can’t.

Declining quality

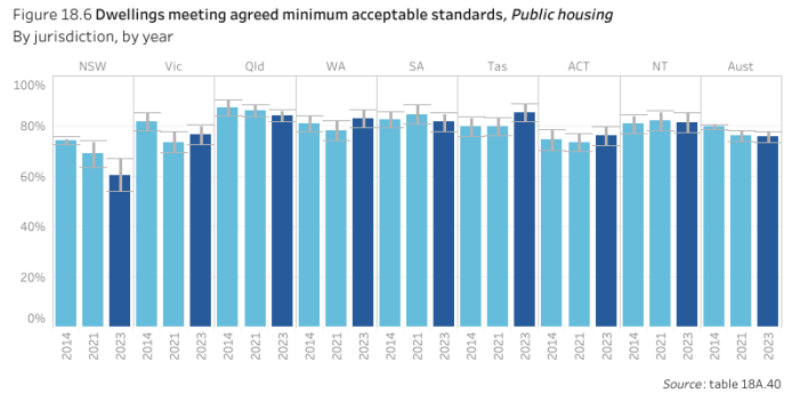

And then there’s the question of declining quality in the public housing that remains.

The PC reports that 76% of public housing dwellings in Australia met “agreed minimum acceptable standards” in 2023. In other words, about a quarter did not.

Most of the decline comes from NSW, where only 61% met acceptable standards, down from 74% a decade before.

Community housing scores better, 84% acceptable nationally and 82 per cent in NSW.

Source: Productivity Commission

Standards are relative. Crucially, public and community housing is affordable for those on very low incomes, while the private market is not for most, even with our increasingly expensive Commonwealth Rental Assistance.

I have reservations about using the HAFF mechanism for funding social housing. If these off-balance sheet Future Fund-run honeypots were such a good idea, we’d have one for nuclear submarines and every other major spend. I’d prefer government to return to those heady days of directly funding public builds, both for purchase and rental involvement, as

leaving it to the market demonstrably has not worked.

But that is not going to happen. Public outrage over housing has been successfully diverted into zoning and tax and red tape issues, missing the main game.

A duopoly unable to admit the effect of Howard’s capital gains tax discount certainly won’t go near actually accepting responsibility for housing as a human right and returning to building a hefty proportion of it to keep the developers honest.

So the PC shame reports will roll on. If Andrew Bragg & Co get their way, they will get worse. If Labor continues, they will merely stay bad.

Trump’s much anticipated tariff war is on as the US imposes import duties on Canadian, Mexican and Chinese goods, and those countries retaliate. What does it mean for the world and for Australia? Scott Phillips with some of the answers.

Over the weekend, US President Donald Trump announced 25% tariffs on imports from Mexico and Canada (but only 10% on imported Canadian energy) and an additional 10% tariff on products arriving in the US from China.

Unsurprisingly, Canadian Prime Minister Justin Trudeau has retaliated, putting a 25% tariff on imports from the US. In his announcement, Trudeau was blunt, telling Americans: “Tariffs against Canada will put your jobs at risk, potentially shutting down American auto assembly plants and other manufacturing facilities.”

They will raise costs for you, including food at the grocery store and gas at the pump.

Discussing Canada’s retaliation, Trudeau said, “We didn’t ask for this, but we will not back down”. Canada’s Department of Finance estimates that cross-border trade (in both directions) currently adds up to nearly $1 trillion per year.

Mexico is reserving its options, with plans to announce its own response in the near future.

Weak justification

This is, unfortunately, but not surprisingly, the first of a likely long series of ‘threat, action and counteraction’ scenarios we could see play out over the next four years.

And it’s hard to separate the politics from the economics because, frankly, the economic justification is as weak as the foreign policy one.

Donald Trump claims this decision was made primarily in response to imports of the drug Fentanyl from Canada to the United States.

Notwithstanding that border controls are universally about policing imports, not exports, as recently as 2020, the United States Drug Enforcement Agency found that “China remains the primary source of Fentanyl and Fentanyl-related substances trafficked through international mail and express consignment operations environment, as well as the main source for all fentanyl-related substances trafficked into the United States.”

“Some fentanyl products are smuggled from Canada into the United States for sale, on a smaller scale”

Perhaps things have changed meaningfully since, and Canadian fentanyl is the new overwhelming scourge.

Perhaps, but that data makes the above-mentioned tariffs seem just a little disproportionate. If the 25% tariffs are necessary, why only 10% on energy?

One might suppose that the price of petrol is more important than the self-declared war on Fentanyl. Then again, given more of it comes from both China (10% higher tariffs) and India (no tariffs, yet at least) – and that there’s been no concurrent action on drugs inside US borders – one might question whether the war on drugs is really the motivation it’s claimed to be.

Who pays?

Former US Treasury Secretary Larry Summers has, overnight, suggested that tariffs could increase US inflation by 1% over the next nine months. And, as we know well from the experience with inflation over the past five years, when prices go up, they tend to result in a permanent reduction in living standards.

Trump has acknowledged the potential impact (though characteristically hedging his bets), posting (in capitals, of course) on social media:

WILL THERE BE SOME PAIN? YES, MAYBE (AND MAYBE NOT!).

Which is the stupidity of tariffs. While the political spin is ‘tariffs on Canada’ (Mexico, China…), the tariffs aren’t paid by those countries but by US consumers.

And then, predictably, those countries retaliate, putting tariffs on imports from the US, pushing prices up for, in this case, Canadians. It is a textbook lose-lose scenario.

But what about ‘making things again’? Isn’t that a justification?

Well, American unemployment is 4.1%. Maybe a small minority of those people have skills that could be directly and immediately applied to new US manufacturing. That is, after new plants are built, machinery is bought (from overseas?), and operations commence, which would take years.

And that assumes those businesses were prepared to make capital investments given the risk that such investments may not be economically feasible if a future administration were to roll back tariffs.

Regardless, most of those unemployed Americans wouldn’t have the right skills or be in the right places, anyway. So then 100% of Americans would be paying more, but for almost no meaningful employment gain.

What about Australia?

That’s the problem (and we hear echoes here in Australia) with ‘we should build things here’

We absolutely should, if it makes sense; if the workers would earn more than they do now if consumers of those products will pay less than they do now, if the quality of the products would be better than they are now, and if we don’t have to tip more government spending into the endeavour.

Also, I’d like a unicorn.

See, that’s the benefit of free(r) trade: we sell them things we do better and/or cheaper, and we buy things they do better and/or cheaper. It’s not perfect, but it’s a very good way to improve living standards in both countries.

Tariffs reverse all of those things. Either we pay more for imports, or we pay more for locally produced alternatives. Think that’s a good thing? Because it supports ‘local’ jobs and products? It seems like it at first. But if you’re paying more for Product A, you can’t buy as much of Product B (or buy Product B at all).

Your living standards fall, and the business making Product B goes broke, and those workers lose their jobs. Something that started sounding good at first blush, suddenly seems more complex and maybe a bad idea after all.

If it’s easier to conceptualise, consider if there were trade tariffs across Australian state and territory borders. Queensland bananas would cost more in NSW. NSW-made steel would cost more in Queensland.

NSW workers wouldn’t be any better off, but the bananas would cost more. Queenslanders would pay more for steel and get no benefit from the higher price of the produce they send south.

But for now, at least, there’s little direct impact on Australia. That doesn’t mean there won’t be any impact, though.

International tariffs

Higher tariffs on Chinese imports into the USA will almost certainly reduce demand for those products. And I don’t need to remind you that China is our largest trading partner. According to DFAT, China bought $219 billion worth of Australian exports in 2023, fully one-third of everything we sent offshore.

So it’s probable that any Chinese economic impact will have echoes in that country’s demand for Australian exports.

Beyond that, it’s anyone’s guess. Will Trump pick a fight with Australia? We would have assumed not, but he picked a fight with Canada, the US’ long-time ally, with which it shares an 8,891km land border.

And how would the Australian government, before and/or after the next election, respond?

At the moment, Trump appears to be two parts schoolyard bully (tariffs and bluster), one part 17th century king (executive orders aplenty) and one part Roman emperor (with designs on Greenland, the Panama Canal and, yes, Canada).

Perhaps the rest of the world comes to an explicit or implicit agreement to build and maintain multilateral trading partnerships to reduce the potential and actual impact of a volatile and demanding United States.

Or individual countries might try to curry favour with the US administration by deciding to play Trump’s game, for the short-term financial benefits that could accrue.

Individual companies would be well-advised to meaningfully and quickly diversify their international customer bases, much as many had to do when China put tariffs on Australian products in 2020.

What’s next?

Economic types have long said that when the US sneezes, Australia (and other countries) catch a cold. While inflation is the immediate threat, any significant disruption to trade could risk global economic growth, too.

With my investor’s hat on, the immediate impact will be on the profitability of businesses with significant cross-border trade between those jurisdictions. There aren’t many ASX-listed businesses selling much from US factories into Canada or Chinese plants to the US, thankfully.

We should prepare for more global market volatility, though, as investors try to work the announced and potential changes into their assessment of value. The ASX fell 2% out of the gate this morning. I don’t do predictions, but I think we can assume we should expect the unexpected, from here.

Oh, and a reminder that Trump has only been in office for 2 weeks. It’s going to be a helluva ride.

While the pundits focus on next week’s interest rate move by the Reserve Bank, the job market is the strongest it’s been for a long time. Alan Austin reports.

The latest figures from the Bureau of Stats (ABS) show the workforce has expanded by more than 3% in each of the last three years. This is unprecedented since the Bureau began keeping records.

Those rises were 3.35% in 2022, 3.19% in 2023 and 3.15% last year. That expansion of 1.38 million new workers in three years may well be the greatest in the developed world, relatively speaking.

That this has happened without a blow-out of the jobless or even a dip in the participation rate is quite remarkable.

The only other time Australia registered two straight years of workforce expansion above 3% was in 1986, when the jobless rate was 8.36% and the participation rate (see below) a mere 61.93%.

More jobs for more applicants

Of the extra 919,500 Australians in the workforce in just the last two years, the vast majority went into paid jobs.

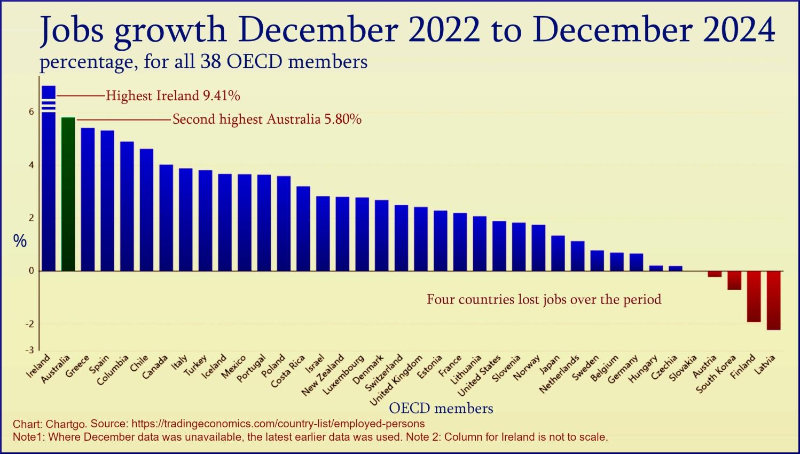

According to the data at Trading Economics, only four of the 46 nations comprising the Organisation for Economic Cooperation and Development (OECD) and the G20 enjoyed employment growth over those two years above 5% – Ireland, Australia, Greece and Spain. Australia ranked second.

Australia’s jobless rate has remained below 4.25% for the entirety of the Albanese Government and, in total, for 37 months. That has not happened since ABS records began in 1966. The female jobless rate has been below 4.1% throughout the current term, also a first.

December’s unemployment rate of 3.98% now ranks ninth in the OECD. That’s up two places from the previous year, easing ahead of the Czech Republic and, for the first time ever, Norway. That compares with ranking 23rd in June 2020.

Jobs by Prime Minister

The tussle between political parties over which administration generated more jobs is no longer close. Albo is streets ahead.

These are the rankings on jobs created per year as a percentage of employed workers:

Anthony Albanese:

3.13%

Bob Hawke:

2.48%

John Howard:

2.37%

Malcolm Turnbull:

2.31%

Paul Keating:

2.02%

Scott Morrison:

1.93%

Kevin Rudd:

1.60%

Julia Gillard:

1.44%

Tony Abbott:

1.35%

Malcolm Fraser:

0.83%

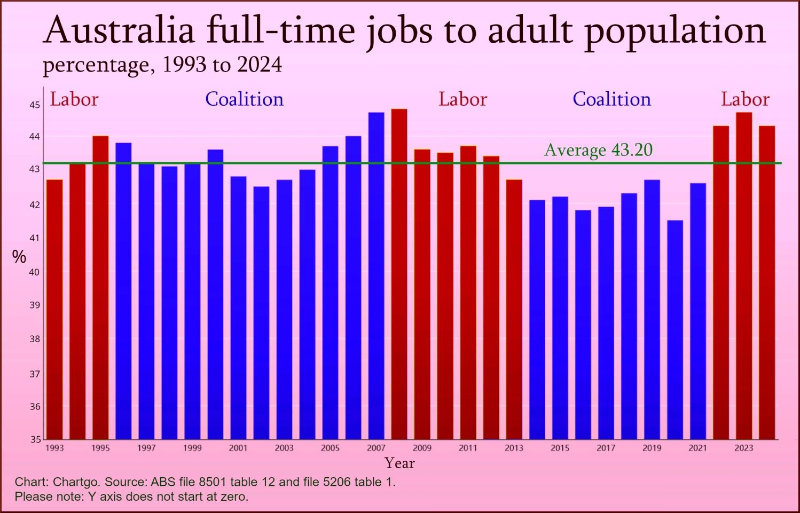

Surge in full-time jobs

Full-time jobs as a percentage of the adult population hit a 34-year high annual average of 44.74% in 2023. Last year’s 44.30% was almost as strong. The last three years have all exceeded 44.30%, well above the long-term average of 43.20%. The Coalition averaged just 42.14% in its recent eight-year reign.

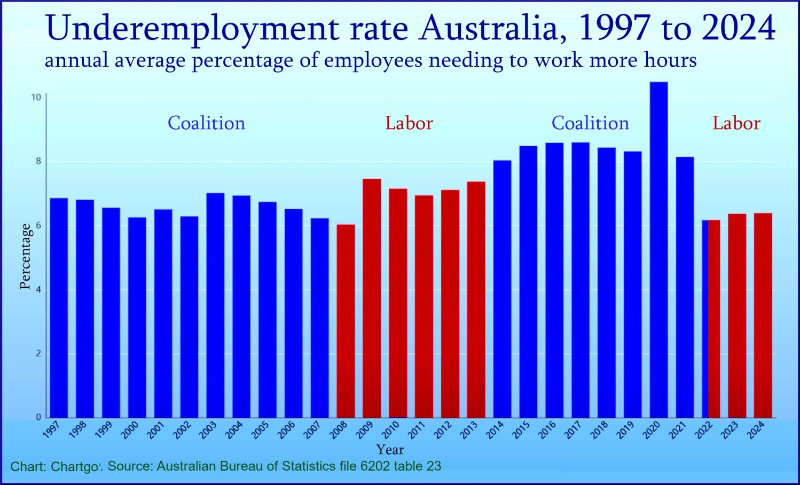

The flip side of this is the underemployment rate – the proportion of the labour force with jobs but working insufficient hours for a satisfactory income.

Through the recent Coalition period, this fluctuated between 7.5% and 13.0%. It has now settled between 5.8% and 6.7%.

Participating in the economy

For some decades the difficulty of finding a job discouraged potential workers from even signing up to look for one. This was quantified by measuring all workers plus job seekers as a percentage of the population – and called the participation rate.

This fluctuated between 62 and 65% through the Howard years and between 64 and 66% during the more recent Coalition period.

Those days appear gone. The participation rate hit an all-time monthly high of 66.71% in March 2023, then two more record highs later in 2023. Last year, this reached three all-time records, including December’s 67.13%.

The figures also show that there are more jobs for 15 to 24-year-olds.

Youth and young adult unemployment was 9.05% in December, with the rate steadily declining. This has been below 10% for the last nine months. That compares with the 12.49% average through the Turnbull period and 12.02% under Morrison.

Debunking jobs myth

Canadian economist David Card won the Nobel Prize for economics in 2021 for demonstrating that raising minimum wages doesn’t cost jobs and that immigration doesn’t lower incomes of native-born workers.

He and other Nobel laureates, including Claudia Goldin, Paul Krugman, and Joseph Stiglitz, have claimed – controversially – that governments directly shifting wealth and income from the top to the bottom is actually constructive in achieving desired economic outcomes for all citizens.

It’s hard to find a better example of Card’s theories in practice than Australia under Albanese and his treasurer, Jim Chalmers.

They have aggressively increased pensions and benefits, pushed for higher minimum wages, shifted the tax rates in favour of low-income workers, made it easier to prosecute wage thieves, handed cash to families to help pay energy bills and employed more government workers in strategic sectors. All while allowing high migrant inflows. This is Card’s fever dream.

That said, there is still much work to be done to reduce the overall cost of living, halt the ever-increasing housing costs and reduce inequality.

Australia is now the only economy in the world in budget surplus, with triple-A credit ratings and continual GDP growth for the last ten straight quarters. It is also the world’s only economy with a jobless rate below four percent, inflation below three percent, and median wealth per adult above US$250,000.

Australians are among the wealthiest people on the planet yet life has never felt harder for many. How can this be? asks Harry Chemay.

A new research paper has highlighted the plight of middle Australia, which has, over the past two decades, experienced a fall in economic circumstances relative to both low and high-wealth households.

This squeezing of middle Australia coincides with and exacerbates, the cost-of-living crisis of the past few years, mostly borne with outward stoicism and an irreverent sense of humour.

Not without good reason has ‘cozzie livs’ entered the Australian lexicon, as rising living costs post-COVID have impacted all aspects of life Down Under, from renting to health care to the ability to put enough food on the table for some.

Increasing household financial stress is further evidenced in recent data from the Australian Bureau of Statistics (ABS), which indicates nearly 1 million workers (almost 7% of employed people) now have more than one job.

It might be tempting to presume that it is lower-skilled workers who are being forced into a ‘side hustle’ out of economic necessity, but the data reveals instead that professionals dominate by number, with more than 300,000 currently holding multiple jobs, a rate of over 8%, as the below chart shows.

Source: Australian Bureau of Statistics, Multiple Job Holders, Sept 2024

Life has never felt harder for middle Australia, yet we are, on average, amongst the richest people on the planet. How can these two opposing statements co-exist and both be true?

The Melbourne Institute’s Applied Economic & Social Research Centrepaperdelved into wealth inequality in Australia for the period 2002 to 2018. By using this pre-COVID period, it reveals longer-term factors predating, and thus not influenced by, the pandemic that shaped changes in wealth inequality since the early 2000s.

Using a survey run by the Melbourne Institute, one that has tracked the changing economic and social circumstances of the same participants since 2001, the researchers looked at household wealth in 2002 and then every four years thereafter until 2018.

All components of household wealth were considered, including financial assets such as superannuation, bank accounts, shares and other investments. Non-financial assets incorporated the primary residence (if a homeowner), together with any investment and holiday properties, business assets, collectibles and vehicles. Liabilities such as mortgages, credit card debt, business debt and educational loans (HELP and VET) were captured but deducted from assets to focus on net wealth outcomes.

The outputs were then divided into different wealth groups to primarily capture high-wealth households (those in the top 90%), middle-wealth households (at the middle 50%) and low-wealth households (in the bottom 10%).

The study’s results indicate that low-wealth households saw their net wealth increase from $15,313 in 2002 to $28,000 in 2018 on average, an increase of 82.9%.

Middle-wealth households saw a lift from $340,623 to $520,300 over the same period, a lift of 52.7%, while high-wealth households experienced an increase in net wealth from $1,349,548 to $2,224,400, growing 64.8% in that time.

Importantly, the researchers noted that the absolute gap between different groups diverged over the 16-year period. While the gap between high and low-wealth households increased by 64.62%, and the gap between middle and low-wealth households grew by 51.36%,

the largest rise was between high and middle-wealth households at 68.90%.

The report noted, in appropriately neutral academic speak, that there “is some evidence here of a ‘disappearing middle’ as the relative wealth position of those in the middle of the wealth distribution worsens”.

Housing the driver

To understand the factors driving this ‘disappearing middle’, the researchers then analysed net financial wealth and net property wealth separately.

In financial wealth terms, low-wealth households increased their circumstances on average from $2,775 to $9,200 over the 16 years, a change of 231.6%. The researchers noted superannuation as a possible reason for this significant uplift. Middle-wealth households increased their financial net wealth from $75,989 to $152,900, a 101.2% uplift. High-wealth households saw an increase in net financial wealth from $609,403 to $934,766 on average, an uplift of 53.4%, with the Global Financial Crisis of 2007-08 disproportionately impacting this group.

Turning to property wealth however, the results essentially invert. The low-wealth households, on average, had zero property net wealth at every survey point across the 16 years, evidencing the difficulty in becoming property owners for lower-income households.

Middle-wealth households saw a lift in net property wealth from $221,279 to $290,000, a rise of 31.06%. High-wealth households, in contrast, saw net property wealth rise from $737,598 to $1,250,000 on average, a lift of 69.47%.

The chart below depicts the net wealth positions of each household type across financial, property and total net wealth across the study period.

Source: author’s analysis based on data in the HILDA working paper (2024)

In 2002, property wealth for high-wealth households was 3.1 times that of middle-wealth households. By 2018, it had increased to 3.4 times, and the absolute dollar gap in net property wealth separating these two groups had increased from $332,000 to $1.1 million.

This ‘disappearing middle’ phenomenon appears to be exacerbated by ever-escalating residential property prices and the increasing debt burden carried by middle-income Australians to enter, and stay in, the property market.

The Melbourne Institute paper is but the most recent in a long line of research that all points to the same underlying cause: high and rising residential property prices, relative to incomes, that over time,

concentrates property wealth in the hands of fewer, generally older, households.

With $11 trillion in residential property compared to $4 trillion in superannuation, it is property that has an outsized influence on Australian household wealth and who holds it.

This distribution of wealth is linked to declining property ownership, particularly in younger households, with the researchers noting that for the adult population, the share of those owning no property at all (the ‘property poor’) increased from 29% to 32%.

Growing property wealth inequality is detectable at the other end of the age spectrum, too. While those 65 and over with no property increased from 32% to 34% during the study period, those with two or more properties increased from 13% to 15%.

As lead author of the paper, Dr Melek Cigdem-Bayram noted:

“Australia’s worsening housing affordability crisis is locking people out of homeownership – a traditional path to economic stability for middle-income earners. As wealth inequality is increasingly concentrated in fewer hands, it entrenches economic instability and exacerbates poverty.”

The acceleration of that trend since the early 2000s has served to inflame the Housing Hunger Games that is Australia today.

The Big Four banks are betting the Australian Bureau of Statistics on Wednesday will deliver the verdict that the RBA has been wrong on interest rates. Not that they’d dare phrase it that way, says Michael Pascoe.

It’s a brave soul who bets on what ABS statistics might be, but that’s what the money market in general and our big banks in particular do. They are making a big bet that this Wednesday’s CPI numbers will show the RBA has got monetary policy wrong, that rates should have been cut in November, if not considerably earlier.

Three of the Big Four reckon the much-ballyhooed “trimmed mean” inflation measure will come in at 0.5% for the quarter. The fourth bank (Westpac) is only a bee’s appendage higher by rounding up to 0.6.

Averaging the four, the alleged underlying inflation measure over the past half year is expected to annualise at 2.5%, right smack in the middle of the target the RBA seems to have adopted since swallowing the dubious Treasury review of its operations.

As for the “headline” CPI, the thing our central bank is actually mandated to target but ignores, three of the four tip it to be up 0.2% for the second consecutive quarter, making 2.4% over the past year and just 1.6% annualising the last six months.

So why didn’t the RBA trim rates in November? Because it does not have a good handle on what the economy is doing, relying instead on dud modelling, just as it has no idea of what the NAIRU (non-inflation-accelerating rate of unemployment) might be.

While deciding to keep the monetary screws turned at its December 10 meeting, the RBA board was sticking with its forecast of trimmed mean inflation for 2024 being 3.4 per cent and not hitting its 2.5 per cent nirvana for another two years.

Of course, all the commercial banks’ highly-paid forecasters could yet be proven wrong on Wednesday, with the RBA the only one marching in step, but I suspect the Martin Place mandarins are feeling a little nervous about the figures.

As the CBA economics team put it:

The December quarter CPI report will make or break the case for the RBA Board to reduce the cash rate at their next meeting.

The CBA is our biggest bank and therefore, through its customers, the mob that should have the best feel for what is happening. The economics team highlighted that there have been growing signs that the disinflationary pulse firmed over the past two months.

“For one, both the October and November CPI reports contained strong price signals confirming this trend,” the bank reported. “And price signals from various timely consumer and business surveys also corroborate this trend.”

RBA relies on modelling

The RBA board had both of those ABS monthly CPI figures to consider at their meeting last month but stuck firm with their modelling.

Should the December quarter trimmed mean print at 0.5 or 0.6, the opportunity is there for the Governor to spin it as our mighty central bank’s great victory over inflation, proving that keeping rates where they were set in November 2023 was exactly the right medicine Australia needed and here’s a 0.25% rate cut to reward all those have been suffering for doing such a good job of suffering.

That’s much more palatable than putting it the way the CBA did when making its annualised trimmed mean forecast:

“That is to say, underlying inflation over the second half of 2024 tracked at the midpoint of the RBA’s inflation target.”