In his first term as president of the United States, Donald Trump launched a trade war against China. In his second term, he has expanded that trade war to many countries around the world.

In a ceremony outside the White House on April 2, which the US president dubbed “Liberation Day”, Trump announced sweeping new tariffs on dozens of countries, including high taxes on imports from top US trading partners: 54% on China, 46% on Vietnam, 25% on South Korea, 24% on Japan, and 20% on the European Union.

Trump falsely claimed that these tariffs were “reciprocal”, but they were actually unilateral.

Surging inflation in North Korea has some people complaining that they need to carry a backpack full of cash just to go shopping, residents in the reclusive country told Radio Free Asia.

Despite government attempts to tightly control prices, the cost of many items on informal markets called jangmadang, which became part of the economy after the famine that hit North Korea in the 1990s, have steadily risen.

North Korean authorities initially forbid jangmadang, but they gradually allowed the markets because they provided a means for people to survive. Many women in particular have set up stalls and small businesses to earn money for their families because the salaries their state-employed husbands receive is so low.

But over the past two years, the price of eggs, sugar, pork, rice and cooking oil have jumped twofold to fivefold, according to two sources from Yanggang province.

North Korean customers get assistance at a supermarket in Pyongyang, North Korea, on Sept. 12, 2018.(Kin Cheung/AP)

The main reason appears to be a shortage of supplies and the depreciation of the North Korean won against the Chinese yuan and U.S. dollar, which makes goods more expensive in local currency, the sources say.

“Market prices have jumped at least twofold and, in some cases, more than fivefold,” said a Yanggang province resident who requested anonymity for security reasons. “Now, instead of carrying a money pouch to the market, people literally have to bring a backpack full of cash.”

North Korea doesn’t report consumer price data, so examples of specific products reflect the changes.

For example, a kilogram of sunflower oil, used for cooking, has nearly tripled to 75,000 won over the past two years, while sugar has jumped fourfold to 40,000 won. A kilogram of pork has more than tripled to 87,000 won.

Since 1,000-won notes are commonly used for daily transactions, buying a kilogram of sugar would require a stack of 40 such bills. Smaller bills would require even more.

North Korea is chronically short of food, and most people struggle to get food on their tables amid poor harvests and a weak economy still recovering from COVID-19 shutdowns. Every year, people starve to death, experts say.

Also, prices appear to have increased after the government raised wages in January 2023.

In North Korea, nearly everyone’s salaries are set by the state. In 2023, workers’ base salaries were raised from 2,000 won a month to 30,000 won.

The apparent goal of this plan was to raise wages while keeping prices stable. Authorities wanted to encourage workers to rely on their salaries for living expenses rather than engaging in side businesses or money-making activities in the jangmadang markets.

However, because of the widespread shortages of food and many other goods, the plan failed. On jangmadang markets across the country, prices have been steadily climbing, residents say.

Two years ago, before the wage hikes, a kilogram of salt cost 500 won, but now it goes for 2,000 won. A carton of eggs has risen from 800 won to 2,000 won, residents say.

Footwear is also more expensive. Before the wage hike a pair of sneakers made at the Sinuiju Shoe Factory sold for 19,800 won, but now they cost 170,000 won on the black market.

“As wages have risen, so have the prices of all other necessities, making it unclear why the government decided to raise wages in the first place,” he said. “Instead of improving people’s livelihoods, the wage increase has only made daily life even more difficult.”

A party official from Yanggang province who also requested anonymity said the price of rice has nearly doubled to 9,400 won per kilogram in the jangmadang markets.

Tobacco and cigarette prices have surged. Last March, a kilogram of “Yanggang wild tobacco” cost 400,000 won, but now it has soared to 2.5 million won.

“To buy just 1 kilogram of tobacco, you would need 500 of North Korea’s highest-denomination 5,000-won bills,” said official said.

Weaker won

Meanwhile, the domestic currency has weakened against the U.S. dollar and Chinese yuan, which are widely used in the markets — despite authorities’ attempts to restrict their use.

It has also raised the price of goods if customers pay in won.

Before the 2023 wage hike, 1 Chinese yuan bought 1,260 won and 1 U.S. dollar equaled 8,500 won on the black market. But now, a yuan is worth about 3,500 won and a dollar is worth 24,000 won.

“The North Korean currency has become so worn out that it is barely recognizable, and with prices skyrocketing, people have no choice but to use Chinese yuan,” said party official said.

Using foreign currency has even become a status symbol.

“Among young and wealthy people, a common way to show off is to say, ‘I don’t play with North Korean money,‘” the official said. “Those with financial means only use Chinese yuan or US dollars, while North Korean currency has essentially become the currency of the poor.”

Edited by Malcolm Foster.

This content originally appeared on Radio Free Asia and was authored by RFA Korean.

When investing, as in horror films, the most terrifying villains are the ones we thought were dead. Stagflation that economic nightmare of the 1970s characterized by stagnant growth paired with persistent inflation was supposedly dead and buried decades ago. But like any good movie monster, it’s clawing its way back to the surface, and Americans need to prepare for its return.

The warning signs are unmistakable. Despite the Federal Reserve’s aggressive rate-hiking campaign over the past two years, inflation remains stubbornly above target. February’s Consumer Price Index showed prices still rising at 3.2%, while previous months have delivered unwelcome upside surprises. Meanwhile, GDP growth has begun to sputter, at just 1.6% in the first quarter, down sharply from 3.4% in late 2023.

Even more alarming, the Atlanta Federal Reserve’s closely watched GDPNow forecast model has recently slashed its second-quarter growth projection. When the Fed’s regional banks signal economic deceleration while inflation persists, the stagflation alarm bells should be ringing loudly.

This toxic combination represents the classic stagflation recipe: prices rise faster than paychecks while economic momentum simultaneously loses steam. Conventional economic models struggle to address this scenario, as policies that fight inflation typically hamper growth, while growth-boosting measures often exacerbate inflation.

Stagflation is particularly pernicious because it confounds traditional economic remedies. When inflation and unemployment rise simultaneously, policymakers face an impossible choice between fighting one problem while exacerbating the other.

The warning signals extend beyond inflation and growth statistics. Federal agencies have begun implementing hiring freezes and initiating workforce reductions as budget pressures mount. The Bureau of Labor Statistics reported that federal government employment declined by 5,000 jobs in January alone, with more cuts potentially looming. These job losses contribute to economic stagnation without addressing the underlying inflation problem.

Meanwhile, fiscal austerity measures designed to address budget deficits have reduced government spending across multiple agencies. While necessary for long-term fiscal health, these spending cuts remove economic stimulus precisely when private sector growth is already slowing, amplifying stagflationary pressures.

Perhaps most concerning for millions of Americans is the resumption of student loan payments after a three-year pandemic pause. With average monthly payments of $200-$300, the Department of Education estimates that borrowers collectively face over $7 billion in monthly payments—essentially a massive consumer spending tax that dampens economic activity without addressing supply-side inflation drivers. For many households, these payments come on top of significantly higher housing costs, energy bills, and grocery expenses.

Labor markets offer another concerning indicator. Despite headlines touting low unemployment, job growth has slowed considerably. In contrast, wage growth hasn’t kept pace with inflation in many sectors. Companies are increasingly caught in a vise between rising costs and consumers unable or unwilling to absorb higher prices.

The roots of our current predicament are not hard to identify. Years of extraordinary monetary accommodation followed by trillions in pandemic stimulus created excess liquidity. Supply chain disruptions, geopolitical tensions, and energy price volatility fueled the fire. We’re left with an economy where growth is cooling, but prices refuse to follow suit.

For investors, the stagflation playbook requires a dramatic departure from conventional wisdom. The investment landscape of the next several years will reward those willing to adapt and punish those clinging to outdated strategies.

First and foremost, commodities deserve a prominent place in any stagflation-resistant portfolio. During the 1970s stagflation, the S&P GSCI commodity index delivered a staggering 586% return over the decade. Gold performed even more spectacularly, rocketing from about $269 per ounce in 1970 to over $2,500 by 1980.

Why do commodities shine in stagflationary environments? They represent tangible assets with intrinsic value that tend to rise with inflation. Hard assets become monetary safe havens when currencies weaken through policy interventions or economic uncertainty.

Treasury Inflation-Protected Securities (TIPS) also merit serious consideration. Unlike conventional bonds, which suffered brutal losses during the 1970s with approximately negative 3% annualized actual returns, TIPS adjust their principal value based on the Consumer Price Index. This built-in inflation protection can preserve purchasing power when conventional fixed-income investments crumble.

Investors should pivot decisively toward defensive sectors within equities—consumer staples, healthcare, and utilities. These industries provide essential goods and services people need regardless of economic conditions, and many possess the pricing power to pass inflation through to consumers. During past stagflationary episodes, U.S. consumer staples delivered average quarterly returns of +7.9%, while consumer discretionary stocks declined by 1.3%.

The dangers of stagflation extend far beyond investment portfolios. The most insidious aspect of stagflation is how it methodically erodes societal living standards. When prices rise faster than wages for extended periods, everyday purchases become increasingly painful. Essentials consume a growing share of household budgets, leaving less for discretionary spending, savings, or investments in the future.

The psychological toll shouldn’t be underestimated either. During the 1970s stagflation, consumer confidence plummeted to record lows as Americans believed economic malaise was permanent. This pessimism affected everything from marriage rates to entrepreneurship, creating a downward spiral of reduced risk-taking and investment precisely when the economy needed it most.

Stagflation particularly punishes those on fixed incomes especially retirees whose pension or Social Security benefits fail to keep pace with true living costs. It also penalizes savers, and those with traditional fixed-income investments, who watch their purchasing power diminish monthly.

For younger Americans already grappling with housing affordability challenges and now facing resumed student loan payments, stagflation compounds financial stress. Many millennials and Gen Z workers entered a labor market already characterized by stagnant real wages; persistent inflation threatens to erase what little progress they’ve made.

Businesses suffer, too, caught between rising input costs and price-sensitive consumers. Profit margins contract, leading to reduced hiring, investment cuts, and, in many cases, layoffs. Small businesses with less pricing power and financial cushion are particularly vulnerable, potentially leading to increased market concentration as only the largest firms survive.

Stagflation will eventually end through successful policy intervention or economic adjustment, but the transition may prove lengthy and painful. The 1970s stagflation persisted for nearly a decade before Paul Volcker’s Federal Reserve crushed inflation, with interest rates approaching 20%.

Today’s policymakers face a similar dilemma, but even higher debt levels constrain their options. The Fed has signaled reluctance to cut rates while inflation remains elevated, yet maintaining restrictive policy risks further dampening growth—the very definition of our stagflationary trap.

Preparation means building financial resilience for individuals: reducing high-interest debt, maintaining emergency savings, and seeking opportunities to increase skills and income potential. Homeowners with fixed-rate mortgages benefit from what amounts to an inflation discount on their housing debt, while renters may need to budget more aggressively as housing costs continue climbing.

Though difficult, stagflation is ultimately a surmountable challenge. Following the 1970s ordeal, America entered a period of extraordinary growth and prosperity. The pain of adjustment, while real, eventually gave way to renewed economic vitality. The same can happen again if we make the difficult choices necessary to restore price stability while fostering sustainable growth.

The stagflation monster may be back, but America has faced and overcome economic challenges throughout its history. By understanding the nature of the threat and taking appropriate actions both as individuals and as a society, maybe we can weather this economic storm and emerge stronger on the other side. The alternative of ignoring the warning signs until a crisis forces our hand will only prolong the pain and deepen the eventual reckoning. The time for clear-eyed assessment and deliberate action is now.

Whilst observing the questionable economic decisions of our elected officials, it seems that no one will bury stagflation back in the graveyard.

US President Trump ran his campaign on a pledge to “make America affordable again,” following the inflationary crisis during Biden’s administration. But since the beginning of his presidency, the cost of living crisis, including the cost of staple grocery items and rent, has persisted.

Peoples Dispatch spoke to economist Richard Wolff, who outlined that “prices are shaped by many factors, and only a few of those are under the control of any president.”

“Trump did what American politicians usually do, which is take a cheap shot at his political enemies by blaming them for something bad going on in this case, inflation,” Wolff said.

Did you know that the government can never run out of money, taxes don’t fund its spending, the national debt isn’t a debt, and printing money doesn’t cause inflation? Probably not, because your parents, teachers, politicians, and favorite journalists have always told you the opposite.

For most of my life, I didn’t know either. I have two PhDs, and if one of them were in economics, it wouldn’t have helped. The only people who know how government finances work are central bankers (who won’t tell you), traders with hands-on experience of the failure of economic norms, and those who stumble across their work (which I explain below).

Everyone else, from New York Times economists to the leaders of both major parties, reinforce common falsehoods, which may be why the economy is brutal and crashes every ten years. Some of these experts lie, others don’t want to rock the boat or jeopardize their careers, but most don’t have a clue.

That is why, if there is a conspiracy to stop us learning “why the government can never go broke,” for example, so that we don’t ask for nice things like public healthcare, climate action, and a basic income, it is almost effortless. Most people automatically treat the government like a big household that is subject to the same financial rules as themselves—balance income with spending, save for a rainy day, and avoid debt.

As responsible adults, that is our lived experience—the hard truth of budget living that accompanies adulthood—and it continues to guide every financial decision we make. When analogized to the government, disagreement appears infantile to us “adults in the room” who assiduously calculate how to pay for government programs with taxes and cuts.

What eventually caused me to stop basing my beliefs on assumptions, hearsay, and intuition were questions like “where does money come from?” And, how did the trillions of dollars that exist today actually get here? My intuition had only supported the ridiculous notion that money is an eternal object that circulates in the economy and cannot be created or destroyed.

In my examination of what seemed like a scholarly question, I discovered what may be the greatest cause of suffering in the developed world— politicians who falsely declare that a government “cannot afford” something or has “reached its debt ceiling” are creating opposition to social spending that would save lives and could save the planet we live on.

The remainder of this article will provide you with the knowledge to reject their misinformation and, I hope, facilitate the greatest societal change of the 21st century.

Where Does Money Come From?

Take the United States as an example. Every U.S. dollar in existence was created by the U.S. government (or by banks with government licenses), and this exclusive right to create the dollar is enshrined in the U.S. Constitution. It is even called a Federal Reserve Note to tell you it was created by the government’s bank.

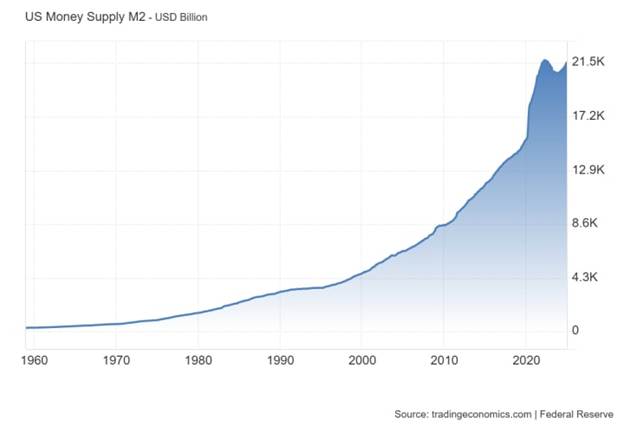

The first dollar was created in 1792 and trillions have been created since then. In fact, there are twice as many dollars in existence today compared to ten years ago (see graph). Although much of the new money is bank credit, the rest is created when the government passes spending bills.

Most national governments are currency issuers, including the U.K., Australia, and Canada, although some are not (e.g., European Union states such as Greece). Localities such as U.S. states also do not create currency and require some form of income.

This power to issue currency means that every statement from a politician, economist, or media personality about the government “running out of money” or being “unable to pay its bills” is a lie.

The Government Can Never Go Broke

In a rare and unreported admission, the Federal Reserve confirmed that the U.S. government issues the dollar and can never run out.

As the sole manufacturer of dollars, whose debt is denominated in dollars, the U.S. government can never become insolvent, i.e., unable to pay its bills. — Federal Reserve Bank of St. Louis

Alan Greenspan also said the following under oath in front of Congress (see video for context).

There is nothing to prevent the federal government from creating as much money as it wants and paying it to somebody. — Alan Greenspan (Federal Reserve chairman, 1987–2006)

Another Fed chairman, Ben Bernanke, said something similar when he described how the government bailed out the banks after the 2008 financial crisis (see video below). As I said in the introduction, central bankers know how it works. They just almost never tell you.

Taxes Do Not Fund Spending

In the previous video, Bernanke explained that tax money was not used to bail out the banks, and, logically, a currency-issuing government does not need taxes to fund itself.

The proceeds from taxation and bond sales are technically incapable of financing government spending […] modern governments actually finance all of their spending through the direct creation of high-powered money. — Professor Stephanie Kelton

It makes no practical sense for governments to wait until they have accumulated enough in taxes. Or did you think the Treasury was waiting for your grandmother’s taxes to arrive before they could buy a warship?

Rather, they create money as they spend. As Bernanke explained, the government makes a payment by instructing the Federal Reserve to increase the number of dollars in a bank account. This happens by keystrokes on a computer. It doesn’t even need to be printed.

Taxes Are Deleted

There is a veiled admission from the Federal Reserve about the fate of our taxes. Essentially, they acknowledge in footnote 1 here that taxes paid to the U.S. Treasury are no longer part of the money supply (i.e., deleted).

Governments create money by spending and extinguish it via taxation. — Professor James K. Galbraith (former executive director of the Joint Economic Committee of Congress)

Why Tax At All?

Unfortunately, taxation is necessary. When the government creates dollars, it needs you to value and accept those dollars as payment for your goods and labor. The government does this by forcing you to pay taxes only in dollars, which means that you have to obtain dollars from somewhere.

In other words, giving value to the government’s currency is the core reason for taxes, but there are other reasons, such as to reduce the money supply and to punish problematic industries (e.g., polluters). Funding government spending is not one of the reasons. Indeed, governments have to create and spend money before anyone can even pay their taxes.

Printing Money Does Not Cause Inflation

Intuition tells us that creating money reduces its value by the same amount, but this leads to the ridiculous notion that the first dollar ever created was as valuable as the collective trillions in existence today. It also forgets that the money supply is increasing all the time, usually without noticeable inflation.

In my case, I held this myopic belief about inflation because I saw a photograph of a wheelbarrow of money in a 7th grade history class about Weimar Germany and I assumed that correlation means causation.

The conventional wisdom that printing money causes inflation is not true. — Professor John T. Harvey

Public domain photo

Although money creation could expedite inflation, it was not the cause of the historical examples that most people cite, such as Weimar Germany and Zimbabwe. Rather, the inflation was caused by supply shortages, or foreign debt, and money was created after to maintain the public sector.

The causation is that inflation increases the nominal need for cash and reserves, not that increased cash causes inflation. — Warren Mosler (hedge fund executive and professor of economics)

We can describe inflation with the equation, MV = Py. While increasing the money supply (M) could increase prices (P), the money may be saved, reducing the rate of spending (V). Alternatively, if the money is spent, businesses will seek to accumulate it by hiring workers and producing more goods and services (y). In either case, prices do not increase.

Inflation can occur if there is a lack of resources or labor, which is why it’s usually a supply issue, and why quintupling the money supply in the past thirty years has not brought about Armageddon.

The National “Debt” Is Not Debt

A national “debt” of more than $35 trillion sounds scary. So scary that people are paid great deals of money to tell you how scary it is. The more afraid you get, the less likely you are to want public healthcare or climate action. How could we possibly afford that?

Much of this “debt” is Treasuries, which are savings accounts with the U.S. government that earn interest. Countries like China and Japan buy Treasuries because they earn dollars through trade and have nowhere better to put them. What this tells us is:

Holders of U.S. “debt” do not want it repaid for the same reason that you don’t want your bank to close your savings account.

The government does not need the money. It creates all that it needs, and it created every dollar that has since been used to buy Treasuries.

If the government wants to eliminate this “debt” it can phase out Treasuries and deposit the money into checking accounts.

If anyone wants to withdraw their money, the government can create/print the withdrawal amount and give it to them (see video).

So the national “debt” is not a debt. When the government creates money, it offers people the chance to buy Treasuries of equal value. These Treasuries, plus cash left in the economy, are the money supply (the total of every budget deficit in history). Eliminating it, such as with less spending and more taxation would eliminate the money supply.

Nevertheless, fear-mongering about the “debt” has persisted for at least 88 years, when it was a thousand times smaller (see video). Normally, when someone predicts the apocalypse, they are discredited when their prediction fails.

Budget Surpluses Cause Recessions

A budget deficit occurs when the government has created and spent more money into the economy than it has removed in taxes. A budget deficit therefore puts more money into your pocket than it takes out.

A budget surplus occurs when more money is taxed out of your pocket than is spent in. This is not good for you, and it doesn’t help the government either because taxes are not saved. But that doesn’t stop corrupt politicians from appealing to popular intuitions about “saving for a rainy day” or the fact that surplus sounds positive and deficit sounds negative.

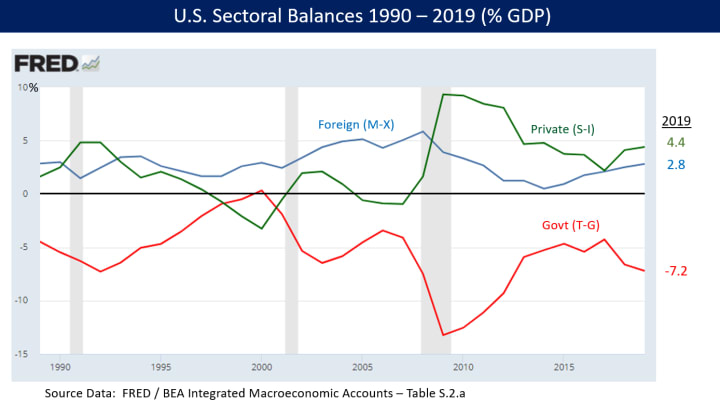

Politicians do this to discourage social spending. Furthermore, attempts to “balance the budget” or have a budget surplus cause cash-strapped people to accumulate private debt (i.e., realdebt) that is held by the wealthy donors of these politicians. Unfortunately, this situation (see graph when the green line drops below zero) almost always triggers a recession (shaded areas of the graph).

Historical data shows that a government deficit (the red line, below zero) is a private sector surplus (the green and blue lines, above zero). Basic accounting tells us that the lines balance out every year and sum to zero.

Why Learning Economics Is Important

Every time a policy is proposed that could save lives, such as public healthcare or climate action, it is belittled with the following eight words: “how are you going to pay for it?”

Liberals propose taxes or cuts that conservatives disagree with, and the two sides have argued about these imaginary financial constraints for decades while millions have died.

The truth is that the government has no financial constraints. It only has resource constraints and the risk that its spending might cause a demand for resources that exceeds the economy’s productive capacity (inflation). However, there is nearly always room to expand that capacity with construction, imports, education, and innovation.

In recent years, Modern Monetary Theory (MMT) and its advocates have popularized and informed people about the ideas presented here. Eventually, these ideas could transform society, causing it to focus less on the importance of money and more on what can be achieved with the real resources at its disposal.

It is no coincidence that every modern historical triumph, from reaching space to winning WW2, acknowledged the triviality of money. We did not say “we can’t afford to fight Germany.” Rather, we looked at what we could do with the resources we had and used money to incentivize people to contribute. A government can create as much incentive as it wants.

In my view, our collective understanding of these paradigm-changing ideas will bring about the greatest societal change of the 21st century. The imaginary financial constraints that our leadership class places upon itself will be removed. Instead of “we can’t afford that” we will say “how do we resource that?” and reduce suffering on a massive scale.

Of course, MMT already has its critics. Typically, they either do not understand the theory or do not want you to understand it. They create straw man versions to make it appear unreasonable, uncomplicated, and not the work of highly-credentialed academics and economists.

For example, you may have heard that MMT is “just about printing money,” that the theory does not consider inflation, or that it can only work while the dollar is the world’s currency (the framework applies to any currency-issuing nation).

Many of these critics have careers or ideologies that have been sustained by their support for economic models that cause a recession every ten years. Other critics have reservations about what will happen to human society if these ideas become popular. Others are wedded to conspiracy theories that impede their ability to process the information.

Dispensing with the intuitive economic falsehoods that you have grown up with should not be entrusted to people whose careers or egos are sustained by them. Rather, MMT should be learned from the academics who developed the theory, such as those listed below.

Multiple national grocery retailers are imposing limits on how many cartons of eggs consumers can purchase amid a shortage of the product and rising grocery prices across the U.S. As of Monday morning, the average price for a dozen eggs was around $7.74 — an increase of about 18 percent since President Donald Trump took office. According to a report from NBC News, many national chains…

Inflation is top of mind for many Canadian small and medium-sized businesses (SMEs) these days. A recent survey of Canadian SMEs found 90 percent of them had been impacted by inflation, and another survey of 500 Canadian accountants revealed inflation as the most significant financial threat to Canadian SMEs. With the vast majority of Canadian worker co-ops being SMEs, it’s reasonable to assume that they’re also feeling these pressures. But delving deeper into the issue suggests that while worker co-ops face some of the same challenges as conventional businesses regarding inflation, how they respond is likely to be different.

President Donald Trump signed three executive orders on Saturday following through on his promise to impose 25% tariffs on goods from Mexico and Canada and 10% tariffs on goods from China, a measure that targets the nation’s three largest trading partners. The tariffs are set to go into effect on Tuesday, according to The Associated Press. The orders contained no language allowing for…

Trump’s proposals to radically transform much of US economic and social policy are being rapidly rolled out during the first week of his administration. How much he succeeds or fails in that transformation will depend on a number of factors. High on the list of such factors is the residue of conditions and policies leftover by the Biden administration—i.e. the legacies of the Biden years. Those legacies will play an important role influencing, and perhaps even determining, how Trump may fare in implementing his plans. So what are the legacy policies and conditions?

President-elect Donald Trump is backtracking on a major campaign promise, stating in a recent interview that he cannot guarantee that he will be able to drive down grocery prices after all. In an interview with Time magazine following his being named “Person of the Year,” Trump was asked by the publication whether he still believed that his policies would be able to lower costs for consumers.

Angela Bishop has been struggling with what she describes as “the cost of everything lately.” Groceries are one stressor, although she gets some reprieve from the free school lunches her four kids receive. Still, a few years of the stubbornly high cost of gas, utilities, and clothing have been pain points.

“We’ve just seen the prices before our eyes just skyrocket,” said Bishop, who is 39. She moved her family to Richmond, Virginia from California a few years ago to stop “living paycheck to paycheck,” but things have been so difficult lately she’s worried it won’t be long before they are once again barely getting by.

Families nationwide are dealing with similar financial struggles. Although inflation, defined as the rate at which average prices of goods or services rise over a given period, has slowed considerably since a record peak in 2022, consumer prices today have increased by more than 21 percent since February 2020. Frustration over rising cost of living drove many voters to support president-elect Donald Trump, who campaigned on ending inflation.

Simply put, inflation was instrumental in determining how millions of Americans cast their ballots. Yet climate change, one of the primary levers behind inflationary pressures, wasn’t nearly as front of mind — just 37 percent of voters considered the issue “very important” to their vote. Bishop said that may have something to do with how difficult it can be to understand how extreme weather impacts all aspects of the economy. She knows that “climate change has something to do with inflation,” but isn’t sure exactly what.

In 2022, inflation reached 9% in the U.S. — the highest rate in over 40 years. That was part of a global trend. The lingering impacts of the pandemic, Russia’s invasion of Ukraine, higher fuel and energy prices, and food export bans issued by a number of countries contributed to a cost of living crisis that pushed millions of people worldwide into poverty.

Extreme weather shocks were another leading cause of escalating prices, said Alla Semenova, an economist at St. Mary’s College of Maryland. “Climate change is an important part of the inflationary puzzle,” she said.

In February of 2021, Winter Storm Uri slammed Texas, causing a deadly energy crisis statewide. It also caused widespread shutdowns at oil refineries that account for nearly three-quarters of U.S chemical production. This disrupted the production and distribution of things necessary for the production of plastics, which Semenova says contributed to ensuing price hikes for packaging, disinfectants, fertilizers and pesticides.

Food prices are another area where the inflationary pressure of warming has become obvious. A drought that engulfed the Mississippi River system in 2022 severely disrupted the transportation of crops used for cattle feed, increasing shipping and commodity costs for livestock producers. Those added costs were likely absorbed by consumers buying meat and dairy products. Grain prices jumped around the same time because drought-induced supply shortages and high energy prices pushed up the costs of fertilizer, transportation, and agricultural production. Not long after, lettuce prices soared amid shortages that followed flooding across California, and the price of orange juice skyrocketed after drought and a hurricane hit major production regions in Florida.

Though overall inflation has cooled considerably since then, the economic pressures extreme weather places on food costs persist. The Food and Agriculture Organization of the United Nations reported that weather disruptions drove global food prices to an 18-month high in October. In fact, cocoa prices surged almost 40 percent this year because of supply shortages wrought by drier conditions in West and Central Africa, where about three-quarters of the world’s cocoa is cultivated. This can not only impact the price tag of chocolate, but also health supplements, cosmetics, and fragrances, among other goods that rely on cocoa beans.

“What we have seen, especially this year, is this massive price spike,” due to abnormal weather patterns, said Rodrigo Cárcamo-Díaz, a senior economist at U.N. Trade and Development.

But the impact on consumers “goes beyond” the Consumer Price Indicator, which is the most widely used measure of inflation, said Cárcamo-Díaz. His point is simple: Lower-income households are most affected by supply shocks that inflate the price of goods as increasingly volatile weather makes prices more volatile, straining households with tighter budgets because it can take time for wages to catch up to steeper costs of living.

Rising prices are expected to become even more of an issue as temperatures climb and extreme weather becomes more frequent and severe. In fact, a 2024 study found that heat extremes driven by climate change enhanced headline inflation for 121 countries over the last 30 years, with warming temperatures expected to increase global inflation by as much as 1 percent every year until 2035. Lead researcher and climate scientist Maximilian Kotz noted that general goods, or any physical things that can be bought, broadly experienced “strong inflationary effects from rising temperatures.”

All told, the inflationary impact of climate change on cost of living is here to stay and will continue to strain American budgets, said Semenova. “The era of relatively low and stable prices is over,” she said. “Costs have been rising due to climate change. It’s the new normal.”

That’s bad news for families like the Bishops, who are simply trying to get by.

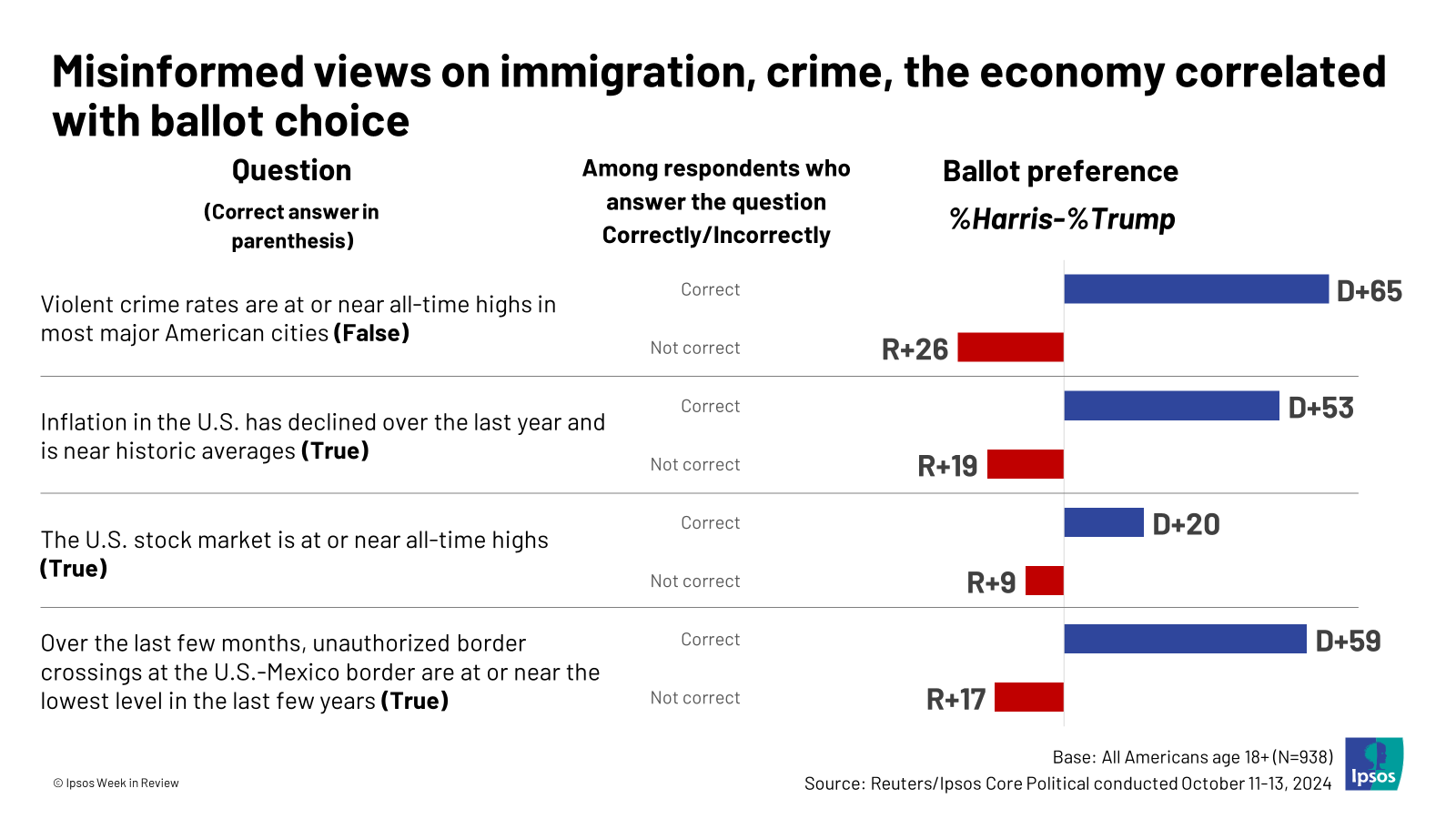

Ask voters to verify basic facts related to major political issues, and the results are depressing. An Ipsos survey from October of this year, for instance, discovered most Americans were unaware that unauthorized border crossings were at or near their lowest point over the last several years, that violent crime was not at or near all-time highs in most major cities—and that inflation was down from a year earlier and near historic averages.

The political implications of such ignorance are both predictable and striking, with more ignorance associated with greater support for Donald Trump.

Conservative media, unsurprisingly, appears to be a major culprit in the miseducation of the American public, with people whose primary media source is conservative media registering lower familiarity with reality than those who stuck mainly to other media sources. (Reliance on social media, too, was associated with less knowledge of basic facts.)

But even among those who primarily get their news from the more general category of cable/national newspapers, a third didn’t realize that inflation had declined over the past year. Voters’ lack of knowledge, therefore, cannot simply be laid at the feet of the conservative press. Corporate outlets more broadly must share the blame.

And on perhaps no other issue has corporate media’s failure to inform been more consequential than on inflation. This was, after all, arguably the key factor in the election: Inflation surged, and Democrats were pummeled.

Did they deserve this fate, though? That’s a tougher question, but one that corporate media could help the public grapple with—if only they weren’t committed to misinforming the public about the issue at hand.

Artificially spiking Trump’s economy

It would be absurd to expect the public at large to have the time or ability to do a deep dive into statistics in order to develop as accurate an image of the economy as possible. It wouldn’t be so absurd, however, to expect journalists to perform this task. After all, their essential function is to deliver high-quality, accurate information to a lay audience. Unfortunately, in reality, they often fail at this job. We might refashion an old phrase to say: There are lies, damned lies and statistics as represented by journalists.

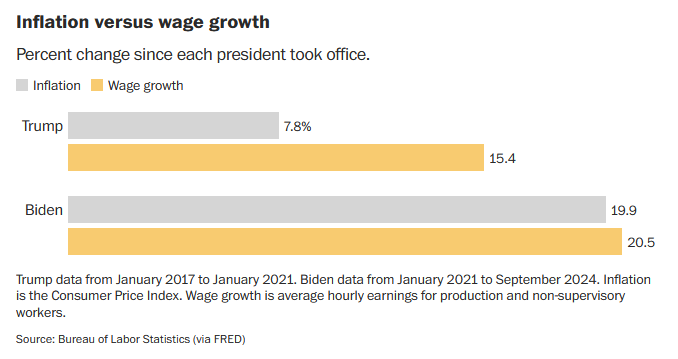

Take a recent piece by Washington Post columnist, and former economics correspondent, Heather Long (11/8/24). In it, she makes the claim that voters enjoyed much more robust wage growth under Trump than under Joe Biden, after accounting for inflation. Her column includes a chart showing wage growth outpacing inflation by 7.6 percentage points under Trump and only 0.6 percentage points under Biden.

Something important goes unmentioned here, something that might surprise a casual reader. Specifically, there was a serious and well-known—at least among experts—methodological issue that led to an artificial spike during 2020/2021 in the wage measure Long is citing. As many more low-wage than high-wage workers lost their jobs at the height of the pandemic, this measure artificially inflates wage growth under Trump and deflates it under Biden. Maybe an issue worth mentioning, if you’re making a claim about comparative real wage growth under the two.

When you chart the measure the Washington Post (11/8/24) used to show the superiority of Trump’s wage growth, it’s revealed as an artifact of people dropping out of the workforce during the pandemic (Arin’s Substack, 1/18/24).

Does Long mention this, though? No. Will the average reader be sufficiently in the economic weeds to know she is misleading them? Also no.

An unreal measure of real income

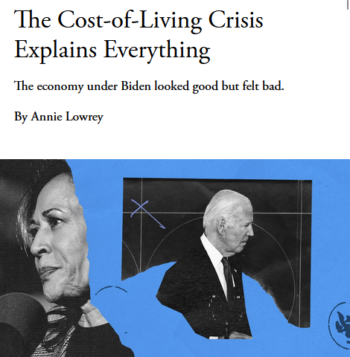

What explains everything for the Atlantic (11/11/24) is a cost-of-living crisis that disappears if you use a better measures of the cost of living.

Another offending piece appeared recently in the Atlantic (11/11/24). There, staff writer Annie Lowrey made the case that the cost-of-living crisis, and the Democrats’ inability to tackle it, explains the election results. Curiously, the media’s role in distracting the public from the remarkable achievements of macroeconomic policy during Biden’s tenure in office went unmentioned.

Lowrey at least acknowledged how impressive the macroeconomic figures have been coming out of the Covid downturn, but she asserted that this obscured a darker story: “Headline economic figures have become less and less of a useful guide to how actual families are doing.” Instead of relying solely on these numbers, Lowrey proposed consulting “more granular data” that “pointed to considerable strain.”

First among these data points was an apparent fall in real median income since 2019. As Lowrey put it, “Real median household income fell relative to its pre-Covid peak.”

What she failed to disclose was the flimsiness of the underlying measure being used. As economist Dean Baker (Beat the Press, 9/10/24) pointed out a couple months back, when the Washington Post (9/10/24) ran a piece highlighting trends in the same metric—a median income measure designed by the Census Bureau—making a comparison between the 2024 figure and the 2019 one is messy:

The problem is with the comparison to 2019, the last year before the pandemic. There was a large problem of non-response to the survey for 2019, which was fielded in the middle of the pandemic shutdown in the spring of 2020. The Census Bureau wrote about this problem when it released the 2019 data in the fall of 2020.

As a result of the non-response issue, the 2019 number is artificially inflated, and a comparison between it and more recent figures, which seem to also be inflated but to a lesser degree, is difficult at best. Othermeasures of income, meanwhile, find real income increasing for Americans since 2019. These critical pieces of information, however, are missing from the Lowrey piece.

Sloppy reporting of real problems

This is not to say that Lowrey and others who have made similar arguments don’t have a point that there are real issues facing the American public. For such a wealthy country, the US has obscenely high poverty, internationally aberrant levels of inequality, and a notoriously ramshackle welfare state.

Partially out of sheer necessity, the US welfare state was substantially boosted during the pandemic, and the unwinding of this enhanced safety net after 2021 must have had some effect on Americans’ perceptions of the economy and their own economic standing. Real disposable income, for example, spiked in 2021 due to temporary measures like stimulus checks, but then fell back to the pre-pandemic trend of growth, which may have felt like a loss to some.

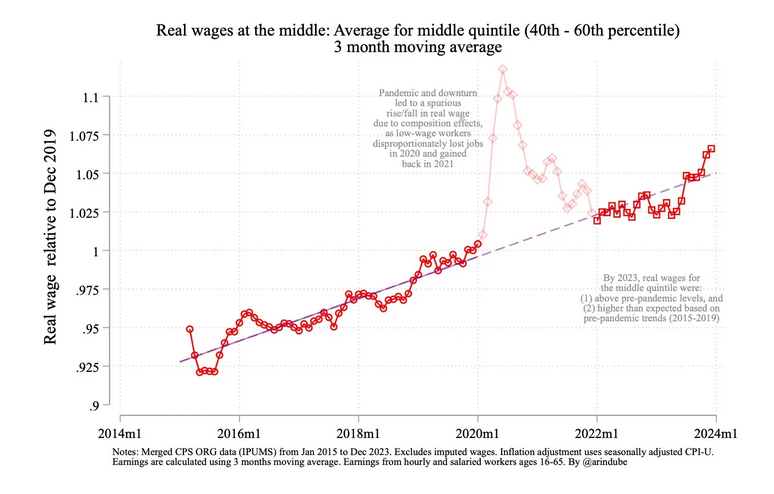

And though the Washington Post‘s Long mucked up her analysis of wage trends under the Biden and Trump presidencies, the data that we have does indicate that inflation bit into workers’ wages early in Biden’s term, with median real wage growth turning negative in 2021 and 2022. (It’s nonetheless worth noting that these wage declines were concentrated among high-wage workers, not low-wage ones.)

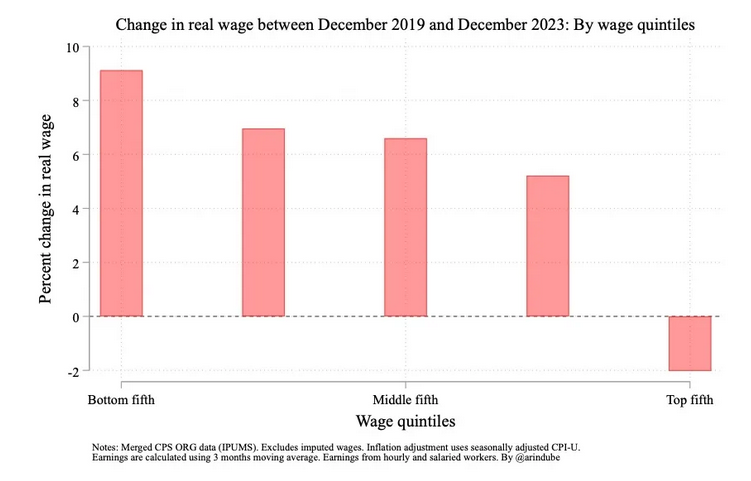

From December 2019 through December 2023, inflation-adjusted growth in wages was highest in the poorest quintile, and only negative for the top quintile (Arin’s Substack, 1/18/24).

Clearly, there are reasons for people to be angry about the economy. The issue is that imprecise descriptions of the trajectory of the US economy over recent years leave people unable to decipher how the economic situation has deteriorated, and in which ways there actually has been improvement.

Citing a flawed measure of median income to suggest that people are worse off than in 2019, for example, is careless at best. We know that, even after adjusting for inflation, Americans’ wages, disposable incomes and, perhaps most crucially, spending levels are higher today than they were in 2019. Notably, this is true across income groups, with real retail spending up for low-, middle- and high-income households.

There are many ways in which the US economy flatly fails, but addressing those failures becomes even harder when the public is misled into thinking that inflation is outpacing wages, or that real median income is actually decreasing.

For the New York Times (11/8/24), inflation affects “everyone,” whereas unemployment matters to “only a minority of the population.”

Messing up the technical details when presenting statistical information is bad enough. But corporate media misinformation goes beyond that. Recently, for instance, the New York Times (11/8/24) decided to add to the barrage of inflation misinformation by blatantly misrepresenting how inflation and unemployment affect the public. In a piece titled “How Inflation Shaped Voting,” reporter German Lopez wrote:

Why does inflation anger voters so much? Some economic problems, like high unemployment, affect only a minority of the population. But higher prices affect everyone.

This is wrong. An increase in unemployment has economy-wide effects, dragging down wage growth across the income distribution, though particularly at the bottom. In fact, the societal effects of higher unemployment seem to be much more dramatic than those of higher inflation. According to a piece from the Times (7/20/22) published back in 2022:

In a 2003 paper, the economist Justin Wolfers, then of Stanford University, found that a percentage-point increase in the unemployment rate caused roughly five times as much unhappiness as a percentage-point increase in inflation.

Had Lopez written that high unemployment directly affects a small percentage of the population, he obviously would have been on solid ground. But that’s not what he wrote.

Skewing in one direction

“There’s another fundamental cause of economic discontent that should be getting more attention: corporate media’s single-minded obsession with inflation, which has left the public with an objectively inaccurate view of the economy” (FAIR.org, 1/5/24).

These criticisms of how journalists present economic information are technical, but they are important. Notably, in each instance cited, the skewing of facts has specific political implications.

In Long’s piece, workers’ gains under Trump were exaggerated, and their gains under Biden were understated. In Lowrey’s piece, income gains under Biden were disregarded. And in Lopez’s piece, the negative impacts of increased unemployment, which the Biden administration avoided at the cost of a somewhat larger spike in inflation, were downplayed. The negative effects of inflation were played up.

It’s not hard to see how such an approach to reporting will benefit one political party at the expense of the other. This would be totally reasonable if the reporting were based in reality, with journalists sticking to the facts and representing statistics with care. But that’s not what’s happening.

Instead, journalists over the past several years have engaged in a collective freak-out over a surge in inflation, feeding the public’s pre-existing negativity bias with a hyper-fixation on rising prices in economic coverage. That this coverage has not only overshadowed coverage of more positive economic stories—such as the successes of a historically progressive stimulus bill, and the massive wage gains it has spurred—but has misled the public about basic economic facts in the process is a scandal.

Journalists should face flak for imprecision in their reporting, and should be pushed to improve when they fall short of a high standard of accuracy, especially when they occupy elite perches in the US media environment. Otherwise, an information environment polluted by conservative outlets and social media misinformation will never get cleaned up. If corporate media’s mission is truly to inform the public, they have a long way to go.

MSNBC‘s Chris Matthews, once one of the most prominent pundits on cable TV, used his post-election appearance on Morning Joe (Mediaite, 11/6/24) to demonstrate just how unhelpful political commentary can be.

Asked by host Willie Geist for his “morning after assessment of what happened,” Matthews fumed:

Immigration has been a terrible decision for Democrats. I don’t know who they think they were playing to when they let millions of people come cruising through the border at their own will. Because of their own decisions, they came right running to that border, and they didn’t do a thing about it.

And a lot of people are very angry about that. Working people, especially, feel betrayed. They feel that their country has been given away, and they don’t like it.

And I don’t know who liked it. The Hispanics apparently didn’t like it. They want the law enforced. And so I’m not sure they were playing to anything that was smart here, in terms of an open border. And that’s what it is, an open border. And I think it’s a bad decision. I hope they learn from it.

You could not hope for a more distorted picture of Biden administration immigration policy from Fox News or OAN. “They didn’t do a thing about it”? President Joe Biden deported, turned back or expelled more than 4 million immigrants and refugees through February 2024—more than President Donald Trump excluded during his entire first term (Migration Policy Institute, 6/27/24).

Human Rights Watch (1/5/23) criticized Biden for continuing many of Trump’s brutal anti-asylum policies; the ACLU (6/12/24) called those restrictions unconstitutional. How can you have any kind of rational debate about what the nation’s approach to immigration should be when the supposedly liberal 24-hour news network is pretending such measures amount to an “open border”?

‘Democrats don’t know how people think’

In one brief segment, MSNBC‘s Chris Matthews (Morning Joe, 11/6/24) was able to mangle the most important issues of 42% of the electorate.

“It’s all about immigration and the economy,” Matthews told Geist. Well, he got the economics just as wrong:

I think you can talk all you want about the rates of inflation going down. What people do is they remember what the price of something was, whether it’s gas or anything, or cream cheese, or anything else, and they’ll say, “I remember when it was $2, and now it’s $7.” But they remember it in the last five years. That’s how people think. Democrats don’t know how people think anymore. They think about their country and they think about the cost of things.

The suggestion here is that success in fighting inflation would not be bringing the rate of price increases down, but returning prices to what they were before the inflationary period. That’s called deflation, a phenomenon generally viewed as disastrous that policy makers make strenuous efforts to prevent.

A decade ago, the Wall Street Journal (10/16/14) described “the specter of deflation” as “a worry that top policy makers thought they had beaten back”:

A general fall in consumer prices emerged as a big concern after the 2008 financial crisis because it summoned memories of deep and lingering downturns like the Great Depression and two decades of lost growth in Japan. The world’s central banks in recent years have used a variety of easy-money policies to fight its debilitating effects.

in a deflationary economy, wages as well as prices often have to fall—and…in general economies don’t manage to have falling wages unless they also have mass unemployment, so that workers are desperate enough to accept those wage declines.

It’s natural for ordinary consumers to think that if prices going up is bad, prices going down must be good. For someone like Matthews to think that, when he’s been covering national politics for more than three decades, is incompetence.

“Practical men who believe themselves to be quite exempt from any intellectual influence, are usually the slaves of some defunct economist.” John Maynard Keynes made this observation in 1936, in his masterwork The General Theory. Nearly a century later, readers and viewers of corporate media face the same fate.

The fundamental problem confronted by these news consumers is not that corporate news outlets consult economists in their reporting; as experts in their field, economists often have important and worthwhile contributions to make. The problem is that these outlets consistently elevate the views of specific economists who serve particular ideological interests over the views of other economists, or even the academic profession as a whole.

The austerity gospel

Simon Wren-Lewis (LRB, 2/19/15): “‘Mediamacro’…prefers simple stories to more complex analysis. As part of this, it is fond of analogies between governments and individuals, even when those analogies are generally seen to be false by macroeconomists.”

Consider the case of the 2008 financial crisis and the austerity mania that followed. The British economist Simon Wren-Lewis (London Review of Books, 2/9/15) has documented how media depictions of austerity diverged sharply from professional economists’ understandings and textbooks’ explanations of macroeconomics. His term for the media’s unique understanding of macroeconomics is “mediamacro,” which is characterized by an obsession with cutting the deficit over and above all other concerns.

In the wake of the banking crisis that followed the collapse of the housing bubble in 2007-08, and then the onset of the Eurozone crisis in 2010, standard textbook macroeconomics dictated a runup in the deficit to stimulate the economy out of a downturn. Corporate media, however, bought the arguments of political conservatives and a fringe of academic economists (who nonetheless held positions at prestigious universities), who maintained that austerity, specifically through spending cuts, could return the economy to health.

In the most notorious instance, corporate media outlets opportunistically promoted the findings of a 2010 paper, written by two Harvard economists, that were later famously invalidated due to an Excel error. As Paul Krugman noted in 2013 (New York Times, 4/19/13), this paper was controversial among economists from the start, but this did not stop corporate media from citing it—and its flimsy assertion that there existed a tipping-point for government debt at 90% of GDP, beyond which this debt supposedly imposed a major drag on economic growth—as gospel:

For example, a Washington Posteditorial earlier this year warned against any relaxation on the deficit front, because we are “dangerously near the 90% mark that economists regard as a threat to sustainable economic growth.” Notice the phrasing: “economists,” not “some economists,” let alone “some economists, vigorously disputed by other economists with equally good credentials,” which was the reality.

The view from finance

As Mark Copelovitch (SSRN, 10/27/17) has noted, “The single most important factor [in elevating falsehoods about austerity] has been the media’s willingness to embrace and promote these narratives, while largely ignoring the overwhelming empirical and historical evidence that austerity is deeply contractionary and counter-productive.”

In another instance recounted by Wren-Lewis (LRB, 2/9/15), after the return of some growth in 2013 in Britain following the election of a Conservative government committed to austerity in 2010, the Financial Times editorial board (9/10/13) declared the Conservatives victorious in their political argument for austerity. This despite the fact that “less than 20% of academic economists surveyed by the Financial Times thought that the recovery of 2013 vindicated austerity.”

Such false right-wing narratives about macroeconomic policy came to dominate media discourse, not merely because political elites adopted these false narratives and thus made them newsworthy, but because corporate media outlets were compliant messengers for elite views and prescriptions.

Why does the media adopt “mediamacro” as its approach to coverage of the economy? One reason proposed by Wren-Lewis (LRB, 2/9/15) is the influence of City of London (or, in the US case, Wall Street) economists, whose

views tend to reflect the economic arguments of those on the right: Regulation is bad, top rates of tax should be low, the state is too large, and budget deficits are a serious and immediate concern.

Moreover, the political leanings of corporate media outlets, whether or not they are made explicit, may encourage them to seek the expertise of economists of a particular ideological bent. These economists’ views may, in turn, be out of step with the academic mainstream on topics like austerity.

The inflation oracle

The corporate media’s tendency to elevate economists of a specific type hasn’t disappeared in the 2020s. With the onset of Covid and the spike in inflation that followed, media broke out their familiar playbook of consulting prominent economists with extreme, and business-friendly, positions.

The infamous example was the elevation of Larry Summers, who slammed Biden’s 2021 stimulus as “the least responsible macroeconomic policy we’ve had in the last 40 years” and warned stridently of inflation (Washington Post, 5/24/21). When inflation rose to a high of just over 9% the next year, Summers was hailed by the media as “an oracle: the man who saw it all coming,” as Jacobin editor Seth Ackerman (2/13/23) sarcastically put it.

In one sense, it was true that Summers had seen inflation as a strong possibility, and he did deserve some credit for that. Other economists, notably Paul Krugman, had downplayed the possibility of a jump in inflation and had to eat their words (New York Times, 7/21/22). But the fact that Summers had gotten this one point right, after an illustrious career of getting things wrong, did not exactly justify his skyrocketing status as the go-to voice on inflation, or the heaps of at times fawning media coverage thrown his way (Wall Street Journal, 6/27/22; Fortune, 9/23/22).

Did it justify, for example, Summers garnering six times as many mentions as Krugman on top cable news channels from 2021 through 2023? A Nobel laureate and widely respected commentator, Krugman also happened to be the most prominent proponent of a more dovish, less austere approach to inflation. Though he failed to foresee the initial rise in inflation, Krugman accurately predicted, in contrast to Summers, that the US economy could achieve a “soft landing,” a fall in inflation without a substantial rise in the unemployment rate (New York Times, 5/18/23).

Meanwhile, Summers capitalized on his new status as economic prophet to insist that extreme pain was required to tame inflation. By mid-2022, he confidently proclaimed (Bloomberg, 6/20/22):

We need five years of unemployment above 5% to contain inflation—in other words, we need two years of 7.5% unemployment or five years of 6% unemployment or one year of 10% unemployment.

Cherry-picking expertise

Like the views of extreme austerity advocates in the wake of the 2008 financial crisis, Summers’ views in 2022 were acutely out of sync with the mainstream among academic economists, as becomes apparent from surveys of professional economists taken over the course of the inflationary outbreak.

Financial Times/Booth survey of macroeconomists (9/13/22)

One FT/Booth survey taken in the fall of 2022 is particularly informative. It found that most economists thought that the Federal Reserve was on track to contain inflation with its pace of interest rate hikes. Specifically, when asked to react to the statement “Futures markets now suggest the Fed will raise the federal funds rate to about 3.9% by the end of 2022,” only 36% of economists classified the Fed’s actions as “too little too late and insufficient to help keep inflation under control.” The rest either thought that this policy path was sufficient to contain inflation (55%) or thought that it was overkill (9%).

When asked about the toll Fed policy would take on the labor market, academic economists took a moderate stance. Most agreed that the unemployment rate would peak below 6% and that a recession would last for less than a year. Incidentally, only a small minority of economists seem to have foreseen the possibility of inflation returning to target without a recession and with unemployment rising no higher than 4.3%, which is what in fact has occurred. But notwithstanding their apparent excess of pessimism, economists generally agreed that inflation would come under control with nowhere near the punishment Summers was prescribing.

To be fair, these economists were not asked directly what would be sufficient to contain inflation, and if asked directly, it is likely that some segment would have been in Summers’ camp—after all, about a third of the economists surveyed thought that the Fed was doing “too little too late.” But those backing Summers’ full diagnosis would be a fraction of those taking this minority view. So the central point that Summers was in the minority, and likely in quite a small minority, among professional economists is undoubtedly true.

Yet with his quasi-divine status granted by corporate media, Summers could pontificate freely about the need for mass suffering without fear of marginalization for lack of evidence or credibility. So when he prescribed 5% unemployment for five years, all that an outlet like Bloomberg (6/20/22) did was report on his views, no skepticism necessary. And no warning label stating: This is completely out of step with the academic mainstream. In effect, corporate media decided to once again cherry-pick expertise to legitimize austerity policies.

‘Not sensible policy’

James K. Galbraith and Isabella Weber (Boston Globe, 8/22/24) : “Americans still have some common sense…. It shows that all of the efforts of free-market economists to beat it out of them have not yetworked.“

At the same time, alternatives to the dominant austerity paradigm have been treated with caution, if not outright hostility. The New York Times (8/15/24), for example, in a recent piece on Kamala Harris’s advocacy for anti-price-gouging legislation, did consult Isabella Weber, a progressive economist who has become well known for her work on profit-driven inflation. But her testimony was overshadowed in the piece by that of economists with more conservative takes on the issue.

Most notably, the Times relied heavily on the insights of Harvard economist Jason Furman, who helped lead the push for extreme austerity alongside Summers (Wall Street Journal, 9/7/22). His first quote in the article had a simple Econ 101 message: “Egg prices went up last year—it’s because there weren’t as many eggs, and it caused more egg production.” In other words, egg prices went up because of supply issues, and it’s good that prices went up because that spurred more egg production.

Unfortunately, this story doesn’t fit with the facts. Responding to this Furman quote, Weber and James Galbraith observed in a separate article (Boston Globe, 8/22/24):

In fact, US egg production peaked in 2019 and then fell slightly, through last year. Egg prices spiked from early 2022 to $4.82 a dozen on average in January 2023, before falling back again, with no gain in production. High prices did not stimulate America’s hens to greater effort. On these points, Furman laid an egg.

It might be assumed that the Times would engage in this sort of basic factchecking of its sources, and not leave it to two progressive economists writing in the Boston Globe to do that for them. But when the source is a Harvard economist who not too long ago was suggesting (wildly incorrectly) that unemployment would have to jump over 6% for two years to tame inflation (Wall Street Journal, 9/7/22), apparently skepticism is not in order.

Leaving little room to doubt the leanings of the Times reporters, the article ended with another quote from Furman, this time on Harris’s proposal to go after price gouging:

“This is not sensible policy, and I think the biggest hope is that it ends up being a lot of rhetoric and no reality,” he said. “There’s no upside here, and there is some downside.”

Hand-picked by elites

Conor Smyth (FAIR.org, 2/14/24): “For media outlets owned by the wealthy, there’s obvious utility in directing the conversation away from inequality and toward other concerns.”

If one of the main functions of the media is agenda-setting—deeming certain topics, like government debt, newsworthy and others, like inequality, not so much (FAIR.org, 2/14/24)—another primary function is legitimization: letting audiences know who they should trust and who they should treat with skepticism. Over the course of the recent bout of inflation, corporate outlets have made it clear that those economists who erred on the side of far-reaching austerity were worth listening to. The ones who dissented most strongly from the austerity paradigm were, for the most part, sidelined or only tepidly consulted.

The result has been a constrained debate. Extreme pro-austerity positions have enjoyed high visibility, while progressives have been relegated to the background. This is not because of an imbalance in the evidence. If anything, the side that has been arguing for anti-austerity measures to fight inflation, like temporary price controls, has more evidence for their claims than the side that’s backed harsh monetary austerity. They, at least, haven’t been proven embarrassingly wrong by the experience of the past couple years.

What could help explain the imbalance in coverage is instead the background of different sets of economists. Before being legitimized by corporate media, extremists for austerity like Summers and Furman were legitimized by political status—Summers served in top roles under Bill Clinton and Barack Obama, and Furman served as a key adviser to Obama. Progressives like Isabella Weber have not enjoyed similar political standing.

Thus, we can see a sort of chain of legitimization that runs from a political system dominated by economic elites to a media ecosystem owned by economic elites. If you can secure a top post in politics, it doesn’t matter whether you’re an extremist with views contradicting the consensus among academic economists. Your views should be taken seriously. For progressives, who have largely been excluded from elite politics in recent decades, serious skepticism is in order.

On the face of it, this system makes some sense. But think a little deeper and you can see an insidious chain servicing the dominant players in American society. That chain needs to be broken. Media outlets need to listen to the evidence, not the false wisdom of economists hand-picked by American elites.

The University of California Board of Regents approved a request from five UC campuses, including UC Berkeley and UC San Francisco, for additional military equipment for their police departments.

Janine Jackson interviewed journalist Freddy Brewster about the supermarket megamerger for the August 30, 2024, episode of CounterSpin. This is a lightly edited transcript.

Janine Jackson: In October of 2022, the largest supermarket chain in the US, Kroger, announced a plan to take over the second-largest supermarket chain in the country, Albertsons, in a merger that would create the country’s third-largest private-sector employer overall—after Walmart and Amazon—a conglomerate of some 5,000 stores and 710,000 employees. What could go wrong?

A lot of things, the Federal Trade Commission suggested, as they sued to block the merger this February, including less competition, lower quality products and weaker bargaining positions for workers. Legal proceedings began this week.

Our guest is helping make sense of this story. Writer and journalist Freddy Brewster’s latest piece on the proposed Kroger and Albertsons merger, and the maneuvering behind it, appears at LeverNews.com. He joins us now by phone from the Bay Area. Welcome to CounterSpin, Freddy Brewster.

Freddy Brewster: Hi, thanks for having me on. Appreciate it.

JJ: If we could first situate this in common sense and lived experience: Americans have been seeing the price of eggs and milk and other staples go way up, to the point where already-struggling people are pressed to the limit. Asking why this is happening, we’ve been told for years now, well, Covid, and related supply chain problems, and inflation. It’s out of companies’ control.

I have problems already with that, because the notion that companies have to maintain a certain profit margin, no matter what’s happening in the world, is a choice. Companies could always accept less profit, or pay managers less, if keeping prices down was their aim.

But, OK, Covid, supply chain, inflation: That’s no longer the reality, yet it’s still somehow the story. Did Kroger not just acknowledge in testimony that, oh yes, we did push prices higher than inflation just because we could, but still if you give us more market power, you should believe we won’t do that anymore? I want to ask you about specifics, but this whole baseline, to begin with, almost seems like a joke at the expense of people already struggling. Am I missing something there?

Freddy Brewster: “Kroger’s CEO, on a shareholder call, admitted that inflation is a good thing, because it’ll allow the company to raise prices.”

FB: No, no, you’re kind of right on it. And just add to that, in 2021, Kroger’s CEO, on a shareholder call, admitted that inflation is a good thing, because it’ll allow the company to raise prices, pass the cost on to consumers and keep prices high. In fact, I have a quote right here from Kroger CEO Rodney McMullen, from that shareholder call, and it says, “We view a little bit of inflation as always good in our business, and we would expect to be able to pass those costs through to consumers on things that are permanent in nature.” And so, right here, he is admitting that they can use inflation to raise prices, and then keep those prices high.

JJ: And that sounds like exactly what they’re saying they won’t be doing in this sort of PR talk about lower prices and better choices.

I went to look up this story, and I found a website called KrogerAlbertsons.com, which opens with this, I find, hilarious disclaimer, and I just want to read it:

Certain information included in this website is forward-looking, and involves risks and uncertainties that could cause actual results to differ materially from those expressed or implied by such forward-looking statements. These statements are based on the assumptions and beliefs of Kroger and Albertsons companies management in light of information currently available to them.

And it goes on:

Such statements are indicated by words or phrases such as “accelerate,” “create,” “committed,” “confident,” “continue,” “deliver,” “driving,” “expect,” “future,” “guidance,” “positioned,” “strategy,” “target,” “synergies,” “trends” and “will.”

Now companies call this skating where the puck’s going to be, right? You just act as though you’ve already gotten the thing that you’re demanding. And then if the deal doesn’t happen, you’re encouraging people to see it as nature’s path being interfered with, rather than public-protecting processes being followed.

FB: Yeah, that website is funny, and it’s almost like, if there’s any young people out there who are aspiring to work in PR, you can read that website. It is just like those words that they highlight themselves are rather interesting, and kind of like buzzwords, to be able to push a certain type of narrative that they find benefits them, or would be profitable to their narrative.

JJ: What information is the FTC working with when they set up to question or potentially block this merger? Why are they doing that?

FB: They want to block this merger because, like you had mentioned earlier on, this merger could result in poor-quality products, higher prices and worse employment options for employees, especially for employees who are trying to unionize or who want to threaten to be able to go work at the competitor.

Just to give you kind of a sense of Kroger’s market power, in an attempt to allay the concerns from the FTC about this merger, Kroger had promised to sell off 600 stores, slash prices by a billion dollars, and invest a billion dollars in wages if the merger is allowed to go through.

So what this kind of says and highlights is that Kroger is already buying Albertsons for $24.6 billion, and is willing to invest another $2 billion to bring down prices and to get more wages. That shows that they already have quite a bit of market power. They have $29 billion sitting around that they can use to buy another company and lower prices and give people better wages. Well, why aren’t they lowering prices and giving people better wages right now?

That statement itself just highlights the market power that Kroger has, and if this merger is allowed to go through, they’ll have even greater market power. And Kroger says that they want this merger to go through to be able to compete with Walmart and Amazon, which may be legitimate, but Walmart and Amazon, they operate in different spheres than what traditional grocery stores do.

JJ: Right. So the idea that all four of these companies… we as citizens are meant to be excited about a bigger behemoth getting into the fight with other behemoths.

FB: Yeah, exactly. And Kroger already owns a handful of common grocery stores that people know about. There’s Fred Meyer, there’s Harris Teeter, they own King Soopers and Ralphs. And then also Albertsons owns Safeway. They own…

JJ: Acme, I think….

FB: Shaw’s and Vons. Yeah, exactly. And so all of this would put it all under one roof.

And then also, if this merger’s allowed to go through, what puts it under that same roof, too, are also all those store-brand products. Like Kroger has Kroger brand salad dressing, for example, or different sauces or snacks or whatever. And Albertsons has the same thing. But then that puts it all under one roof, one house in one store, and that leaves less options for consumers.

And an expert I talked to highlighted about how when there’s less options, that these companies are focused on profits, and they often use emulsifiers and other things that really aren’t the best to be consuming for the average human, and that can affect health in different ways, weight in different ways.

JJ: Among other tactics, Kroger is declaring that the FTC’s whole case should be thrown out because it’s unconstitutional, because it involves Kroger’s “private rights.” What legal legs do they think they’re standing on there?

FB: So, historically, the courts have ruled in favor of these government agencies. The FTC, for example, and similar with the Securities and Exchange Commission, have these internal courts that rule on certain matters. So, for example, the FTC internal administrative court, they hear evidence, kind of like a standard court, and will issue initial decisions. And companies have sued in the past to try to say this is unconstitutional, and has to be fought in federal court. But the courts have largely ruled in favor of these government agencies.

Up until recently; that’s begun to change. Now the Supreme Court, earlier the summer, ruled that the in-house courts issuing civil penalties for securities fraud, for the Securities Exchange Commission, is unconstitutional. And then, also, there was a 2023 Supreme Court ruling that allowed companies facing an FTC enforcement action to challenge those actions that the companies deemed unconstitutional in federal court, before those actions are deliberated inside the internal FTC court. So it’s a little convoluted, but those are the two main cases that Kroger is relying on to say that the internal FTC court is unconstitutional.

JJ: Listeners will know that we’ve been instructed to see corporations as people since Citizens United, but if I’m in court and I’m deleting relevant text messages, I’m not sure that I could just say, “Oh, well, you know, stuff happens.” Tell us a little bit about some of the behind the scenes actions, if you will, that seem meaningful here to this case.

FB: So deleting text messages and internal chats has seemed to become the go-to tactic for business executives facing enforcement actions and regulations from the federal government. Jeff Bezos and Amazon executives were caught using Signal, which is an encrypted messaging app, but it also has the option for auto delete. And so a lot of these messages that they were exchanging between each other were automatically deleted.

Google executives were also caught deleting messages. So Google has this internal policy where it directs employees to use a feature that automatically deletes Google Chat messages after 24 hours. And Google received an order from regulators to preserve these messages, but a judge found that the executives did not properly notify employees to stop using the auto delete feature, and some messages were deleted.

And there’s also, in the case of Google, messages that have been preserved that show that some of these executives realized the fact that the auto delete function was not turned off. And so it’s preserved in court documents that show that they know that they were supposed to turn off this auto delete function, but they had left it on.