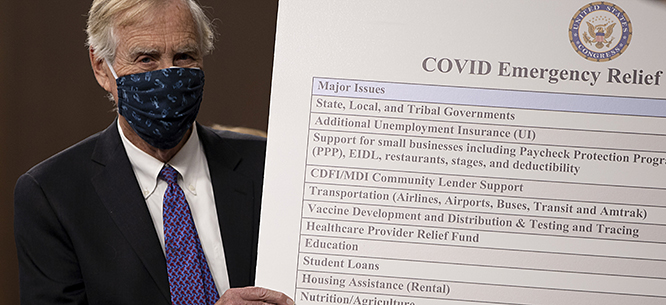

From 2020 to 2022, Americans saw the state mobilize immense resources to boost their standard of living—and then witnessed the hard political constraints hemming in this capacity.

This post was originally published on Dissent Magazine.

From 2020 to 2022, Americans saw the state mobilize immense resources to boost their standard of living—and then witnessed the hard political constraints hemming in this capacity.

This post was originally published on Dissent Magazine.

China’s economy is facing multiple headwinds, including a local government debt crisis, weak domestic demand and the collapse of property prices.

Meanwhile, unemployment among young people has hit a five-year high.

It’s taking its toll, with high numbers of young people dealing with depression amid an uncertain job market and uncertain futures.

China’s 18-24 year-olds were found to have a 24.1% risk of depression in a government mental health survey completed last year, compared with an overall risk of 10.6% for adults generally.

In a further signal of dark clouds on the horizon, this year China’s population declined for the first time in more than half a century.

“China is entering a severe demographic crisis … becoming more and more so a demographically old country,” said Dudley Poston, an emeritus professor of sociology at Texas A&M University.

The latest in China’s multiple economic woes is deflation, which economists broadly believe to be a signal of weak demand.

Data released Monday showed that the cost of the average Chinese shopping basket stayed the same in June, while the Producer Price index, a measure of inflation at the wholesale level, sharply fell, according to reports.

Nomura economist Richard Koo said in a recent episode of Bloomberg’s “Odd Lots” podcast that deflation “is a very bad sign macroeconomically.”

“Individually, [people trying to save money] might be doing the right things, but collectively, they may be killing the economy.”

Koo coined the term “balance sheet recession” – the idea that too much debt can plunge an economy into recession for many years, even decades – to describe Japan’s “lost years” after it fell from commanding economic heights in the late 1980s.

He argues that China faces “Japanification” if it does not come up with the right policies, such as offering support for key areas of weakness like the property sector.

The balance-sheet recession experienced around 30 years ago in Japan was triggered by a collapse in property prices, said Koo. “That is already happening in China. So few people are borrowing, so many people are paying down debt.”

Hesitant spenders

Late last year, the Chinese government announced an ambitious 12-year plan that would see household consumption driving the economy, in a move away from fiscal stimulus, or investment, which has long been Beijing’s tool for stimulating the economy.

China’s household spending accounts for just 38% of its GDP, well below the global average of 68%, while 43% of China’s economy is driven by investment – about double what the U.S. economy relies on.

Some economists cheered the move, which would see a massive restructuring of the Chinese economy.

Others were more skeptical.

Writing for Foreign Affairs last month, Zhongyuan Zoe Liu and Benn Steil said, “Sensible though it is, consumption-led growth in Xi’s China is doomed to fail. As Xi has done so often in the past, he will back away from the policy once the inevitable backlash from powerful constituencies, including state-owned enterprises, local governments, and the national security bureaucracy, takes hold.”

It was a prescient warning. Chinese consumers are simply not spending and Beijing is already showing signs that it is ready to use fiscal stimulus measures to jumpstart the sputtering economy.

Bloomberg this week reported that “more economic support measures are imminent” with authorities signaling it was time to offer relief to the ailing property market by extending loan relief for developers.

State media ran reports this week suggesting that supportive policies were needed in the property sector in order to boost business confidence.

Economist Michael Pettis, writing for the Carnegie Endowment for International Peace, notes that household consumption comprises less than 40% of China’s GDP as of 2020,” versus a global average in other countries of roughly 60%. “China has by far the lowest consumption share of GDP of any economy in the world,” he wrote.

Pettis argues that the reason Chinese consumption, as a share of GDP, is so low is “no mystery.”

“Chinese households retain a very low share – in the form of salaries and wages, other income, and transfers – of what they produce, so they are unable to consume more than a low share of what they produce.”

Pettis argues that Beijing’s much touted “common prosperity” policy, which will theoretically redistribute wealth from the rich to ordinary Chinese and broadly boost spending confidence, is likely to only help “at the margins.”

Back to stimulus

China’s first move back to its tried and trusted stimulus playbook is likely to focus on the property sector, and according to reports financial regulators have been stepping up pressure on banks to ease terms for property companies and extend outstanding loans.

The People’s Bank of China and National Financial Regulatory Administration said in a joint statement on Monday that the aim is to ensure the delivery of homes that are under construction.

“When a large bubble bursts and asset prices collapse badly, it’s going to take five, 10 years easily to repair those balance sheets,” said Koo.

He added that the Chinese are aware of this problem.

“Once you know that this is a recession that is produced by lack of borrowers – the borrowers are not coming to borrow money because they have balance-sheet problems themselves … then the government has to step in and borrow and put that money back into the income stream, which means fiscal stimulus is absolutely essential.”

Koo said, it’s not a problem that China can export its way out of because China already has the world’s biggest trade surplus and any moves to make it bigger will face resistance from other countries. “It will cause trade friction,” he said.

Edited by Mike Firn.

This content originally appeared on Radio Free Asia and was authored by Chris Taylor for RFA.

This post was originally published on Radio Free.

Senate Minority Leader Mitch McConnell (R-Kentucky) is facing widespread criticism for his recent assertion that the so-called labor shortage in the U.S. is the result of the stimulus checks that were sent out over a year ago.

At an event in Kentucky on Tuesday, McConnell said that the $3,400 in direct aid sent out to American taxpayers over the past two years has been holding people back from working — a misleading statement in several respects, especially considering the fact that unemployment is currently quite low, with some states documenting record low unemployment over the past few months.

“You’ve got a whole lot of people sitting on the sidelines because, frankly, they’re flush for the moment,” McConnell said, according to Insider. “What we’ve got to hope is once they run out of money, they’ll start concluding it’s better to work than not to work.”

Sen. Elizabeth Warren (D-Massachusetts) condemned McConnell’s statement on Twitter on Wednesday. “Mitch McConnell’s blaming Americans for not wanting to work. It’s absurdly out of touch,” she said. “More workers have jobs now than pre-COVID. Investing in affordable child care would help parents return to work, but Republicans refuse to support actual solutions.”

Indeed, it is absurd to suggest that the checks, which were aimed at combating COVID-related financial and employment problems, could be a lifeline for struggling families years after they were sent out.

Although the stimulus checks and expanded child tax credit did help decrease financial hardship and poverty immediately after they were sent out, the effects of the aid only lasted so long. As of last month — 14 months after the last stimulus checks were approved and six months after the last expanded child tax benefits were sent out — 39 percent of Americans said that it’s difficult to afford regular expenses like bills or rent. That’s up nearly 50 percent from last spring, according to an analysis by The Lever.

For years now, McConnell and other Republicans have been moaning that the stimulus payments suppress employment. But analyses of the financial aid programs that Congress implemented for the pandemic show that these claims are simply not true.

In fact, the extra financial aid may have helped people get back into the job market earlier than they would have, as the money helped people afford to pay for child care, as well as expensive measures that make it easier to get a job, like education, certifications, relocation, and more. Last year, economists found that employment recovery slowed down in states that prematurely ended the early COVID-era expanded unemployment insurance checks, in comparison to states that continued giving the checks out.

In reality, the reason that McConnell and the GOP have complained about the stimulus checks and other federal aid is likely because their ideology hinges upon opposing measures that reduce poverty. For decades now, they have parroted lies that reducing the welfare state will help the economy, while quietly helping out wealthy donors and corporations at every turn.

McConnell’s implication that there is a labor shortage is also misleading. Employers have been moaning about a lack of people willing to work — a myth that circulated last year and which was likely created by conservative think tanks and corporate lobbyists.

But workers have said, through surveys and labor activism, that a major factor preventing them from getting or keeping work is that employers aren’t paying nearly enough to survive in the current economy. Data has backed up these claims; when accounting for inflation, workers actually got a pay cut across the board last year.

This article was published in partnership with the Los Angeles Times.

Photos by James Bernal.

For years, Annie Graham’s dream was to open her own business. She began piecemeal, hunting down merchandise at swap meets, thrift stores and garage sales, developing an eye for items with resale potential. Eventually, 15 years ago, she was able to rent a unit on Manchester Boulevard, in a predominantly Black area of Inglewood, which adjoins Los Angeles. Now, her business spans four storefronts.

“I started out with just a little square,” she said. “Just a square. And I kept working hard, and each time someone would move out, I would just go over, go over and go over.”

Ms. Ann’s features racks of colorful dresses and rows of sneakers and stilettos. A mannequin in the window features a ruffled purple dress. Another shop, The White House, features only white outfits for weddings and parties.

Graham knows the owner of nearly every shop in this stretch of Inglewood – Hair by Mari, Swank Men’s Fashion, a shoe store called TILT, the Styling & Profiling barbershop.

“Mainly this section from Fifth across Manchester is all Black-owned businesses here,” she said. “So we’re all fighting to help each other to stay in business.” She’s adapted to the pandemic like they all did. She began selling home decor. When she fell behind on rent at the storefronts and at home, Graham let go of her team of six, all independent contractors and most of them family members. The Easter finery she had stocked last spring is still on the racks. Now, she said, her customers mostly buy dresses for funerals.

The federal Paycheck Protection Program, one of the largest financial bailouts since the Great Depression, promised to help businesses like Graham’s. In signing the Coronavirus Aid, Relief, and Economic Security Act – or CARES Act – on March 27, 2020, President Donald Trump announced that the PPP would provide “unprecedented support to small businesses” in order “to keep our small businesses strong.” The program has injected more than $770 billion into businesses, including Reveal from The Center for Investigative Reporting and the Los Angeles Times, since last April.

But a year after California shut down, Graham had yet to receive any government assistance – despite multiple attempts to apply. In fact, in Graham’s corner of Inglewood, only 32% of businesses got PPP loans.

Through the CARES Act, Congress ordered the Small Business Administration and the Treasury Department to issue guidance to lenders to ensure that the program “prioritizes small business concerns and entities in underserved and rural markets.”

Yet a Reveal analysis of more than 5 million PPP loans found widespread racial disparities in how those loans were distributed.

Those disparities were visible across the nation. Reveal found that in the vast majority of metro areas with a population of 1 million or more, the rate of lending to majority-White areas was higher than the rates for any majority-Latinx, Black or Asian areas. In many metro areas, the disparities were extreme.

Explore where Paycheck Protection Program loans were distributed across U.S. states and territories in Reveal’s interactive map.

Los Angeles had some of the worst in the nation. Although communities of color were hit far harder by COVID-19, businesses in majority-White areas received loans at twice the rate that majority-Latinx tracts received, one and a half times the rate of businesses in majority-Black areas and 1.2 times the rate in Asian areas.

The New York metro area, which includes Newark and Jersey City in New Jersey, saw equally striking disparities, with White areas receiving loans at twice the rate of Latinx areas, 1.8 times the rate for Black areas and 1.2 times the rate in Asian areas.

In other metro areas, including Dallas, San Francisco, San Diego, Las Vegas and Phoenix, businesses in majority-White areas also received loans at about twice the rate as those in majority-Latinx areas.

In the Philadelphia, Kansas City and Baltimore metro areas, businesses in majority-White areas received loans at 1.7 times the rate that businesses in majority-Black areas did. And in San Francisco, White areas got loans at 1.2 times the rate as Asian ones.

Shannon Giles, a spokesperson for the Small Business Administration, said the agency does not comment on third-party analyses of its data.

Last May, Reveal and 10 other news organizations sued the Small Business Administration for access to PPP loan data. A federal judge ordered the release of the records in November.

Reveal’s analysis is the first look at how PPP loans were distributed at the census tract level across racial groups. As the Treasury Department and SBA initially eliminated a standard demographic questionnaire from the PPP application, banks did not routinely collect information on the race or gender of borrowers. So Reveal looked at loan totals and business data according to the racial makeup of each tract.

Jesse Van Tol, CEO of the fair lending group National Community Reinvestment Coalition, said the disparities Reveal uncovered show that banks failed to live up to the goals of a 44-year-old federal law that requires them to equitably serve all communities where they do business.

The racial disparities in the PPP rollout may not be patently illegal, Van Tol said, because the law has limited mechanisms for accountability. “It requires leadership and someone from those agencies to say, ‘This was a problem.’ ”

But of the disparities, he said: “Is it fair? No. Is it equitable? No. Does it violate the spirit of the Community Reinvestment Act? Absolutely.”

The inequities of the PPP are etched along the landscape of Los Angeles. Travel along Manchester, a four-lane road stretching from South LA to the ocean, and the disparities come into sharp focus. To the west, the avenue empties out into the laid-back beach community of Playa del Rey. Businesses are struggling in this majority-White community, too, but most of them – 61% – have been bolstered by PPP assistance.

When Joey Ancrile, one of the partners at The Shack, posted on Facebook last summer that the iconic burger joint needed support, he said customers lined up around the block to order burgers. By then, The Shack was already approved for a $156,000 PPP loan and received an additional $109,000 in February. “The PPP loans have really saved us,” he said. “And, of course, the community. They showed up.”

Across the street, Cantalini’s Salerno Beach Restaurant – a local institution founded in 1962 – got a $95,000 PPP loan last April and an additional $133,000 in January. It wasn’t easy: When owner Lisa Schwab first contacted her own bank, Wells Fargo, she said, “They were just buried.” But she then submitted a successful application with WebBank, an online lender. “There’s no way we would’ve survived without that money,” Schwab said. “It was a lifeline.”

So at the neighborhood place, named after her grandparents, Schwab is still serving up the recipes her grandmother taught her – ravioli, eggplant parmesan, gnocchi.

“I had a good support team,” she said. “There are a lot of people out there that don’t and they were trying to navigate some pretty difficult waters.”

Fifteen minutes east on Manchester is a predominantly Black area of Inglewood, where business owners got PPP loans at roughly half the rate of Playa del Rey. Graham, whose dress shop is here, first tried applying for a PPP loan at her bank, Wells Fargo, just like Schwab. But she found the online process complicated and couldn’t successfully submit an application.

In May, she heard that a company owned by former basketball star Magic Johnson had invested $100 million with MBE Capital Partners to fund PPP loans for minority- and women-owned businesses. So Graham applied with the New Jersey-based fintech company.

On June 15, an MBE representative emailed Graham about some missing paperwork. She needed to submit payroll documents, IRS forms 940 and 941, it read. But Graham, as a sole proprietor, did not file them. Like 96% of Black business owners, she didn’t have employees on payroll.

On June 23, MBE declined her application. The documents she submitted, the email read, “did not support the loan request.”

She mailed a letter to MBE the next day. “I am a small, minority, woman-owned business,” she wrote. “It was my understanding that your mission was to help and assist businesses like mine.”

“For me not to be able to get any help, it’s hurtful, that’s all I can say,” she said.

In an interview with Reveal, MBE’s president, Carra Wallace, acknowledged that the lender should have reached out to Graham to help her revise her application. But she said the company was overwhelmed as it reviewed roughly 20,000 PPP requests. Reveal’s analysis shows that MBE ultimately extended loans to majority-Black neighborhoods at a far higher rate than most other lenders.

“We’re a small business that is a minority-owned business ourselves that all of a sudden got asked to participate and help out and do something good for our community,” Wallace said. “We didn’t have the resources to spend an hour on the phone with somebody. We needed you to go online, read the directions and upload the right information so that we can process it through.”

Farther east on Manchester lies a predominantly Latinx stretch of South LA, where the picture worsens. Here, 10% of businesses received PPP support – six times less than in Playa del Rey. The experience of Herminia Reyes, who took over Alfredo’s Mexican Food less than a year before the pandemic hit, is typical. She pivoted to delivery services and relied on her drive-thru window. But as an immigrant who pays taxes with an Individual Taxpayer Identification Number, or an ITIN, instead of a Social Security number, she was shut out by the PPP last year. She hasn’t received any loans or grants, she said.

“I haven’t had any help from the government because I’m an immigrant,” she said. “I felt discouraged.”

The PPP also failed to reach Daniel Sanchez, owner of Giann’s barbershop, two miles farther east. Just 10% of businesses in his Florence neighborhood got loans.

“The bills, they have to get paid,” he said. “And I did not have help from anyone.”

The first round of the PPP, totaling $349 billion, opened up just days after the CARES Act was signed – and was depleted within 14 days. Lenders had to prepare for the onslaught before the Small Business Administration had even issued guidelines. That rush widened the gap between who was approved and declined for PPP loans. Any obstacle, such as missing paperwork or a lack of an existing relationship with a bank, risked leaving a business last in line.

By the end of round two in August, for an additional $321 billion, the costs of that bungled rollout were clear. A Reveal investigation found that businesses in Republican states yet to experience the brunt of the pandemic were more likely to receive funds in the program’s first round. The Washington Post found that most money from the first two rounds had gone to large businesses, with about 600 big companies and national chains receiving $10 million, the maximum. McClatchy and the Miami Herald found that banks raked in $18 billion in fees for handing out the loans – without risking any of their own capital.

In October, a congressional select subcommittee on the coronavirus crisis issued a sharply critical report on the program’s implementation. Congress had instructed the administration to prioritize underserved communities and “economically disadvantaged individuals,” according to language in the CARES Act.

The SBA, Treasury and the country’s biggest banks failed to implement this directive, the subcommittee found. Despite what JPMorgan Chase called “almost daily guidance” from the SBA, no lenders interviewed by the subcommittee recalled receiving any guidance on prioritizing underserved communities. Several banks had fast-tracked the PPP process for wealthier customers “at more than twice the speed of smaller loans to the neediest small businesses,” according to the report. Banks’ larger clients “often benefitted from a faster, more personalized experience.”

The subcommittee also found that the American Bankers Association, citing a call with Treasury officials, told its members to direct PPP lending to existing customers. At least one major bank knew this would create a “heightened risk of disparate impact on minority and women-owned businesses,” according to an internal Citibank memo. The New York Federal Reserve Bank has found that most Black business owners don’t have an existing banking relationship.

Although Treasury later denied giving that guidance, the report found that several major banks had moved forward with the directive. The Treasury Department did not respond to requests for comment.

The SBA declined an interview. In response to a request to outline steps the agency took to prioritize underserved communities last year, spokesperson Shannon Giles wrote: “The SBA continues to support efforts to benefit the smallest businesses and underserved communities and address potential barriers to access to capital. It also has called on its lending partners to redouble their efforts to assist eligible borrowers in these communities.”

“This was a government program,” said Van Tol, of the National Community Reinvestment Coalition. “We wouldn’t have said you can only get your stimulus check if you happen to have a banking relationship with a bank that’s going to offer a stimulus check. But that’s how the PPP program played out.”

Even business owners of color with banking relationships struggled to gain access. “When they said small business, I thought, ‘Oh yeah, that’s me. I’m a small business,’ ” said Lara Curtis, owner of Mingles Tea Bar in Inglewood. She called her bank, Capital One, but the lender did not begin processing applications until April 15, the day before the first PPP round was depleted. (Curtis was later approved for $2,600 with online lender Square.)

Edward Flores owns an eatery on Olvera Street, a historic district lined with Mexican restaurants and artisan shops. He took over Juanita’s Cafe, founded by his grandmother in 1944, three decades ago.

“It’s one of the oldest remaining places in LA that’s been untouched,” Flores said.

When Los Angeles shut down, so did Olvera Street. With sales down catastrophically, Flores said he cut his operating hours and laid off his staff. When the city allowed restaurants to do takeout, Flores went to the cafe as early as 4 a.m. to cook small batches of food himself, clocking in 13-hour days. “There was one day that I recall that I sold $11.25,” he said.

He’s banked at Bank of America, the largest PPP lender in the nation, for decades. But Flores said he didn’t think the bank would help.

“They’re going to show me the door,” he said. “I don’t know who wants to loan money to a business that’s failing.”

He wasn’t the only proprietor in the historic district to miss out on the massive federal aid program – only 21% of businesses in the Olvera Street area got PPP loans last year, around a third the rate of Playa del Rey.

Seven miles east, in a majority-Asian corner of Monterey Park, the rate was only slightly higher. Here, about a third – 37% – of businesses received PPP loans. Ron Tang, owner of the bubble tea cafe One Zo, was one of them. A former tax manager, Tang said he had a good relationship with Bank of America; when his foot traffic dropped dramatically last year, he secured PPP funds with ease. But since then, the bank rejected his application twice due to a “tax ID discrepancy.”

“I called multiple times and sometimes they would say it’s with the SBA, sometimes they would say they’re reviewing my application,” he said. “I don’t really know who to blame. It’s more like … ‘Why is this happening to me at a time when we really need the funds?’ ”

Malik Muhammad runs a bookstore at a mall in Baldwin Hills Crenshaw. He turned to Wells Fargo, the bank he’d relied on since the 1990s, for help. The owner of Malik Books, which specializes in African American books and literature, submitted his online application in early April.

For weeks, he waited for a response. On June 2, he received an automated email from Wells Fargo that read: “We cannot confirm that all applications will be submitted and processed by the SBA before the funds are depleted, and we anticipate that demand will exceed available funding.” And that was it. Like most businesses in his predominantly Black neighborhood, only 32% of which got 2020 loans, the PPP initially left him out in the cold. (Muhammad later received a small round two PPP loan through Square.)

“I didn’t even get a follow-up from them whatsoever,” he said. “I know we’re not big business, but we deserve a call.”

In the Los Angeles area, Wells Fargo, the nation’s fourth-largest PPP lender, effectively starved communities of color of PPP money. The bank lent to businesses in majority-White neighborhoods at more than twice the rate it lent to businesses in majority-Black and Latinx neighborhoods.

In Miami, San Francisco, New York, Phoenix and Dallas, the bank also lent at higher rates in White census tracts than Latinx or Black ones.

The bank declined Reveal’s interview request, but spokesperson Manuel Venegas said in a statement that the lender was aware of the disparities. In response, Venegas said the bank supplied capital to community development organizations and launched an email campaign in February 2021 – almost a year after the PPP began – targeting Wells Fargo’s clients in communities of color “to bridge those awareness gaps and help facilitate these owners getting the support they need.”

JPMorgan Chase, which, according to SBA data, lent the most PPP money last year at $29 billion, produced similar disparities. In New York, Los Angeles, Houston and Chicago, it approved loans to businesses in White-majority communities at more than twice the rate as in Latinx and Black neighborhoods.

In a statement, JPMorgan Chase spokesperson Anne Pace claimed the lender had served communities of color in proportion to their numbers in Los Angeles. But she did not dispute the disparities affecting majority-Black and Latinx communities in particular and acknowledged that the bank prioritized existing customers. “Under the program rules, the most efficient way to get funds to as many struggling businesses as possible was to initially focus on our existing clients with a business deposit account,” Pace said.

Together, the top five lenders in the LA metro area – Bank of America, JPMorgan Chase, Cross River Bank, Wells Fargo and Customers Bank – made enough loans to cover nearly a quarter of businesses in majority-White census tracts. The same lenders extended loans covering about 20% of businesses in Asian tracts, 16% of businesses in Black tracts and 11% of businesses in Latinx tracts, according to Reveal’s analysis.

Some of the widest lending disparities in the metro area came from Los Angeles-based City National Bank, which extended loans in White-majority neighborhoods last year at four times the rate of majority-Black neighborhoods and nearly seven times the rate of Latinx neighborhoods. City National did not dispute Reveal’s findings, but spokesperson Debora Vrana noted that the bank had done “extensive outreach” about PPP loans to partners serving communities of color.

No lender was more dominant in implementing the PPP than Bank of America, which facilitated the most PPP loans in the country – 343,500 – for a total of $25.5 billion. It sent loans to White communities in the LA area at nearly twice the rate it did to majority-Latinx and Black communities. In such major metro areas as New York, Miami, San Francisco, Dallas and Phoenix, the bank’s lending to majority-White tracts also outstripped its lending to majority-Latinx or Black tracts.

When asked about the wide disparities Reveal found in Bank of America’s numbers, Dan Letendre, a senior vice president focused on serving low-income communities, blamed the loan program’s design.

“We did recognize that the Paycheck Protection Program design would present challenges for many of our clients, and in particular for very small businesses,” he said. “When the program was designed, the view was, ‘How does the economy or system get money to employees who can’t go to work and are therefore likely to be unemployed?’ Which I think was valuable.”

With sole proprietorships more common in communities of color, he said, “they did see less money.”

While it’s true that the program was initially unfavorable to sole proprietors, “it’s also fair to say that there were problems with the way banks were implementing the program,” said Kevin Stein, deputy director of the California Reinvestment Coalition. “The blame could be applied in both places.”

Banks, under the Community Reinvestment Act, must affirmatively meet the credit needs of communities where they operate. But banks can meet this mandate in part by farming out the work to community development financial institutions, or CDFIs, that work closely with underserved communities. Letendre said Bank of America provided more than $850 million in credit to CDFIs that went toward roughly 10,000 PPP loans.

The reliance by banks on CDFIs and so-called minority depository institutions, the congressional report found, “failed to adequately address the needs of minority and women-owned small businesses.” And most CDFIs were shut out of the first round of PPP funding entirely because Treasury required that lenders have a historical lending volume of over $50 million to participate. Facing criticism, the SBA and Treasury set aside $60 billion for community lenders, including $10 billion for CDFIs, during round two last year.

Still, as one CDFI explained to the congressional subcommittee: “CDFIs felt like an afterthought in PPP.”

On a recent afternoon, Mark McKenna sits at the desk in his bedroom and stares at the three computer monitors before him. Headphones on, he makes calls to business owners applying for PPP, or those he suspects may qualify. “Ron, how are you?” he says in an upbeat voice. “This is Mark McKenna from Prestamos.”

McKenna is a business development officer for Prestamos – “we lend” in Spanish – a CDFI founded by the Phoenix-based nonprofit Chicanos por la Causa. Over the past year, he’s spent countless hours processing PPP applications.

With most of its clients in Arizona, Nevada and California, Prestamos approved more than 900 PPP loans totaling some $26 million last year, outperforming most other lenders in Latinx communities. Like other CDFIs, Prestamos received funding from such major lenders as Bank of America and Wells Fargo.

After a year of processing applications, McKenna possesses an intricate understanding of why so many small business owners were shut out by the PPP. Many banks didn’t proactively reach out to sole proprietors, he said. And the name of the program itself – Paycheck Protection Program – confused many sole proprietors, who assumed they didn’t qualify because they didn’t issue paychecks.

In addition, the SBA’s forgiveness restrictions initially disadvantaged sole proprietors who needed to cover rent and utilities instead of payroll.

Some business owners, like Herminia Reyes, the owner of the Mexican restaurant in South LA, lacked a Social Security number and were barred from applying altogether.

Still others told Reveal that they hesitated to take out a loan in the middle of economic uncertainty – a hesitancy that may have been exacerbated by the restrictions on qualifying for forgiveness. Daniel Sanchez, the barbershop owner, said he was concerned about defaulting on a loan and ending in bankruptcy.

“I just believe you save your money, pay them (a bank) to take care of your money, and that’s that,” he said.

There are other challenges.

Many small business owners don’t consistently maintain their financial documents and don’t have the computers or scanners they need to send those documents to banks. McKenna, who is based in Tucson, Arizona, often found himself asking whether a neighbor or relative has a computer a client can borrow or simply asking clients to take photos of their ID and bank statements with their phones.

“I can’t even tell you how many people didn’t even bother applying because they didn’t have those capabilities,” he said.

It was another massive government investment in the middle class that ingrained racial wealth gaps that persist in the United States today.

Faced with a housing crisis in the 1930s, Congress established the Federal Housing Administration and tasked it with facilitating mortgage lending in an effort to create jobs and expand homeownership. But the agency refused to insure mortgages in predominantly Black neighborhoods – neighborhoods rated as “hazardous” credit risks on color-coded federal maps.

These discriminatory lending practices, known as redlining, were never completely reversed. In 1977, Congress passed the Community Reinvestment Act, which requires banks to serve all communities regardless of income. But there were major flaws in the federal law: It lacks strong enforcement mechanisms – and doesn’t explicitly mention race. In 2018, Reveal found that Black and Latinx households were still denied conventional mortgages at far higher rates than their White counterparts.

But despite the banking system’s consistent failures in serving communities of color, Congress designed the PPP to run through commercial lenders.

“So when you have a crisis like COVID, like a pandemic, when you say, ‘OK, we’re going to put together a recovery program,’ … and you run that recovery program through that same system, you’re going to see the same result, right?” said Paulina Gonzalez-Brito, executive director of the California Reinvestment Coalition. “You’re not going to see an equitable recovery.”

In September, the Federal Reserve announced a proposal to reform regulations in the Community Reinvestment Act to better serve the law’s “core purpose.” One of the considerations is how to better address “ongoing systemic inequity in credit access for minority individuals and communities.”

“What is happening is a real reckoning around race in this country,” Gonzalez-Brito said. “It’s not enough, frankly, for bank CEOs to say Black lives matter. … It’s not enough for banks to put together racial equity philanthropic initiatives. … It has to be policy changes and systems changes within their own practices if we’re actually going to make a difference in the way that they’ve been functioning for generations.”

The Biden administration made a few changes to the PPP that are already reaping benefits for very small business owners. In February, the SBA established a 14-day exclusive PPP loan application period for businesses with fewer than 20 employees. By March 5, minority business loan approvals had increased 20%, according to the SBA.

“The SBA is working to ensure the economic aid is accessible to all that are eligible, including those hit hardest, while protecting program integrity and ensuring as quick distribution as possible of the aid,” said Giles, the SBA spokesperson.

Sole proprietors can now apply by reporting their gross income instead of net, resulting in larger loan amounts. And business owners with ITIN numbers, like Reyes, the restaurant owner, can now apply. The current round of PPP lending closes out May 31.

For many businesses, these changes came too late. As the October congressional report found, “the PPP can no longer assist owners and employees of businesses that closed as a result of previous implementation failures.” A New York Federal Reserve Bank study found that Black business ownership declined sharply – 41% – in the first few months of the pandemic, two and a half times more than White businesses. Latinx and Asian business ownership also dropped at higher rates than White ownership, 32%, 26% and 17%, respectively.

Could more equal PPP lending have made a difference? If every community in Los Angeles had received PPP support at the rate that White neighborhoods did, some 79,000 more businesses in majority-Asian, Black and Latinx communities could have gotten loans, according to Reveal’s analysis.

As with redlining practices from decades past, the PPP’s disparate lending patterns risk affecting communities of color for generations, said Kevin Stein, of the California Reinvestment Coalition. “What are the main ways that people build wealth? It’s through homeownership and then it’s through small business ownership.”

For family-run businesses that closed, Stein added, “there’s a great likelihood that they will be unable to build wealth in this generation.”

Gonzalez-Brito, now based in Oakland, grew up in Los Angeles and said she worries about her hometown’s future. “When I go back, it’s going to look so different,” she said. “We’re going to lose all these small businesses that have been there. And who is going to replace them?”

On Olvera Street, Edward Flores’ cafe was approved for a $108,000 loan under a separate SBA economic disaster program. That loan is not forgivable, and a statement has already arrived in the mail.

“I’m fairly certain that we’re going to survive,” he said. “That’s probably what a lot of businesses are just trying to do – is just survive.”

On Manchester Boulevard in Inglewood, Annie Graham, the owner of Ms. Ann’s, is hanging on by a thread. She received a $15,000 California Small Business COVID-19 relief grant – but “my rent ate that up immediately,” she said – and was also approved for an economic disaster loan. She applied for the PPP again, this time through the CDFI Lendistry, which did not ask her for payroll documents. She was approved in March for nearly $15,000.

“I built my business on faith and strength, not on what somebody else can do,” she said. “So that’s why I’m trying to hold on.”

Reveal community engagement producer David Rodriguez, Los Angeles Times reporter Alejandra Reyes-Velarde and freelancer Sarah Cohen contributed to this story. It was edited by Esther Kaplan, Soo Oh, Jack Leonard and Jennifer Goren and copy edited by Nikki Frick.

Laura C. Morel can be reached at lmorel@revealnews.org, Mohamed Al Elew can be reached at malelew@revealnews.org, and Emily Harris can be reached at eharris@revealnews.org. Follow Morel and Harris on Twitter: @lauracmorel and @emilygharris.

This story was produced with the support of the John S. Knight Journalism Fellowships and Big Local News at Stanford University.

Rampant racial disparities plagued how billions of dollars in PPP loans were distributed in the U.S. is a story from Reveal. Reveal is a registered trademark of The Center for Investigative Reporting and is a 501(c)(3) tax exempt organization.

This post was originally published on Reveal.

To envision a global Green New Deal requires a serious effort to grasp the deep inequities of the international economic order.

This post was originally published on Dissent MagazineDissent Magazine.

Sen. Pat Toomey (R-Pennsylvania) blocked an attempt to protect stimulus payments from being seized by predatory debt collection agencies, after several Senate Democrats requested a vote of unanimous consent on the issue Thursday.

As part of the latest coronavirus economic relief package, every American under a certain income threshold is set to receive (or has already received) a $1,400 stimulus payment for themselves and for each dependent listed on their tax forms. But protections against collections agencies were not included in the final bill that reached President Joe Biden’s desk earlier this month, due to Senate rules regarding the reconciliation process.

Sen. Ron Wyden (D-Oregon), Sen. Sherrod Brown (D-Ohio) and other Democrats had proposed a standalone bill on Thursday that sought to provide protections against debt collectors taking stimulus funds from Americans.

“The Senate will either stand today for the working families who desperately need this help … or the Senate is with private debt collectors, reaching their hands into those families’ pockets,” Wyden said in remarks on the Senate floor.

“We passed these checks to help families, to support families, to support local economies, not to line the pockets of predatory debt collectors,” Brown added.

Democrats had requested a vote of unanimous consent, a parliamentary procedure that allows quick passage of the bill without delay. However, Senator Toomey objected to the request, delaying the bill and making it likely that many Americans will see their stimulus checks garnished.

In voicing his objection, Toomey tried to place the blame on Democrats, arguing it was their fault that the bill didn’t include protections. Toomey also defended debt collectors, stating they had “valid legal claims” to take away people’s stimulus funds.

By refusing to pass the original stimulus bill with bipartisan support, Democrats were at fault for the present situation, according to the Republican senator. “That is the only reason that this provision couldn’t be addressed because it can’t be dealt with under the reconciliation rules,” Toomey said.

It’s possible that Republicans may end up using a filibuster to ultimately block the bill, once it comes up for debate later.

This is not the first time that a coronavirus stimulus package has failed to prevent debt collectors from seizing aid to Americans. After the CARES Act was passed last spring, debt collectors began removing funds from bank accounts. The Senate attempted to shield the checks from seizure — passing a unanimous consent bill like the kind Toomey now objects to, HuffPost reported. Unfortunately, the House of Representatives did not take up the bill, and debt collectors continued to collect funds from individuals’ bank accounts.

The December stimulus bill did include protections against debt collections, as it passed without the need for reconciliation.

This post was originally published on Latest – Truthout.

Their cry-wolf act is well practiced but lacks credibility. Continue reading

The post Republicans Greet Covid Stimulus With Another Round of Inflation Fearmongering appeared first on BillMoyers.com.

This post was originally published on BillMoyers.com.

A new report has found that the American Rescue Plan, which passed the House on Wednesday and is expected to be signed into law by President Joe Biden on Friday, will sharply reduce poverty in the country, especially among Black and Latinx people.

The report, by D.C.-based think tank the Urban Institute, finds that the $1.9 trillion stimulus will reduce the projected poverty rate for 2021 from 13.7 to 8.7 percent overall. It will also shrink the racial poverty gap by reducing poverty among Black and Latinx people by 42 and 39 percent, respectively, the report says.

The economic impacts of the pandemic have hit Black and Latinx people especially hard, more so than other racial demographic groups. And, as the economy has bounced back over the past months, Black people have not bounced back as much, following the pattern of the fallout of the 2008 recession that left Black households in the lurch for over 10 years.

The American Rescue Plan, in combination with previous stimulus packages, could also cut the share of people experiencing deep poverty, or people earning under 50 percent of the poverty line, by a third, the Urban Institute report finds.

The provisions with the biggest impact on reducing poverty, say the report’s writers, are the additional unemployment checks, the extension of food stamp benefits, the $1,400 relief checks and the new expanded version of the child tax credit in the bill.

Biden’s stimulus package will also be particularly good for children, the report finds, reducing the poverty rate for children by more than half in 2021. This is in large part due to the expanded child tax credit in the bill, which expands upon the existing child tax credit by offering parents up to $3,600 per child over the next year in the form of monthly payments.

The report’s findings bolster previous reports which have also found that the expanded child tax credit could play a massive role in lowering child poverty, and poverty in general. This includes a Columbia University analysis, which found that the bill will cut child poverty by half (though the Columbia report also included several provisions like the minimum wage raise that didn’t make it into the final package).

The House passed the bill Wednesday afternoon, and the White House said that Biden will sign the bill on Friday afternoon, two days before key unemployment benefits from the last bill expire. The package passed the House and the Senate with zero Republican votes as Republicans united against the bill.

Though Republicans oppose the bill, the legislation and its policies enjoy overwhelming bipartisan support among the public. A new poll out Wednesday conducted by CNN finds that 61 percent of Americans support the bill overall. The poll also finds that 85 percent of those polled support the bill’s provisions to expand tax credits, including 95 percent of Democrats and 73 percent of Republicans — a far cry from the 0 percent buy-in from congressional Republicans.

The CNN poll of 1,009 people also finds a 55 percent majority support for the $15 minimum wage proposal that didn’t make it into the final bill.

Though the bill doesn’t include the vaunted progressive goal of raising the minimum wage, the American Rescue Plan does include provisions that have earned progressive praise. “Because of [the progressive movement’s] support, the U.S. Senate … passed the most comprehensive pro-worker piece of legislation in the modern history of our country,” said Sen. Bernie Sanders (I-Vermont).

Progressives in the House have also celebrated the package, which Rep. Pramila Jayapal (D-Washington), the head of the Progressive Caucus, called in a statement, “a truly progressive and bold package that delivers on its promise to put money directly in people’s pockets.”

This post was originally published on Latest – Truthout.

After weeks of tense negotiations on the third round of direct relief checks in the upcoming $1.9 trillion stimulus package, Democrats and President Joe Biden have caved in to demands from centrist Democrats and Republicans to lower the income eligibility for receiving stimulus checks.

While the checks will still phase out at the $75,000 yearly income threshold for individuals and $150,000 for couples, the checks will now be phased out completely for individuals making $80,000 and couples making $160,000. This is a decrease from the previous ceiling of $100,000 and $200,000, respectively.

The concession is smaller than what Republicans had been asking for in the past months and what Democrats had been considering. In their pared down version of the stimulus, Republicans called for the checks to begin phasing out at $50,000 a year for individuals instead of $75,000, but Democrats stuck to the $75,000 threshold in draft legislation released in February.

Though it was a Republican proposal to restrict eligibility, Democrats had considered it seriously despite the fact that Republicans are standing united against the stimulus anyway. But the pressure to consider lower income thresholds this time appears to have come from within the party itself with centrist Democrats like Sen. Joe Manchin (D-West Virginia) being vocal about the need to target the checks more narrowly.

Though it’s unclear exactly where the current proposal came from, the Associated Press reports that the official who was the source of the news was describing internal conversations between Democrats. Biden’s sign-off on the proposal also comes after a White House meeting with moderate Democrats on Monday, where the moderates said they would be pushing for a narrower aid package.

The official confirmed, however, that Democrats would not be conceding to Manchin’s request from Monday to cut the unemployment benefits. Additional unemployment checks are currently at $400 a week in the stimulus package, and Manchin, himself a multimillionaire, had pushed for them to be lowered to $300 a week instead.

Democrats and progressives have previously been critical of the idea of limiting check eligibility. One point of frustration is that Democrats campaigned and won the Senate on the promise of $2,000 relief checks, but that promise has been pared down twice: first with the lower amount of $1,400, and now, with the lower limit on eligibility.

Democrats like Biden have justified the smaller amount of the checks by pointing out that the amount adds up to $2,000 in tandem with the $600 checks that went out as part of the stimulus bill passed at the end of last year. However, with the more restricted eligibility for these new checks, a number of people who received the $600 checks will likely not be eligible to receive anything this time around and will therefore be denied the full $2,000 payment, some say.

Others point out that it’s going to make Democrats and Biden look bad if the people who received their stimulus checks under Trump are denied them under this new stimulus bill. “I think a lot of people who got Trump checks won’t get Biden checks,” tweeted Bloomberg reporter Steven Dennis. “Manchin & co. getting more of what they wanted.”

Another problem with the eligibility restriction is that it’s based on 2019 tax filings — before the pandemic — for those who haven’t yet filed their taxes for 2020. The pandemic has cost millions of people their jobs and slashed many others’ ability to work enough hours to make ends meet. So, it’s quite possible that someone who made $80,000 in 2019, but lost their job in 2020 or earned half as much in 2020 because of the pandemic, will not be eligible for the $1,400 check if they have not yet filed their taxes for 2020.

The stimulus checks — and the stimulus itself — have been shown in polls to have overwhelming bipartisan support from the public. Many progressives have argued that Democrats should be uniting behind popular policies, rather than cutting them. Standing for more unpopular proposals like cutting the check eligibility, some say, will harm Democrats’ chances of holding their control over Congress.

The stimulus package is set to be voted on soon. The Senate is expected to begin their second round of amendment-proposing on the stimulus, known as “vote-a-rama,” as soon as Thursday, and a formal vote may soon follow. Congress is under pressure to pass the stimulus before unemployment benefits from the last package expire March 14.

This post was originally published on Latest – Truthout.