Original post can be read here: https://www.london.gov.uk//press-releases/assembly/zack-polanski/londoners-back-policies-for-universal-basic-income

More than twice as many Londoners back a universal basic income as a way to build financial security after the pandemic than oppose it, according to new data from YouGov commissioned by Green London Assembly member, Zack Polanski.[1]

Fifty per cent of Londoners say they support a universal basic income (a policy that makes sure everyone has an income, without a means test or requirement to work) with just 22 per cent opposed.

For rent controls, which Londoners have previously supported by a large majority in other polls,[2] support reaches more than two thirds, at 67 per cent, with just 11 per cent opposed.

Zack Polanski AM will today propose that the Mayor of London supports a trial of a basic income in a budget-related motion he will propose in the London Assembly.[3]

He says:

“Introducing a national basic income needs a change of policy from Government, but we can act now to show the value of this idea in London and the benefits to people on low or precarious incomes. “The Assembly already backed the idea of trialling a basic income within London in 2020.[4] It is time for the Mayor to step up and help fund the community-led trials that are being proposed. Greens have been pushing for rent controls and a basic income for several years and, while the current Mayor has now committed to pushing for devolved powers to control rents, the Government has so far not listened. We are asking him now to work more urgently, with Mayors from other cities, to allow cities to control rents and help Londoners whose wellbeing is seriously harmed by sky-high housing costs.”

These new data suggest that a plurality of Londoners now recognise that world events may put anyone’s income at risk, and are willing to support a simplified social security system that would ensure everyone has a basic income, regardless of circumstances.

Both measures saw a plurality of support across all age groups. For a basic income, the highest level of support was seen among Londoners aged 25-49, while rent controls saw the highest support in the 50-64 age group.

Notes:

1. All figures, unless otherwise stated, are from YouGov Plc. Total sample size was 1,166 adults in London (18+). Fieldwork was undertaken between 13th – 17th January 2022. The survey was carried out online. The figures have been weighted and are representative of all London adults (aged 18+).

2. Zack Polanski AM will propose the following motion to the Assembly at the Plenary Meeting on the Mayor’s draft consolidated budget on Wed 26 January:

“This Assembly calls on the Mayor to explore the benefits of a universal basic income for Londoners, by creating a fund to support community-led trials as part of his final draft consolidated budget for 2022-23.”

Webcast of the meeting begins at 10am. Motions will be debated after a short lunch break at around 1pm.

By covering part of the cost of daycare, Child Tax Credit checks have allowed many mothers to continue pursuing a career despite the Great Resignation.

For the first time in six months, I did not receive the expanded Child Tax Credit payment on the 15th of the month. I depended on that money to afford my son’s daycare costs. Now, I’m in a state of limbo.

After a devastating pandemic, many families like mine are trying to get back on their feet, and the Child Tax Credit helped us do just that. Without those payments, I’m giving serious thought to leaving my job to take care of my child full time.

In Georgia, where I live, an overwhelming majority of parents spent the money on essentials like food, housing, and child care. I recently became a mother, and I now know just how many unexpected costs are thrown your way when you have children. The CTC has lifted millions of kids out of poverty and allowed millions of additional middle-class workers like myself to have a bit of breathing room.

When my husband and I decided to start a family, our lives were completely different. We were both working full-time jobs and running a thriving photography business on the side. Things were going well, and we felt financially secure.

By the time I’d given birth to my son in June of 2020, everything had changed. Not only was a deadly virus ravaging the country, but our financial situation had taken a turn for the worse. Our small business was hit hard when in-person photography events were first postponed, then canceled indefinitely.

When my maternity leave ended, I faced the dilemma many mothers know all too well: I needed childcare to work but I didn’t earn enough to justify the high cost of daycare. I wasn’t ready to leave the workforce, but I felt my hand was forced. Then we started receiving the monthly Child Tax Credit payments.

It was a relief to receive the money in monthly payments, instead of having to wait for our tax refund the following year. The $300 checks went straight to our childcare costs. Even though the money covered less than half of our monthly daycare bill, it was enough to allow me to keep working.

Getting the money when we needed it most was life-changing. Our “pandemic baby” was able to remain in daycare, and my husband and I were happy to see him picking up social skills that we’d worried would be delayed as a result of isolation during the outbreak.

Last month, Sen. Joe Manchin blocked the extension of the CTC into 2022. He has argued that parents would misuse the money or cease working. That couldn’t be further from the truth. In fact, a quarter of respondents to a national survey reported that the CTC made it easier for them to work, or allowed them to work more hours.

After the news that the CTC would probably end, I felt dejected. My husband and I both had student loan payments that were about to resume and without the monthly money from the CTC, there would be no way we could afford my son’s daycare bill. It’s been a saving grace that the federal government has extended the pause on student loan repayments, even though that relief will likely end soon.

My husband and I are doing all we can to make it work by picking up odd jobs here and there. We work every day hoping that it will be enough to make it by. I’m dreading the day when my son’s daycare begins to eat up too much of our budget. I’ll have no choice but to leave my job to take care of him full-time.

It’s important to me to pursue a career and to be more than just a mother. I don’t want to lose my sense of self. Now it seems inevitable that I too will join the Great Resignation that has seen so many workers leave their jobs over the past year.

Anyone raising kids now knows that a few hundred dollars a month doesn’t cover a fraction of the costs, especially with rising prices. But for many parents, these payments allowed us to participate in the workforce. There will be a lot more of us leaving our jobs if nothing is done to help working families like mine.

_____________________________________

Pasha Benjamin lives in Conyers, Georgia with her husband and their 18-month-old son. She wrote this piece in partnership with the Center for American Progress Action Fund, which advocates for progressive policies.

One of the most significant impacts of the spread of the omicron variant of the coronavirus is upon us, as a wave of Democrat-controlled school systems has begun announcing a return to indefinite remote learning.

Meanwhile, Democrats are proving incapable of responding to the pandemic in real time, and the child tax credit — the only thing keeping some families afloat — has expired. This one-two punch poses a serious financial challenge for working parents in a time of rising inflation.

With the child tax credit, Republicans have the opportunity to step in and save the day for parents in a year that could decide the legislative majority on Capitol Hill.

So far, the omicron variant has caused the most classroom interruptions in school systems across the country since August, when school reopenings were complicated by the emergence of the delta variant. Given the dramatically higher rate of transmission of the omicron variant, it’s unlikely the classroom disruptions will subside any time soon.

With the final monthly child tax credit payment sent to parents last month, many families will have limited options for managing a return to remote learning.

Since Democrats have failed to pass their partisan version of the benefit as part of a reckless spending bill, Republicans have an opportunity to take up the mantle and provide meaningful changes to the policy in a singular CTC renewal that will benefit the economic well-being of working-class families across the country.

According to a study conducted by Humanity Forward and the Social Policy Institute at Washington University in St. Louis, nearly 30 percent of parents spend some of their monthly checks on child care. The coverage for this expense is likely why one in four parents is actually working more hours thanks to the CTC, according to a recent survey.

According to the Humanity Forward study, less than 6 percent of respondents planned to work less, the majority of whom are parents with infants who will be able to seek longer-term, more gainful employment.

The benefits of the monthly, fully refundable child tax credit are abundantly clear. In six months, it has lifted 3.8 million children from poverty, enabled many parents to return to work, fostered entrepreneurship and cut food insecurity by nearly a quarter.

If the moral imperative of reducing child poverty alone is not a compelling enough reason to continue this policy, the economics surrounding it do the rest of the talking — all while empowering parents, not government.

Despite the demonstrated success of the child tax credit, working mothers are still lagging in terms of workforce participation after the initial job losses of the pandemic.

The Department of Labor estimates that 1.8 million mothers dropped out of the workforce as a result of the coronavirus. If working mothers must navigate a patchwork of inconsistent local and government obstructions amid a new COVID-19 surge without the financial support of the child tax credit, many of the gains they’ve made in the past six months will be lost.

I understand the trepidation from Republicans who are hesitant to step into an intraparty fight amongst Democrats that seemingly can only help them. But we’d be forgoing a long-term opportunity for our party for ill-gotten short-term gains. We’d be ignoring parents’ pleas today for their votes in November.

We’ve got to act now.

More players in Washington appear to be involved now in the future of the child tax credit, as Republican Sens. Mitt Romney of Utah and Susan Collins of Maine have both expressed a willingness to reach across the aisle and come to an agreement with their Democratic colleagues. More may soon follow.

This is good news, as it represents another pathway for parents to continue receiving help from one of the few successful government initiatives since the start of the pandemic.

To kill off this policy without considering the omicron variant and the immediate effects it will have on American families in the coming months would be a mistake and would undermine ongoing gains Republicans are making with the working class and suburban women.

For Republicans in Congress, this represents yet another chance to prove they are the party of solutions.

One mystery of the labor shortage is the missing paycheck: How long can people choosing not to work last without an income?

Nobody’s sure, but clues are emerging. The economy continues to recover from the COVID wipeout, and hiring remains strong. Yet Americans are beginning to report more difficulty paying routine bills, not less, and it’s probably related to the end of federal relief measures that kept millions above water during the last 20 months.

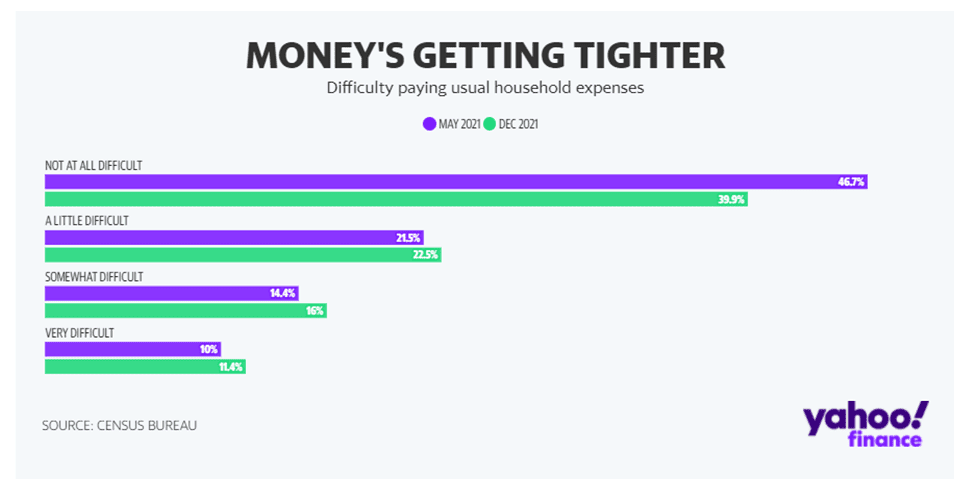

In the Census Bureau’s “household pulse” survey last May, 46.7% of respondents said they had no difficulty paying usual household expenses. By December, that had fallen to 39.9%. During the same time period, the portion saying it’s a little, somewhat or very difficult to pay those bills rose from 45.9% to 49.9%. (The remaining 10% or so did not answer the question.)

Since the economy has been steadily improving, the deterioration in household finances isn’t due to worsening unemployment or falling incomes. But the last stimulus payments went out in the first half of 2021, and emergency federal jobless benefits ended in September. With inflation at 6.8%, buying power is also eroding at the same time aid is drying up.

“There are people who are running out of money,” says Philippa Dunne of TLR Analytics. “It’s getting harder for them to pay their bills. The expiration of expanded unemployment insurance benefits and stimulus payments have taken a toll on household finances.”

There seem to be plenty of jobs for people who need to work. Employers report 10.6 million job openings, nearly the most ever. Unfilled jobs hit unprecedented levels in 2021, as COVID-related anomalies wrought havoc with the labor force. Some parents who want to work must now deal with unpredictable school schedules and an acute shortage of affordable child care. Several million potential workers may still be too concerned about catching COVID on the job to return. Federal aid money has given millions more a financial cushion that could delay a return to work or let them hold out for a better job longer than they may have been able to get before. A record-high quit rate—the portion of workers choosing to leave their jobs—suggests workers have newfound leverage, and they’re using it.

If jobs are there for the taking, people starting to feel a financial pinch should have no trouble nabbing a paycheck or finding new work that pays more or offers better flexibility. But the door to work might not be as wide open as aggregate data suggests. Job-seekers say companies seem to post some listings just to see if they can lure a dream candidate, who never materializes, leaving those jobs open indefinitely. Not all employers are boosting pay and benefits. Some parents can’t find any job offering enough flexibility to let them care for kids or sick family members.

Financial strains could get worse. Another important element of federal relief—an expanded child tax credit—expired in December and it’s not clear Congress will renew it.

The baseline child tax credit remains in place, but the expansion was worth hundreds or thousands of dollars extra to qualifying families. It also allowed those families to claim half the credit in advance, through a monthly bank-account direct deposit or check in the mailbox. The December Census survey showed 39% of child tax credit recipients—nearly 20 million households—spent the money, most likely on necessities. Thirty-eight percent said they used the money to pay down debt and just 26% said they saved it.

One surprise of the COVID pandemic was a broad improvement in household finances, when many economists expected soaring unemployment to make things much worse. Roughly $6 trillion in relief programs passed by Congress gets much of the credit. Consumers also became frenetic savers, since it was hard to spend money when businesses shut down or it felt unsafe to go out. The saving rate rocketed from 8.3% before the pandemic to a high of 33.8% in April 2020. It stayed elevated for the next 15 months, providing a financial cushion as businesses struggled to get back to normal.

That cushion is evaporating. The saving rate in November fell to 6.9%, and Census data shows that more people are now using credit cards to pay for routine expenses. A saving supercycle has now yielded to “dissaving,” when people spend down their surplus and start to borrow more.

None of this means the economy is in particular trouble in 2022, since growth remains solid and robust hiring should resume once the Omicron COVID variant begins to retreat. But tougher economic times for at least some Americans will shape political decisions in 2022 and probably impact the upcoming midterm elections.

There are murmurs in Washington about another round of aid for business and perhaps some consumers still struggling. If it happens, it won’t be nearly as big as last year’s $2 trillion package, but it would reignite disputes between liberal politicians who think Washington should do much more and conservatives who think it has already gone way too far.

Also lingering is President Biden’s “build back better” legislation, which Democrats are revamping in the hope it can pass by the end of February. One of the biggest issues is whether to reauthorize the expanded child tax credit for another year or longer, or revert permanently back to the baseline credit. That bill could also include child care assistance and other measures that might help sidelined workers get back in the action. The question for 2022 is how much help they actually need.

People are being told they will have their benefits cut if they don’t attend job agency appointments, as government resists calls to pause ‘mutual obligation’

A woman with chronic illnesses and an immunocompromised partner and the single mother of a toddler are among those being told they’ll have their benefits cut if they don’t attend face-to-face job agency appointments, despite an unprecedented surge of Covid cases.

Welfare mutual obligations, which have been suspended in Covid-affected areas for much of the pandemic, were reintroduced nationally in late October. Last week the government rebuffed calls to pause them, despite soaring infection numbers.

Guardian Australia has confirmed that while some job agencies are allowing people subject to mutual obligations to meet their requirements from home – by conducting meetings by phone or online, for example – others are insisting participants attend in person.

A participant in the disability employment services program, who did not wish to be named, said her provider warned her that she must attend a group job coaching meeting scheduled for next week.

The 23-year-old, who lives in Adelaide, said she lived with chronic illnesses but was most worried about infecting her loved ones.

“My partner has an autoimmune disorder and is on immunosuppressant medication,” she said. “I’m not really comfortable going out and potentially exposing myself and him.

“He works at the airport but he has decided to take unpaid leave because of the risk.”

Jobseekers face having their payments suspended if they fail or refuse to attend a scheduled appointment with their employment services provider.

For much of the pandemic, the government paused mutual obligations – which meant jobseekers could either continue receiving services online, or stop taking part in meetings. During the period, welfare payment suspensions for “non-compliance” were not applied.

This time, the government has rebuffed calls to return to those measures, instead setting lockdowns – which have been all but ruled out by state leaders – as the marker to dictate when mutual obligations might be stopped again.

Lauren Colvin, 38, is another welfare recipient who is being required to attend face-to-face appointments.

“I have to take my toddler [to the face-to-face meeting],” Colvin said. “We’ve been basically isolated. It’s really scary.”

Colvin, who lives near Newcastle, said she was told by Centrelink she would need to attend a face-to-face appointment on Monday with a ParentsNext provider. The program is supposed to be aimed at getting those on parenting payments on to a path towards employment.

But Colvin, who is a qualified primary school teacher, is already in the middle of a career shift, having completed a bachelor’s degree last year. She starts a master’s of psychology this year.

Colvin believes she is not eligible for ParentsNext because she is already studying, a claim backed by guidelines published online, but Centrelink has insisted she must go to the meeting.

“He just kept repeating the same line, ‘We are not currently under lockdown, therefore you must fulfil your obligations,’” Colvin said. “That was what he just kept reverting back to.

“I tried to contact the complaints line, but just haven’t been able to get through.”

Another participant in the jobactive employment program, who is based in Melbourne, asked for his next meeting to be over the phone rather than in person but was refused.

He said he was told “it’s the government’s rules and I have to do it or my payment will be cut”.

“Given this is an office with a bunch of random people going in and out all day, it’s scaring me a lot,” he said.

Cassandra Goldie, the chief executive of the Australian Council of Social Service, said mutual obligations should be suspended.

“We should not be forcing people to attend unnecessary, risky face-to-face activities, like group job-searching or appointments with jobservice providers, under threat of being cut off from their life-sustaining income support,” she said.

Kristin O’Connell, of the Antipoverty Centre, said the government should suspend mutual obligations in a “return to the strategies that kept us safe in 2020”.

“Moving activities online doesn’t go far enough – payment suspensions must be removed immediately,” O’Connell said. “We are desperately searching for Covid tests, trying to meet our basic needs in the face of shortages, and do all this on poverty payments. People need the time and space to focus on keeping themselves safe, and caring for loved ones, and recovering if they fall sick.”

A Department of Employment spokesperson said providers were required to “ensure face-to-face service delivery is safe, permitted by the relevant jurisdiction’s health orders, appropriate to the participant and staff, is reasonable in the circumstances and beneficial to the participant”.

“If a participant feels that they have a valid reason for not attending face-to-face services, such as a health or Covid-19 related issue, they should advise their provider before their appointment or activity,” the spokesperson said.

“Providers are required to find the participant an alternative and suitable service if the participant has a valid reason.

“Additionally, anyone who is sick, whether that be related to Covid or any other illness, is directed to isolate or is caring for someone who is isolating, can seek an exemption to their mutual obligation requirements.”

A spokesperson for the Department of Social Services, which runs the Disability Employment Services program, said participants were “only required to attend face-to-face appointments where it is safe to do so”.

“Participants concerned about face-to-face appointments affecting their health or that of an immediate family or household member, are offered alternative servicing arrangements,” the spokesperson said.

However the spokesperson confirmed it was DES providers that “determine whether appointments and other mutual obligations activities can take place over the phone or digitally”.

When President Joe Biden announced the Build Back Better framework in October, he called it “the most transformative investment in children and caregiving in generations” and “the largest effort to combat climate change in American history.” A month later, the House passed the Build Back Better Act, following through on Biden’s priorities by devoting $775 billion to family benefits and $560 billion to climate. But last week, Sen. Joe Manchin (D-W.Va.) said he “cannot vote to move forward,” denying the reconciliation bill the 50th Senate vote it needs to pass.

Manchin’s statement blames the bill’s size, describing it as “sweeping” and “mammoth,” and cites the Congressional Budget Office’s estimate that Build Back Better would add $3 trillion to the deficit over a decade if programs scheduled to expire were instead made permanent.

More fundamentally, though, the rejection represents a difference in values between the West Virginia senator and other congressional Democrats.

On the issues of child poverty and climate change, Democrats have a closer ally across the aisle.

Where Manchin may not vote to meaningfully address child poverty and climate change, Sen. Mitt Romney (R-Utah) would. In February, Romney released a Child Tax Credit expansion called the Family Security Act, and last week he urged Congress to use that plan as a starting point for bipartisan child benefit reform. Romney has also called for a carbon dividend onmultiple occasions, saying in October, “For the life of me I don’t understand why Democrats right now through reconciliation […] are not planning on putting in place a price on carbon.”

Romney would likely demand concessions on other parts of Build Back Better, especially the House bill’s $275 billion to expand the state and local tax (SALT) deduction and $270 billion to fund childcare. Liberal policy experts, too, have criticized these provisions: SALT expansion favors the rich, while childcare subsidies raise costs for unsubsidized parents, create welfare cliffs that discourage work, and exclude children in non-participating states. Romney’s Family Security Act instead repeals SALT and the Child and Dependent Care Tax Credit, making the plan progressive, especially paired with its child benefit, which is more generous than Build Back Better.

Renegotiating Build Back Better with Romney as the 50th vote could strengthen its anti-poverty and pro-climate impacts, but it’s not the only way to secure an expanded Child Tax Credit and carbon dividend if Manchin won’t vote for them. Nor do Democrats have to convince 10 Republican senators to join Romney and overcome the filibuster. Since the Senate can draft two reconciliation bills each year, they could use one for a Manchin Build Back Better Act and another for a Romney “Child Poverty and Carbon Emissions Reduction Act.”

With kids in poverty and a climate crisis already underway, Democrats don’t have the luxury of turning away allies. Romney could be their key to lasting change.

At least 20 guaranteed income pilots have launched in cities and counties across the U.S. since 2018, and more than 5,400 families and individuals have started receiving between $300 and $1,000 a month, according to a Bloomberg CityLab analysis. If all these programs complete their pilot periods as planned, they’ll have given out at least $35 million.

These figures mark the close of a year of rapid growth for U.S. programs that give some residents direct cash payments, with a half-dozen other pilots promised to launch in cities next year. For many advocates, the concept of “basic income” has evolved from the more expansive UBI — a universal basic income to all residents — to more targeted guaranteed income programs that have the goal of narrowing inequality and dismantling poverty.

As local programs sprouted up in cities across the U.S. in 2021, more than 60 mayors joined a coalition to advocate for the policy in their cities and nationally. Among Democrats, at least, it is no longer considered radical to propose giving low-income residents money with none of the traditional strings of welfare attached. And at the national level, Congress engaged in its own temporary mass cash distribution program, in the form of stimulus checks to the vast majority of Americans.

Still, the local programs are small in scale and duration, and the nationwide push to expand them comes as the quest for a federal guaranteed income policy has not yet succeeded. The fate of the closest thing to it — the child tax credit — hangs in the balance. Since July, the U.S. government has sent eligible parents between $250 and $300 a month for each child they have. With Congress in a stalemate on the federal spending bill, the chance of extending the benefit, which is set to expire at the end of December, looks unlikely. And there is still significant debate among those on the left over whether the massive government investment it would require to take basic income national should be a higher priority than other social programs like universal health care or affordable housing.

So if 2021 was the year of guaranteed income experiments launching and capturing the national imagination, 2022 will be the year we’ll see if these local, targeted experiments can translate into long-term shifts.

“Five years ago, we were talking about robots; we were talking about the future of work; we were talking about jobs in theory just disappearing altogether because machines were going to take over,” said Chris Hughes, an original co-founder of Facebook (now Meta) and the co-founder of the Economic Security Project, during a December panel discussion hosted by the nonprofit. Now, he said, “we’re talking about a new social contract; we’re talking about basic questions of deservedness, of racial and economic justice, of what we owe one another.”

Research findings grow

As the first phases of many of these pilots come to a close in 2022, advocates will have a growing body of research from which to draw policy.

But these initiatives aren’t the first test cases of how basic income works. So research is expanding in scope, beyond the question of whether regular cash assistance helps — proponents are already convinced that it does.

“I think personally that the body of knowledge that we have is already sufficient to push for change in the safety net,” said Stephen Nunez, the lead researcher on guaranteed income at the Jain Family Institute.

“This is a market economy and if you give people money, they’re going to be better off almost by definition by having money. The better question is better off compared to what.”

Evidence from other countries and from U.S.-led cash assistance programs has found that the monthly support sometimes reduces work hours slightly, Nunez said, and increases positive health outcomes. Early research on the 2021 U.S.child tax credit shows that families overwhelmingly spent their extra cash on food and utilities; the Census Bureau also found that the first payment alone corresponded with a drop in food insecurity in households with kids. In Stockton, California, where a basic income trial ended at the beginning of this year, the research group also reported mood improvements, less income volatility, and more full-time employment than before the money — and compared to the control group.

But critics worry that the limited duration and scope of these programs mean they’re not test cases for expansion. Among the most persistent concerns is that a guaranteed income will deter people from working at all — an outcome undercut by a Finland experiment but hard to definitively disprove.

Many of the newer pilots are designed to test optimal designs for these programs — things like the best disbursement methods, the most effective ways to combine them with other social safety net programs, and how to communicate their worth to the public, said Nunez.

Some are designed as randomized controlled trials, where researchers track outcomes for both control and recipient groups.Others are experimenting with different payment methods and periods: Compton compensates families between $300 and $600, on a sliding scale based on their size; Newark, New Jersey, which is starting its second phase this month, is paying half its participants $250 on a bi-weekly basis, and the other half twice a year, in two $3,000 installments.

Time ranges vary, with San Francisco’s $1,000-a-month for 130 artists lasting 6 months, while Hudson, New York, is paying a random selection of 25 low-income residents $500 a month for 5 years.

And unlike a universal program, which would include everyone, regardless of class, many of these guaranteed income pilots are laser-focused on specific communities that have experienced historic disinvestment, or have been most impacted by Covid, such as Black mothers and fathers, artists and low-income families. Other programs still in their design phase will target unhoused youth and foster youth.

Still,advocates emphasize that they don’t view guaranteed income as a replacement for other components of the safety net, but a supplement. “We’re not UBI maximalists,” Nunez said. For the uninsured, for example, he believes insurance would go a lot further. “Cash is not a solution to market failures.”

Shifting poverty narratives

The other goal of these guaranteed-income pilots is to shift narratives about how to address poverty in the U.S., which advocates say has failed to recover from Reagan-era notions about “welfare queens.” The Nixon administration piloted and almost passed a national basic income policy for all but the wealthiest Americans that was supported by even conservative economists.

“If you go back and you read the research on that, and try to understand why it didn’t happen, it really does feel like it came down to this human instinct of fear, or lack of trust, or doubt, in how an individual might behave if you just give them cash,” said Jill Shah, president of the Shah Family Foundation, which funded a guaranteed income program in Chelsea, Massachusetts, that gave 2,040 households up to $400 per month during the worst of the pandemic. “Like, how could it be so simple?”

It’s not enough for progressive circles just to talk about the toll of economic inequality and the promise of guaranteed income, said Aisha Nyandoro, the CEO of Springboard To Opportunities, a nonprofit organization that runs the Magnolia Mother’s Trust, a program out of Jackson, Mississippi, that is now giving its third cohort of Black mothers $1,000 a month. “It cannot be work that is typically only held by organizations that are led by brown and Black individuals,” she said at the Economic Security Project panel.

Nyandaro remembers being asked what she wanted the headline to be if the Magnolia Mother’s Trust was successful. “I want the headline to be ‘we were wrong,’” she said. “Meaning that individuals recognize that the narrative that they tell themselves about Black women is wrong.”

The fate of monthly child tax credit payments, which are set to expire at the end of this month, is murkier than ever after Senator Joe Manchin on Sunday said he wouldn’t vote for the Build Back Better Act, which would extend regular cash injections.

The senator from West Virginia has cited the bill’s cost and its potential to exacerbate inflation. He has also said he wants there to be a work requirement to receive the benefit and to limit payments to those making less than $200,000 annually. “I want social reforms to the point that [there is] responsibility and accountability,” he said in an interview with MetroNews on Monday.

Overwhelmingly, people who have received the child tax credit payments have used it for food, rent, and utilities and to pay off debt, data from the U.S. Census Bureau has found.

The credit functions as an advance for the tax refund two-parent households making less than $150,000 per year receive. Parents and caregivers get up to $300 per month for every child in their household under six and $250 per month for each older child. Families received the last of the six installments on December 15. The White House is exploring doubling payments in February, if legislation to extend the benefit passes.

So far, the majority of households making less than $50,000 per year are putting the payments toward debt, an August survey by the U.S. Census Bureau found. Higher income families were more likely to be saving the money.

Another report from the Center on Budget and Policy Priorities found 91% of households making less than $35,000 per year used the money to pay for food, shelter, clothing and other necessities. Black and Hispanic families were more likely to use their credits on education-related costs, such as school supplies.

The Biden administration has touted the initiative as a way to reduce child poverty. A study from Columbia University found that making the payments permanent could reduce child poverty in the U.S. by 40%. After the first credits went out in July, food insecurity in households with kids dropped from 11% to 8.4%, the Census bureau found.

One in four parents with young children also use the creditsto pay for child care, an October survey by the Census Bureau found. The Build Back Better Act sets aside $390 billion for subsidized child-care costs and universal, free pre-school.

In the face of the COVID-19 pandemic, and with economic and ecological crises only intensifying, it is easy to understand why so many people feel hopeless for the future. All the more so after this year’s UN Climate Conference (COP26) failed to provide the radical roadmap we need to avert climate catastrophe and as governments are trying to take us back to a dystopic, unequal “normal” despite early promises of a post-COVID re-set.

There are, however, hopeful signs of change, visible beyond the negative wall of impossibility erected by the corporate-captured media. One of these comes from South Korea, where the Democratic Party’s candidate for the presidency, Lee Jae-myung, is running on a platform arguably unmatched in its radicalism anywhere in the industrialised world.

Let me be clear at the outset that Lee is a controversial figure who is the subject of considerable critique from the left and the right, not least because of some allegedly questionable personal and political decision-making. This article, therefore, does not intend to uncritically lionise him as any kind of saviour. But the platform he is running on for the March 2022 presidential elections has such potential that it merits wider discussion.

Lee, who served as governor of Gyeonggi Province until October, is promising three major reforms: unconditional basic income (UBI), a land tax, and a carbon tax. Alone, each of these would be radical; together, they form the basis of a programme that could be transformative.

UBI is an idea almost as old as capitalism itself, and it aims primarily to attenuate the injustices of that economic system. It involves providing all people a regular cash stipend without a means test or work requirement. This would replace the complex, costly and often inefficient “benefits system” with a universal transfer set at an amount sufficient for survival.

Although simple, the implications of such a reform could be seismic.

Scholars argue that by removing the threat of destitution at the heart of the “free” market (either you accept whatever job is on offer or you starve), a UBI scheme could reduce deprivation and exploitation, liberate creative energy, allow women to leave abusive relationships, encourage men to trade work for child care, and enable all of us to re-train or pursue further learning. Perhaps just as significantly, UBI portends a shift in societal values away from “the more you are paid the more you matter” towards “we all matter so we are all paid”.

The idea of a land tax is similarly progressive. First floated by the Victorian reformer, Henry George, a land tax aims to reduce the economic rent that accrues to scarce or monopoly-controlled resources like land with a view to redistributing wealth and fostering productivity. George recognised that when the resources that we all need to survive are privatised by a select few, they can extract exorbitant rates from those able to pay while excluding those who cannot.

This leads to ever-greater concentrations of wealth alongside rapidly rising inequality, which – economists like Thomas Piketty argue – we need wealth taxes to address. It is no coincidence that Lee’s manifesto refers to the land tax as “a corrective”.

Also corrective is his manifesto’s third radical pillar – the carbon tax. Carbon taxes are widely advocated across the political spectrum as a way to wean our economies off of carbon dependence and move towards the clean, green technologies that will be vital if we are to avoid the worst of climate chaos.

The principle is similar to that underpinning the taxing of tobacco and cigarettes: we know that both are damaging, so elected governments impose tariffs to make their use less and less attractive and to fund public spending with the proceeds. In Lee’s case, the dividends would be used to fund a transitional UBI before other revenue streams come online, making the link between the economic and ecological crises and how to deal with them thrillingly explicit.

Indeed, beyond the potential that each of these individual reforms has, it is precisely the fact that they are woven together in a coherent attempt to tackle climate and capitalist crisis that is so exciting. Lee’s manifesto boldly states that its goal is to foster the “transition to a sustainable economy…[to] transform a carbon civilisation into an ecological civilisation…[and to] transform the rent-seeking economy into an innovation-seeking economy”.

These are worthy goals in any context and echo calls for a Green New Deal on both sides of the Atlantic.

What makes them radical in the full sense of that term (which derives from the Latin word meaning “root”) is that they collectively aim to address the underlying causes of the interlinked issues we face, and not just their symptoms.

Lee’s project is far from perfect. A major issue, for example, is the arguably paradoxical attempt to marry radical transformation with sustained growth – surely, a chimera when we live on a finite planet and an idea subject to sustained critique from de-growth advocates and steady state economists alike. However, his proposals match in their ambition the seriousness of the task before us and they far outstrip what is on offer in other advanced economies.

Should Lee go on to win next year’s election, then South Korea could come to represent the model for other progressive leaders to emulate. For such a victory will show that hopeful, transformative visions still have a place in our politics.

OTTAWA – This morning, NDP MP Leah Gazan (Winnipeg Centre) introduced a private member’s bill to develop a national framework for a permanent Guaranteed Livable Basic Income (GLBI) in Canada. Gazan says, as the pandemic continues, it’s never been clearer that people in Canada need financial support and a stronger social safety net.

“Since the pandemic began more people are living in poverty, while the wealthiest have become even richer. It’s shameful that the government is standing by and letting this happen,” said Gazan. “This bill is a response to calls for a guaranteed livable basic income from Indigenous, territorial, provincial and municipal jurisdictions who clearly recognize the need to modernize our social safety net. A GLBI is not only good for our economy but also critical to ensure that all individuals are able to live with dignity and security – rights afforded in the Canadian Charter.”

Gazan is proposing a GLBI for all people living in Canada over the age of 17 regardless of participation in the workforce or an educational training program. Regional differences in the cost of living are considerations addressed in the bill and there are provisions to ensure a GLBI would not mean clawbacks to services or benefits meant to meet an individual’s exceptional needs related to health or disability.

NDP critic for finance, Daniel Blaikie, joined Gazan to speak to media about the important initiative.

“While many factors contribute to the problem of poverty, there is no way to solve the problem without ensuring people have a liveable income,” said Blaikie. “The pandemic has shown how fragile our collective and personal economic well-being truly is… but it also showed that, when we work together, we have the power to provide financial security and dignity to our fellow Canadians. Leah’s bill would make income security a fundamental part of Canada’s economic framework grounded in respect for the rights and dignity of human beings. I am proud to second her bill and call on Canadians from coast-to-coast-to-coast to support this initiative for social and economic justice.”

Besides helping everyday families cover the cost of rent, food and other expenses, Gazan says a GLBI would help to protect people who are made most vulnerable by systems in our society.

“This isn’t just good financial policy; there is a direct correlation between increased rates of violence and poverty,” said Gazan. “The National Inquiry into Missing and Murdered Indigenous Women and Girls calls for a guaranteed livable basic income as a critical, life-saving measure for Indigenous women, girls and Two-Spirit individuals. If the government is serious about reconciliation, they need to get this done.”

Advocacy groups like Basic Income Manitoba, Coalition Canada and Basic Income Canada Youth Network have also expressed support for Gazan’s bill.

A panel recommends South Africa gradually implements a basic income grant, beginning with the institutionalisation of a monthly welfare payment introduced last year to offset damage wrought by the coronavirus pandemic.

“There is no alternative to a system of income support for income-compromised adults from the ages of 18 to 59 as a permanent part of the social protection framework,” Alex van den Heever, chair of social security systems administration and management studies at the University of Witwatersrand and a member of the panel, said on Monday.

The panel was appointed by the department of social development, the International Labour Organisation and the UN-backed Joint Sustainable Development Goals Fund.

The monthly welfare payment of R350, which was reintroduced after civil unrest in July, is set to end in March.

While about 18-million South Africans, or a third of the population, receive welfare payments, most come in the form of old age pensions and child support payments.

Finance minister Enoch Godongwana last month resisted calls by civil society groups for increased welfare spending and the introduction of a basic income grant, a policy business organisations say is unaffordable. The National Treasury has said it will only set aside additional funds for social relief if state finances improve by February next year.

While about 18-million South Africans — a third of the population — receive welfare payments, most come in the form of old-age pensions and child support payments.

SA is one of the world’s most unequal nations, according to the Thomas Piketty-backed World Inequality Lab.

It appears that the Government is moving ahead with a plan to provide Barbadians with a universal basic income, which may come in the form of a “citizen’s dividend”.

Avinash Persaud, Special Envoy to the Prime Minister of Barbados on Investment and Financial Services, in a recent posting on Facebook, indicated that this was on the cards.

He suggested the “citizen’s dividend may be combined with the annual reverse tax credit to form some kind of universal basic income”.

A Universal Basic Income (UBI) is defined as a government programme in which every adult citizen receives a set amount of money regularly. The goals of a basic income system are to alleviate poverty and replace other need-based social programs that potentially require greater bureaucratic involvement.

“We are moving towards universal basic income across three fronts,” he said while commenting on the absence of a government representative on a panel discussion being hosted on the subject.

Persaud wrote: “Despite all the pressure from international agencies to ‘target’ we hold the line on universality. That’s why we restored free tertiary education for all. International studies have shown this is critical to social mobility and opportunity. The less well-off cannot take on the payments, risk and worry of getting heavily in debt to secure their future.

“It’s also why we created the new Business Interruption Benefit for self-employed National Insurance Scheme (NIS) members, giving them some basic income support for the first time even without them having a standard employment contract. The Government is reviewing all NIS benefits to make sure they are relevant to modern work and that all continue to view the NIS as their social security system and not just those in traditional employment.”

Persaud also spoke to the Government’s Sovereign Wealth Fund, which he said will own all of the Government’s assets and the administration will “make them work for all Barbadians”.

He said the assets “not needed for government operations” will not be sold but used to generate income or swapped for assets that can.

“The idea is that some of the income produced every year would be given back to all citizens over the age of 18, perhaps in the form of a citizen’s dividend.

Over time the citizen’s dividend and reverse tax credit could form the basis of a universal basic income and create a greater sense of belonging to all of our people. We welcome other practical, effective ideas on how to achieve this goal quicker.”

The Government advisor added that one of the critical issues of the universal basic income was the mechanism of financing.

“Barbados’ highly innovative reverse tax credit, introduced by the Owen Arthur Administration – the envy of many developed countries – was the first [foray] into a universal basic income. That was long the objective. Under the reverse tax credit, if your income is not above some basic level, the Government will top it up with a payment or reverse tax credit.

“This is one of the practical ways a developing country could quickly get to the universal basic income. Therefore, it was regrettable that in 2016-2017, the last Government stopped paying it – they said they had no money. But everything is a tradeoff.

Like free tertiary education, they should have prioritised this kind of instrument. Since 2018 it has been paid and extended,” he stated on the social media platform.

Speaking at The Wall Street Journal’s CEO Council Summit on Tuesday, West Virginia Senator Joe Manchin issued a dire warning about the threat of inflation. “The unknown we’re facing today is much greater than the need that people believe in this aspirational bill that we’re looking at,” he said, referring to the Build Back Better Act, a multitrillion social spending bill. “And we’ve got to make sure we get this right. We just can’t continue to flood the market as we’ve done.” Manchin has expressed similar concerns before, but the timing here was not accidental: Senate Majority Leader Chuck Schumer has said he hopes to pass the bill before Christmas.

While Manchin was droning on about inflation, House Democrats and Republicans were finalizing a $768 billion defense bill, which would ultimately pass on Tuesday in bipartisan fashion: 363–70. That bill—whose ultimate figure was higherthan what the Pentagon had even asked for—would authorize a 2.7 percent raise for the military, block the Pentagon from acquiring products produced with forced labor by Ugyhurs in China, and create an independent commission to examine the war in Afghanistan (better late than never!). The bill, known as the National Defense Authorization Act, or NDAA, has not passed the Senate yet, but it is expected to sail through with far less fuss than the Build Back Better Act. Naturally, among the things that favor its chances, is the fact that Manchin has said little about how the outlay could accidentally spur inflationary fears or any such concerns about a huge sum of money getting spent. It is essentially a blank check.

Much has been made of the Build Back Better Act’s price tag—$1.7 trillion at this moment, cut down from an initial wish list more than twice as high—and its potential effect on inflation and the larger economy. For conservative Democrats like Manchin, the figure is astronomical—more than a trillion bucks!—and potentially unconscionable, given things like the rising price of gas and other commodities.

But that figure is somewhat misleading. The $1.7 trillion in spending is spread out over 10 years—meaning that the actual yearly outlay is much lower. The defense spending bill, on the other hand, applies only to 2022. If that figure was dealt with in the same fashion, it would come to north of $7.5 trillion. And yet it has hardly registered either politically or in the media. The social spending bill, however, has been a furious subject of granular debate for several months, much of it focusing on cost—with Republicans and Democrats insisting that the country simply cannot afford to pay such an immense figure for things like paid family leave and universal pre-K.

The biggest reason the defense bill has largely flown under the radar—despite being massive—is bipartisanship. Most Democrats and Republicans agree that giving raises to the military is a good thing and spending more (and, in this case, it’s worth underlining: literally spending more than the Pentagon asked for) on defense is an unalloyed good. Because there is relatively little debate over the bill—and, crucially, because the mainstream of both parties reflexively support it—the mainstream press is covering it, unsurprisingly, as a fait accompli. This bill will ultimately pass without much in the way of argument or debate or intraparty disarray, and therefore there’s nothing to cover.

For a media that is primed only to cover politics as a conflict between a red team and a blue team, this bill is basically a nonentity.

And given the press’s squeamishness in covering the military more broadly—emblematic most recently in the disastrous coverage of the withdrawal from Afghanistan, itself a product of the mass media’s cozy relationship with camera-ready celebrities from the military and intelligence fields—little effort goes into even suggesting that there might be anything remotely controversial about military spending. All of this is happening, it’s worth adding, in a presidential administration that has wound down both the war in Afghanistan and the drone war.

The coverage of the Build Back Better Act has been an entirely different beast, and it can be hard to parse the logic why. Its provisions are not just popular with the public but exceptionally popular and, in most cases, on a bipartisan basis: By and large, Americans want universal pre-K, cheaper prescription drugs, and paid family leave. But the bill has ended up being defined not by its merits, or by the public’s needs, but rather by headline-ready conflicts between politicians.

On one front, Republicans insist that the bill is too large and will lead to inflation, while conservative Democrats like Joe Manchin have raised a host of vague objections.

This is catnip for the political press: the usual partisan conflict with the added thrill of one party in disarray. These objections have thus been pushed into stories over and over again in print and on cable news, cementing them in the minds of voters. On a second front, there is a gaping empty space that the media’s coverage has left unfilled, due to a lack of effort in explaining what programs will or could end up being funded or expanded by the actual bill, and an unwillingness to offer a comparison to other types of government spending—such as military spending, which is always deemed to be “must pass.”

The comparison is instructive. Both parties have no problem swiftly moving through a gargantuan military spending bill. Meanwhile, one containing a host of social spending programs and increases is endlessly debated not on its merits but on its cost: Can we really afford to spend $400 billion over 10 years on universal pre-K? Can we do so now at a time when gas costs more than $3 a gallon?

In doing so, the media is facilitating a context collapse that keeps ordinary people in the dark, creating an odd situation in which massive military spending is treated as not just a perennial inevitability but something that is simply never up for any serious debate, when it is, in fact, a choice. Meanwhile, popular social programs that would help limit generational poverty are being treated as not just a choice but an extravagance. Right now, these programs are something that serious people will argue cannot be considered in a time of rising costs. Of course, if we weren’t experiencing an inflationary blip, a different set of arguments would simply get dusted off and pressed into service. As always, “But how will you pay for it?” remains the dominant question—at least for some things we’re paying for! People like Joe Manchin, meanwhile, will never ask the military to tighten its belt. They will demand that Democrats consider jettisoning a popular agenda.

As Congress continues to debate the Democrats’ Build Back Better legislation, a new analysis finds that almost 10 million children could potentially fall back into poverty without the extension of the enhanced child tax credit (CTC).

An estimated 27 million children will receive less than what they are currently getting, or will receive nothing at all, if the current credit is not extended past this year, according to the Center on Budget and Policy Priorities (CBPP). More starkly: An estimated 9.9 million children will fall back behind the poverty line without the monthly enhanced payments.

Among other changes, the CTC was increased this year from $2,000 per child to as much as $3,600 per child, as well as extended for the first time to families who do not typically file a tax return because their income is too low. Half of the full amount is also being sent out in monthly installments rather than as a lump sum at tax time, with the final 2021 payment scheduled to be disbursed Dec. 15. Additionally, 17 year-olds qualify for the payment for the first time.

These changes have helped millions of households, particularly low-income households, pay for basic necessities like groceries and clothing, reports and Census data have shown. If the changes are extended beyond this year, as President Joe Biden and other Democrats are pushing for, then the number of children experiencing poverty is expected to fall by more than 40%.

But “if the expansions end in 2021, this historic progress would be reversed, driving child poverty up substantially,” the CBPP reports.

Without it, the payments will shrink — the maximum credit would fall by $1,000 per school-aged child and $1,600 per child under 6 — and the lowest-income families would be ineligible once again. It would also revert to a lump sum payment included in the household’s tax return, as opposed to the monthly payments families have come to expect.

Some lawmakers worry that, at a price of $100 billion a year, it is too costly to continue in its enhanced form. Sen. Joe Manchin (D-W.V.) has said he wants to impose a work requirement on the credit and limit the program to families earning $60,000 or less. Democrats need all 50 senators on board to pass their agenda.

But many economists support the extension of the advanced credit, arguing that “can dramatically improve the lives of millions of children growing up in the United States and promote our country’s long-term economic prosperity” by reducing child poverty.

Workers’ share of corporate revenues has fallen for two decades to the benefit of owners and investors.

The labor shortage is closing that gap, and companies will have to shift cash from profits to pay, the bank said.

That means the end of corporate excess and a return to profit margins seen in the 1990s.

Morgan Stanley says it’s time for corporations to roll back their profit margins to where they were about thirty years ago — all in the name of worker power.

The investment firm’s research division released a report this week highlighting the gap between corporate profits and worker wages. The discrepancy has taken on new relevance in the pandemic-era economy amid the extraordinary labor shortage. Businesses have struggled to rehire, and workers continued to quit at record rates in September. The trends have fueled a new focus on decades of meager wage growth — and fresh scrutiny of companies’ blockbuster profit gains.

To make up for underpaying workers, Morgan Stanley says corporations should dial back their own profits for the next five years to retroactively fill the gap. After all, the other option to make up for the higher wages being demanded by workers is to raise prices. Those profits, researchers write, should resemble their 1990s level.

“Real wages currently still have to grow by 7.3% in excess of productivity growth to make up the gap,” the report reads. “If this catch-up takes place over the next 5 years, unit profits will fall 33% from current levels… This would move the corporate profit share back to its 1990s average on a pre-tax basis, and leave it just marginally above on a post-tax basis.”

The team, led by chief US economist Ellen Zentner, argues that reducing the gap between profits and worker pay can serve as a “buffer” against higher wages driving prices higher. In turn, trading profits for higher wages would help minimize inflation while reaching the Federal Reserve’s “maximum employment” goal, the team said.

The labor shortage is the US’s new normal

The chasm between compensation and productivity is a relatively new one, Morgan Stanley added. There was a “tight” relationship between the two in nearly every industry from 1950 to 2000. As businesses’ revenues rose, worker pay generally climbed in lockstep.

That link snapped in the 2000s, according to the bank. Workers’ wages started to lag profit growth. Institutions that boosted worker power like unions and high minimum wages weakened. Corporations’ owners and shareholders, meanwhile, benefitted from booming earnings and soaring stock values, Morgan Stanley said.

The gap between company profits and worker compensation in the past two decades is unprecedented and threatens the structure of the economy, the bank said.

“This divergence between real compensation and real productivity had never before been seen in the recorded data,” they said, adding the drop in worker pay “marks a break in the fundamental structure of the economy.”

Closing the gap wouldn’t be a seamless transition, the bank added. Raising wages in today’s tight labor market could put downward pressure on stocks in the near future. Still, strong corporate earnings and “ample liquidity” would cushion against a major selloff, the team said.

Reverting to the profit-wage structure of the 1990s is less radical than it may seem, the economists added. Wage growth rebounded during the pandemic as businesses scrambled to attract workers. The unusually tight labor market is already reversing the trend of the last two decades and policy is “[tipping] the scales in favor of labor,” the team said.

It turns out, the labor shortage already kickstarted that economic time travel.

Nine days later, however, Reynolds signed legislation that pays vaccine refusers to do just that: sit on the sidelines. Under the new law, anyone “discharged from employment for refusing to receive a vaccination against COVID-19 … shall not be disqualified for benefits.” Reynolds is one of many Republican politicians who openly advocate, and in some states have successfully imposed, a two-tiered system of unemployment insurance. It’s not a left-wing policy of money for everyone or a right-wing policy of money for no one.

It’s a policy of pernicious hypocrisy: welfare for vaccine refusers, tough love for everyone else.

Under these new laws, any worker who gets fired for broadly defined “misconduct,” such as flunking an employer-imposed drug test, is disqualified from unemployment benefits—but employees who refuse COVID vaccination are glorified, protected, and subsidized. The state must guarantee, in Reynolds’ words, that these reckless freeloaders “will still receive unemployment benefits despite being fired for standing up for their beliefs.”

The GOP’s coddling of vaccine refusers makes a joke of its rhetoric about self-reliance. This summer, for instance, Tennessee Gov. Bill Lee ended the federal government’s supplemental COVID-era unemployment benefits. “We are paying people to stay home. That needs to change,” he declared. But two weeks ago, Lee signed legislation that pays vaccine refusers to stay home. Under Tennessee’s new policy, the state’s normal rule about employees fired for “misconduct”—that they lose their eligibility for unemployment benefits—can no longer be applied to anyone who is terminated for “refusing to receive a vaccination for COVID-19.”

In fact, the Florida law says that if you’re unemployed and you’re offered a job that requires vaccination, you can turn it down and stay on the dole.

Last week, Kansas adopted the same policy: You can keep drawing unemployment checks while declining job opportunities, as long as you specifically refuse “work that requires compliance with a COVID-19 vaccine requirement.” And if you were recently fired for refusing vaccination—or if you were previously denied unemployment benefits because you refused job offers that entailed vaccination—the state now promises that you’ll be “retroactively paid benefits” going back to the beginning of September. This bonus payout is yours, as a special kind of welfare recipient, even if you have “not requested retroactive payment of such benefits.” Tennessee has enacted a similar clause promising “retroactive payment of unemployment benefits,” without a specified time limit.

Prior to the enactment of these laws, the standard policy about job termination for “misconduct” in most states—i.e., that such offenders were disqualified from unemployment compensation—was generally understood to cover vaccine refusal. Kansas law, for instance, defined misconduct as “a violation of a duty or obligation reasonably owed the employer as a condition of employment including, but not limited to, a violation of a company rule, including a safety rule.” Under Florida law, misconduct included “disregard of the reasonable standards of behavior which the employer expects of his or her employee.” Tennessee’s law was almost identical. Refusing vaccination, in the midst of a respiratory pandemic that has killed millions of people, was a pretty obvious safety violation. Now it’s been elevated to a sacred right.

The new state laws also make a mockery of religion. Under Florida’s statute, if an employee simply “presents” a statement “indicating that the employee declines COVID-19 vaccination because of a sincerely held religious belief,” “the employer must allow the employee to opt out of the employer’s COVID-19 vaccination mandate.” Iowa’s policy is similar. The Kansas law orders employers to accept such requests for religious exemptions “without inquiring into the sincerity of the request.” By framing vaccine refusal as religious freedom—while making it impossible to ascertain whether the refusal is truly grounded in religion—the GOP is wrapping its constituency of anti-social moochers in a cloak of martyrdom.

Republicans also argue that vaccine refusers deserve special treatment because it’s wrong, as a matter of personal autonomy, to let employers dictate workers’ health decisions. As DeSantis put it two weeks ago, “We are respecting people’s individual freedom.” But that’s not how DeSantis treats marijuana. Under Florida law, if you flunk an employer-imposed drug test, that’s “misconduct,” and it bars you from unemployment benefits if you’re fired. And if you apply for a new job—but you’re rejected for failing a drug test “required as a condition of employment” in that job—you’re further disqualified from unemployment benefits “for refusing to accept an offer of suitable work.”

Let’s pause to appreciate the Orwellian majesty of this sequence. 1) You, a responsible citizen, have gotten your COVID shots and want to be productive, so you apply for a job. 2) The prospective employer demands that you take a drug test. You test positive for marijuana, so the employer rejects you. 3) Based on the employer’s rejection of you—not your rejection of the employer—Florida declares that you have refused the job offer and are therefore disqualified from unemployment benefits. However, 4) your neighbor, who was fired for refusing COVID vaccination and has turned down two subsequent job offers that required COVID vaccination, continues to collect unemployment checks.

Meanwhile, under the same Florida law, employees who leave their jobs because they’re afraid of getting COVID become ineligible for unemployment benefits, unless they can prove to the DeSantis administration that this fear constituted “good cause” to quit. They’re treated more harshly than people who quit because they’re afraid of a federally approved vaccine.

This is how Republicans define “personal responsibility.”

Iowa has the same rule about employer drug tests. Its law specifically names marijuana as a substance that merits disqualification of the user from unemployment benefits. Under the Kansas statute, a “positive breath alcohol test or a positive chemical test” is “conclusive evidence of gross misconduct,” with extra penalties—beyond ordinary misconduct—for anyone seeking unemployment assistance. And in Tennessee, losing your job for “refusal to take a drug test or an alcohol test” can be “deemed to be a discharge for misconduct connected with work,” rendering you ineligible for assistance. When Republicans claim that their defense of vaccine refusers is based on a principled commitment to the physical autonomy of employees—as they did at a Senate press conference on Tuesday—don’t believe a word of it.

This isn’t a party of personal autonomy, moral responsibility, free enterprise, limited government, or self-reliance. It’s a party that has casually tossed aside each of these values, first for Donald Trump and then for COVID. Today’s GOP believes that the government should control workplace policies and should subsidize freeloaders who endanger their communities. It’s the party of socialism for anti-vaxxers.

FORT LAUDERDALE, Fla. (AP) — The Democratic Florida congressional candidate who lost a special election primary by five votes has filed two lawsuits asking that the result be thrown out, alleging his opponent’s support of a universal income plan amounted to bribing voters.

Dale Holness alleges Sheila Cherfilus-McCormick’s support of a proposal that would pay most U.S. adults $1,000 a month was an attempt to illegally bribe voters. His lawsuit also wants counted 18 overseas mail-in ballots received from military members and others that were rejected by elections officials because they arrived after Election Day and, officials said, didn’t qualify for an extension. He also says Cherfilus-McCormick should be disqualified because she did not file a financial disclosure form with the U.S. House.

Sheila Cherfilus-McCormick waits for the results of a machine recount at the Voting Equipment Center in Lauderhill, Fla., Nov. 5, 2021.

Cherfilus-McCormick, a health-care company executive, won the Nov. 2 primary to replace longtime U.S. Rep. Alcee Hastings, who died of cancer in April. Florida’s 20th District is overwhelmingly Democratic and she is heavily favored to win the January general election to fill the last year of Hastings’ term. The state certified her victory two weeks ago, saying she received 11,662 votes to Holness’ 11,657.

“None of the three allegations are even close to having merit. They are not in a gray area,” her campaign’s attorney, Mitch Ceasar, said Tuesday. He said the issues were already raised with the canvassing boards that oversaw the election and were dismissed.

In the lawsuits, filed jointly on Thanksgiving Eve in Palm Beach and Broward County circuit courts, Holness pointed to several campaign fliers and billboards where Cherfilus-McCormick touted her support for the “People’s Prosperity Plan.” It calls for the federal government to pay $1,000 monthly to every adult who makes less than $75,000 annually. While some progressive Democrats in Congress have supported such plans, there is no chance one would pass in the foreseeable future.

Holness, a Broward County commissioner, called Cherfilus-McCormick’s support “a gimmick designed only to motivate people to vote for her.”

“The ‘plan’ is intended to offer false hope to underserved communities with the intention and purpose of procuring votes,” Holness’ attorneys wrote. They said some district voters told elections officials they had cast ballots for Cherfilus-McCormick and wanted information on how to claim their $1,000.

Ceasar said Cherfilus-McCormick’s proposal is an “aspirational hope” that is protected by her First Amendment free speech rights.

Holness also claims Broward County erred when it rejected some mail-in ballots as being late. Under Florida law, mail-in ballots must be received by 7 p.m. Election Day with one exception: ballots sent by military personnel and other Floridians living outside the country have 10 additional days to arrive, if postmarked by Election Day. Broward County officials said they rejected the ballots, which arrive in special envelopes, because they appeared to have been mailed from within the United States or had no postmark indicating where they were mailed from.

Holness argues the lack of proof that the ballots were sent from a foreign country should not disqualify them, but Ceasar said some of the ballots were postmarked within the district.

Holness also said Cherfilus-McCormick’s failure to file a financial disclosure form with the House disqualified her from running. She loaned about $2 million to her campaign and Holness argues voters have a right to know how she earned that money. While the forms are required, many non-incumbent candidates fail to file them and that does not result in their disqualification as the House cannot punish someone before they are a member. Ceasar said she has filed for an extension.

Guaranteed income programs are popping up everywhere in the US. It is time to expand beyond local pilot programs and embrace a nationwide Citizen Dividend, an annual distribution of a share of business profits to every American, to beat back against rising economic inequality and hold true to our deepest American values.

Three years ago, perhaps the only widely known American guaranteed income program was the Alaska Permanent Fund which doles out annual payments to every Alaskan funded from state oil and gas revenue. In recent years, pilot programs giving $500 – $1,000 a month to low-income residents have been implemented or proposed in Stockton, California; Jackson, Mississippi; Phoenix; Pittsburgh; and Chicago.

Perhaps the simplest, widest-reaching, and easiest to implement form of guaranteed income we could adopt would be the Citizen Dividend. The debate around guaranteed income often boils down to two fundamental questions: Who deserves the income and how can we pay for them? With a national Citizen Dividend, we answer both of those questions clearly and compellingly.

First, who deserves this income? We all do. No business in this country turns a profit without using wealth we all own together – our natural resources; our societal resources like our roads, our public safety, and our education system; and our inherited systems like our Constitution and our courts. Every citizen has an equal ownership stake in these forms of collective wealth. Therefore, each American deserves some slice of the profits realized by their use. Sure, individual hard work, talent, and good strategy help bring about business success. Imagine though trying to create value without energy, roads, courts, and an educated workforce. It would be downright impossible.

Second, how do pay for this income? A Citizen Dividend is funded through one form of our collective prosperity – business profits. Businesses should retain 95% of their profits to invest in growth, return wealth to private shareholders, and pay the government for the services our society needs (e.g. taxes). But 5% of those profits should be returned to each American in recognition of the collective wealth that was used to create those profits.

Easy to understand and clear in its funding, a Citizen Dividend would have a meaningful positive impact on the lives of Americans and on the fabric of our economy.

Using 2015 estimates on business net income, a Citizen Dividend could return $570 to each American every year – or over $2,200 for a family of four. This payment – which amounts to nearly two months of rent or food for the median American family – could stave off some of the harshest impacts of rising inequality. But perhaps more importantly, it would challenge the false narrative that profit is created merely through individual action and that wealth should be hoarded by those who have the opportunity to do so. Instead, it would reinforce a deeper American story, that we are our best as a nation when we come together across all our differences to blaze a trail toward a common future.

A Citizen Dividend breathes life into the spirit of our nation’s first motto – E Pluribus Unum– out of many, one.

It is time we recognize what truly belongs to every American and be bold in our willingness to build an economy that reflects our best values. It is time for a Citizen Dividend.

Almost twice as many voters support the idea of a universal basic income compared to those who oppose the idea, a new poll for LFF has found.

The poll, carried out by Savanta:ComRes, found that 44% of respondents support the idea of a universal basic income compared to 23% who oppose it.

A universal basic income (UBI) is a regular cash payment every individual receives, without any reference to their other income or wealth and without any conditions. A UBI would help alleviate poverty, provide a degree of economic security and give people real freedom over their lives. It would also remove the uncertainty and stress that so many who receive means-tested benefits face, fearing a sudden withdrawal of support that will push them into poverty, as we saw with the government’s decision to scrap the £20 uplift in universal credit which it is estimated will push 200,000 children into poverty.

While critics argue that ‘free money’ will mean a greater number of people dropping out of work, studies of UBI trials have found the exact opposite.

While 33% of 18-24 year olds support the idea of a universal basic income, the number rises to 46% of those aged 65 and over.

When it comes to party affiliation, 41% of Conservative Party voters support the idea of a universal basic income as do 55% of Labour Party voters, 54% of Liberal Democrat voters and 57% of Green Party voters.