We are public opinion scholars at the Harvard T.H. Chan School of Public Health. We conducted a survey to try to understand how the first round of aid had affected American families in need. What we found shocked us.

We are public opinion scholars at the Harvard T.H. Chan School of Public Health. In cooperation with our partners at the Robert Wood Johnson Foundation and National Public Radio, we conducted a survey in July and August of last year to try to understand how the first round of aid had affected American families in need. What we found shocked us then and feels relevant now as the government negotiates its next steps.

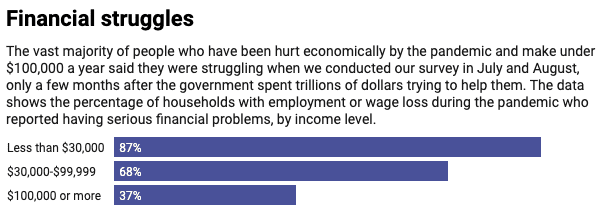

Despite trillions of dollars in government assistance, about two-thirds of families that suffered job losses or reduced wages during the pandemic still reported facing serious financial hardship.

Many people were struggling – and still are – just to pay for basic necessities, like food and rent.

The first round of pandemic aid

Congress passed most of the initial relief in March, including direct payments to qualifying families, expanded unemployment benefits and loans to small businesses that turned into grants if they kept workers on their payroll.

By July 1, when we began our survey, most Americans entitled to a direct check should have received it, and unemployed adults were still receiving supplemental aid of $600 a week on top of state benefits.

We wanted to understand the financial burdens experienced by American families that were economically harmed by the coronavirus pandemic. And we wanted to see whether the government aid was helping the people who needed it most.

Using a nationally representative, randomized survey design, we contacted 3,454 adults and asked them about the financial problems facing their households.

We focused on the 46% who said they or other adults in their household either lost a job, had to close a business, were furloughed or had their wages or hours reduced since the start of the coronavirus pandemic. We published our findings in the economic affairs journal Challenge in January.

Serious financial problems

While it seems like a no-brainer that Americans weren’t ready for the unexpected employment disruptions caused by the COVID-19 pandemic, it was surprising to us that federal aid and charitable assistance seemed to be doing so little to support the people it was intended to help.

We found that the aid didn’t put much of a dent in the financial problems faced by families earning less than $100,000, whether because relief was delayed or wasn’t spent, the amount wasn’t adequate or the funds never made it to the intended recipients.

Among households with employment or wage losses during the pandemic, 87% of those earning less than $30,000 a year and 68% of those earning $30,000 to $99,999 told us they were still facing serious financial problems. And more than half of households in these income brackets reported they had already used up all or most of their savings – or they didn’t have savings to begin with. That share jumped to over three-quarters for people with incomes under $30,000.

Savings take years or decades to accumulate, so it’s likely these households are in even worse trouble now. What’s more, significantly less aid has been provided from the federal government since we conducted our survey.

Julie Dzerowicz, Member of Parliament for Davenport, has introduced legislation in the House of Commons that would enable a national strategy for a guaranteed basic income in Canada.

This is the first time a bill has been introduced in the House of Commons on guaranteed basic income.

If passed, this bill would enable the federal government to establish pilot projects in one or more provinces to test models of implementation of a guaranteed basic income program; create a framework of national standards to guide the implementation of a guaranteed basic income program in any province, and collect data on the impact on government (including responsiveness, cost and reducing the complexity of and/or replacing existing social programs), on recipients, and on recipient communities (including entrepreneurship, job creation and civic action).

Canada’s current social welfare system was created in the 1970s. No matter how many times it is adjusted still too many people fall through the cracks, says a media release.

“Canada needs a robust social welfare system that meets the needs of the 21st century worker, that is more flexible and adaptive while being less complex and better at tackling inequality,” says Dzerowicz.

“It is also important to provide Canadians stability with full and equal access to opportunities so they can be more innovative. I believe that guaranteed basic income could be the key tool that helps deliver on all that and this bill enables us to test it,” she adds.

The world of work is under constant change with many shifting to the gig economy of temporary and short-term contracts and others are being impacted by the effect of automation and AI. It is important for our social welfare system to better reflect the needs of Canadians for today and tomorrow and to be much more flexible at managing labour changes, disruptions and transitions. Bill C-273 proposes that guaranteed basic income is tested as a model that may deliver more flexibility for the new world of workers.

Sheila Regehr, Chair, Basic Income Canada Network, says “This bill takes the building blocks of better income security for all Canadians—the experience, evidence, expertise and know-how we possess—and puts the gears in motion to make it happen.”

BICN is a non-partisan organization that has been working with all parties. This bill, calling for a national strategy, is in line with recommendations in BICN’s brief to the 2021 Pre-Budget Consultations.

Floyd Marinescu, Executive Director, UBI Works, says “Basic Income could create 300,000-600,000 jobs and add $80B/yr to Canada’s GDP while ensuring we have abolished working poverty.

“In this period of rapid disruption of work and declining social mobility, basic income defends equality of opportunity and unlocks our ability to take risks: a key factor for improving Canada’s innovation and labour market productivity.”

As Canada moves its way through this pandemic, it is planning for post- COVID with the intention to spend $70-$100 billion over three years to jumpstart the Canadian economy, it’s the perfect time to fix structural issues, to test innovative ideas, and to build our economic and social foundations back better.

Canada has been criticized for lagging on innovation and productivity. Strong policies, mechanisms and programs are needed to fully focus on improving our innovative potential including ensuring Canadians have the stability they need in order to innovate and take risks, which guaranteed basic income can provide.

Basic income experts, academics and thought leaders have made it clear that there is already strong existing information that supports the effectiveness of guaranteed basic income but less so on the best ways or models to implement and deliver it.

Bill C-273 is focused on enabling the capacity to frame, test and validate different models of implementation to get to those answers and that data.

This legislation comes as provinces like Newfoundland and Labrador and Prince Edward Island consider their own basic income pilots.

“A Guaranteed Basic Income has been bandied about for years and this Bill could provide for the implementation of pilot projects that would allow the collection of data; therefore, decisions could be made on real facts rather than assumptions. I would welcome such a pilot for PEI,” says Wayne Easter, Member of Parliament, Malpeque, Prince Edward Island.

One universal truth holds both pre-pandemic and now: The number one obstacle to escaping an abuser is financial insecurity.

This article contains descriptions and discussion of violence and abuse.

Opinion by Stacey Rutland, founder of Income Movement

When I was 7 years old, my mom woke my sister and me in the middle of the night and told us to pack our belongings into the black garbage bags she handed to us. “And be as quiet as you can,” she told us. We were leaving our abusive stepfather for the first of what would become many times. That night, we drove 200 miles to a close family friend who had offered us her living room couch as a safe space to regroup.

Four years later, the same stepfather left us. After beating our mom, he abandoned us in a home with rent we couldn’t afford without him. It was winter, and our heating bills skyrocketed. Free lunch at school was the primary nourishment for my sister and I during those cold months.

Over the past months, I have imagined what these two crisis moments for our family would have looked like if there had been a quarantine-in-home order and a pandemic raging across the globe.

But millions of women and children don’t have to imagine it; they are living it right now, with dire consequences.

The increased stress that comes from more time spent at home during the pandemic has led to massive spikes in domestic violence, a crime in which women are victims 85% of the time. Early pandemic data shows that in some areas, domestic violence homicides have more than doubled.

Less alone time has also made it harder for victims to access help, as they are unable to escape the watchful eyes of their abusers (the National Domestic Violence Hotline’s website has a quick-exit button on every page to address this devastating reality).

But one universal truth holds both pre-pandemic and now: The number one obstacle to escaping an abuser is financial insecurity.

Our federal leaders have an opportunity in front of them. They can move forward with a standard solution for financial support during this pandemic. Or they can recognize our current reality and build legislation that addresses the needs of those most at risk, those our systems have pushed to the farthest margins. By doing so, they can design a solution that takes care of nearly everyone—including women and children facing quarantine with an abuser.

What does such a program look like? To combat the financial control abusers exert over domestic violence victims, relief measures should use distribution methods that limit an abuser’s ability to isolate his victims by denying him access to existing bank accounts and credit cards. Rep. Rashida Tlaib’s Automatic Boost to Communities Act outlines the use of pre-loaded debit cards that are unique and specific to stimulus support.

This means women would receive their own cards with their own money.

Rep. Tlaib’s proposal outlines distribution of cards via easily accessible public locations, further ensuring funds get into the hands of their intended recipients.

A young woman suffering from domestic violence stands alone in the bay window of her home. (Photo by In Pictures Ltd./Corbis via Getty Images)

Monthly $2,000 checks for the duration of this pandemic would also provide a critical lifeline to victims of domestic abuse. Most abuse survivors have only $250 in savings. These were the findings of a recent report by FreeFrom, a group that focuses on the nexus of intimate partner violence and economic security that has given out thousands of cash grants to survivors throughout the pandemic. Abuse survivors are also four times more likely than the average adult to have faced food or housing insecurity in the past year.

Survivors report the pandemic has made things worse, from the stress of having fewer financial resources to slowed court proceedings delaying critical income like child support.

FreeFrom also found that the average survivor needs just $730 right now to stay safe. Stop and think about that for a moment. In a country that can find billions for corporate bailouts and trillions in tax cuts for the wealthy, it is nothing short of shameful to ask women and children to quarantine in abusive conditions for lack of money.

Instead, what if this economic crisis and health pandemic became an opportunity for women and children to leave a violent situation? What if our leaders wrote legislation that would consider these most vulnerable members of our community?

What if this pandemic was, instead of a prison sentence for these women, an opportunity for independence and freedom?

One $2,000 deposit onto an accessible debit card would pull them out of harm’s way. Recurring checks throughout the pandemic would make sure they have the financial security to stay safe and build new lives. And it would help the vast majority of those facing economic precarity during this pandemic as well.

I know that access to financial resources would have given my mother the ability to leave my stepfather far sooner. I cannot change that for her. But I can fight to make sure that families in the same situation today have the economic security that paves their path to safety.

I should not be alone in this fight. I urge the Biden administration and Congress to join me and protect our country’s most vulnerable by providing a literal lifeline to those who need it most. Pass legislation for monthly stimulus checks today. Support those who need it most during this devastating time.

Stacey Rutland is the founder of Income Movement, an organization that’s been at the forefront of the fight for recurring stimulus checks.

President Biden, the House Ways & Means Committee, and Senator Mitt Romney (R-UT) agree: They want to increase child benefits to parents who work and those who do not, and they want to deliver benefits regularly throughout the year rather than waiting until families file their tax returns each spring.

But what federal agency should administer such a program—the IRS or the Social Security Administration (SSA)?

Neither SSA nor IRS is the obvious best choice. In the short-term, the IRS holds a slight edge: It has political support and expanding a program is easier than starting a new one. In the long-term, SSA may be better because it has experience delivering monthly payments and shifting benefits when families change. But transitioning from a tax credit delivered by the IRS to a child allowance delivered by SSA might prove difficult and should be done cautiously.

What is the proposed policy?

The House Ways & Means Committee and President Biden would make the child tax credit (CTC) fully refundable, which means even very low-income families would get the full credit. This is a departure from current policy. The credit would continue to be administered by the IRS, but it would be delivered monthly or quarterly.

Romney, by contrast, has his eyes set on a monthly child allowance administered by SSA.

Which agency would likely reach more children?

Any new benefit will succeed only if it can actually reach children. The IRS now delivers a tax benefit to 95 percent of all families with children. About half of the children it misses are in high-income households that are ineligible for the benefits.

But half are in low-income households that would mostly be eligible for the expanded CTC. Some children live in households that don’t file a tax return because their income is too low, even though tax is being withheld from their paychecks. Others may live in households that file a return but are ineligible for a benefit because they do not meet all the eligibility criteria.

Reaching children whose parents don’t file taxes will be difficult for the IRS. In 2021, this might be simpler than in years past, since some families either used the IRS non-filer portal to claim an economic impact payment or received a COVID relief payment based on information the IRS received from SSA. Either way, the IRS has reasonably recent information on those families.

SSA has a more complete registry of all children since almost all parents apply for a Social Security Number for their newborns. But SSA has little current information about where to send payments.

Even if it could match children with parents, SSA still would not know where to send the payments since it generally does not track address changes for children. The one exception: SSA does send payments to 6.5 percent of children who are eligible for a monthly benefit from Social Security. But that’s not much of a base to work from if the Administration wants to stand up a program quickly.

Which agency would be better at delivering regular payments?

Monthly or quarterly payments would be much more helpful for cash-constrained families than annual ones. My TPC colleague Howard Gleckman and I suggested the IRS could administer the advance payments – but only with substantial additional resources.

SSA, on the other hand, already delivers payments to about 69 million people each month. A universal child allowance would double its workload. Still, while both agencies would need time and funding to deliver a monthly child benefit, SSA is closer to reaching this goal than the IRS.

Which agency can adjust to changes in family structure?

Family structure evolves throughout the year for many people. Parents marry and divorce. Children move among different households. As a result, advancing the child tax credit means some people will receive payments for which they will be ineligible while others may receive less than they are owed.

The Ways & Means legislation allows that some CTC payments made in error will not need to be paid back, limiting the risk that low-income parents will face a surprise tax bill when they file their returns. The legislation would not provide payments until July, so advance payments may not present a problem this year.

But changes in family structure that lead to erroneous payments would be an issue if Congress continues the program. The annual nature of filing a tax return limits the IRS’s ability to deliver a partial credit to multiple households caring for a child over the course of the year.

SSA determines eligibility for some benefits monthly, and it can respond to changes such as when a child who receives Supplemental Security Income (SSI) moves from one household to another. In that case, the benefit could follow the child. It does not have a system to track changes in family income so may not be able to react in real time to a benefit that phases out with income.

Are payments from SSA treated differently than tax credits from the IRS?

In general, benefits delivered through the tax code by IRS don’t count as income for purposes of determining eligibility for other federal benefits such as Supplemental Nutritional Assistance Program (SNAP, formerly food stamps). Payments from SSA, on the other hand, typically do count as income when determining eligibility for other benefits.

Congress could make an exception for a child allowance administered through SSA, but that might be confusing for those receiving both child payments and, say, SSI. Legislators would need to be careful transitioning from a tax benefit to a child allowance, making sure to minimize unintended consequences.

Over the long run, SSA’s flexibility and its experience delivering monthly payments might make it the better agency to deliver a regular child benefit. But if lawmakers want to stand up a program quickly, IRS seems like the better bet.

Walmart CEO Doug McMillon said more customers spent their recent stimulus checks on necessities, such as groceries, rather than big-screen TVs.

He said the spending patterns indicate that more families are hurting and need help.

The retail chief stressed that message when he met with President Joe Biden last week.

When Walmart CEO Doug McMillon went to the White House last week, he said he gave a clear message: Americans urgently need another round of stimulus checks.

Walmart’s stores and websites reflect consumers’ spending patterns, the retail chief said in an interview with CNBC’s Courtney Reagan on “Squawk Alley.” The company could tell when they stocked up on food and cleaning supplies in the early part of the Covid pandemic and gravitated toward bikes, puzzles and hair color as they remained stuck at home.

When consumers got the most recent stimulus checks at the end of the year, he said a new pattern emerged: more shoppers put the extra dollars toward buying necessities.

“We can see in our customer behavior that some customers — as they received this most recent stimulus — are spending it more on basics, more on private brands, smaller pack sizes, things like that as opposed to some of the stimulus dollars that came out earlier last year that were spent more like tax rebate checks, where people were buying televisions and things to entertain themselves at home,” he said.

“There’s a bit of a mix shift now and we think it reflects the fact that customers out there do need some help.”

McMillon met with President Joe Biden and Treasury Secretary Janet Yellen last Tuesday, along with JPMorgan CEO Jamie Dimon, Gap CEO Sonia Syngal, Lowe’s CEO Marvin Ellison and Tom Donohue of the U.S. Chamber of Commerce. He said he urged help for American families and small businesses during that meeting.

The current bill calls for direct payments of $1,400 per individual, or $2,800 per married couple, plus $1,400 for both child and adult dependents — but lawmakers are still hammering out a deal and numbers could change.

If approved, it would be the third direct payment to Americans since the start of the pandemic and the largest check so far. The government sent payments of up to $1,200 in the spring and another that was up to $600 in December, but the amounts and eligibility were based on a person’s income.

As a major retailer, Walmart would benefit if customers have more money in their pockets.

Its chief financial officer, Brett Biggs, told CNBC that its fiscal fourth-quarter earnings got a lift from stimulus payments and it would expect similar results if consumers get another check.

Yet McMillon said he stressed stimulus checks during his Oval Office visit because of what he has seen and heard at the company’s stores.

He said some families have increasingly dire financial circumstances as they struggle to find work.

McMillon said he recently spoke to a customer who was trying to stretch $20 to cover all of his expenses for the last week of the month, from groceries to gas.

“Those customers are the ones that the stimulus package needs to go help and go help quickly,” he said.

The expert panel would have benefited from a political scientist or, heaven forbid, one or two people actually living in poverty sharing the pen.

By Hugh Segal

A recent report of the British Columbia Expert Panel on Basic Income prepared over two years by three economists, two from B.C. and one from Alberta, has given encouragement to long standing opponents of a basic income.

In some ways, however, the very nature of their sixty-five recommendations for program changes in income security and related programs in B.C. undercuts the anti-basic income orientation of the report itself. The analysis and recommendations of the report do appear to have the authors bumping into themselves while coming around the corner.

They are right, of course, in one central conclusion: basic income is not affordable by any one province on its own.

Important pillars of Canada’s poverty reduction program, the Guaranteed Income Supplement for seniors, and the Child Benefit for low-to-modest income families with children are national programs administered by Ottawa. They are successful and efficient — and did not and do not require building new administrative capacity to administer them, now, or in the future — as would be very much the result for the multi-program fix called for by the B.C. expert panel.

The other rather intriguing conclusion from the content of the report, was the agreement of all three panel members to downplay the value of “autonomy” for those in poverty who might be lifted out of poverty by basic income.

Better, the report concluded, to shower the poor with a myriad of different programs, each incrementally adjusted or improved over the present version, in the belief that will create the village necessary to help the poor.

It is the classic government conceit, that if “we build it” they will come — the “they” here being the poor with no other choice.

Our First Nation brothers and sisters understand the sound of “the crown knows best” trumpet. It is simply a colonialist response that denies poor Canadians the life choices, however modest, that a basic income would provide.

The B.C. report embraces costing of a basic income with assumptions about the option of sending a cheque to everyone, whether needy or not, and taxing back the excess from those not in need.

There are few proponents in Canada of this Andrew Yang-style American proposal.

As is the case with the Guaranteed Income Supplement and the Child Benefit, that has not been the Canadian way. Our tax system is an excellent way of determining need, through the statutory filing we all make, and enhanced automatic filing now being considered by Ottawa.

The Guaranteed Income Supplement for those over sixty-five is based on the premise that every senior needs around $1,500 monthly ($2,400 for a couple). The gap between what they do have and $1,500 is topped up by the supplement — the opposite of “the same cheque for everyone” as opponents of a basic income allege. Recipients will need different levels of top up, and that is exactly what happens now.

The B.C. report buries very little of the compelling case for basic income by questioning the improvement in health outcomes that would accompany using a basic income to lift the poor into the mainstream.

The three economists set aside decades of empirically reviewed literature on the social determinants of health.

Most disappointed at the report are the members of the B.C. Green party, whose alliance with the New Democrats allowed the Liberal government to be replaced without an election. They sought action on the basic income, as a condition of that alliance.

The B.C. NDP government may well use the expert panel as a rationale to do little if anything other than tinker incrementally with a myriad of programs.

Poverty levels in B.C. will not come down as a result of any of report’s recommendations.

There are lessons here for those who care about government and the quality of expert advice it seeks and, on occasion, receives.

The expert panel would have benefited from a political scientist or, heaven forbid, one or two people actually living in poverty sharing the pen.

Even Adam Smith, the market and society theorist from the eighteenth century, whom they cite in their anti-basic income rationale, might well have told them that.

One woman’s work to get UBI onto the screens and into the hearts of Americans.

By Diane Pagen

People who care about winning a Universal Basic Income (UBI) have done many things to push it into the public consciousness and onto the desks of public servants. Over the years, a host of things including flyers, street outreach, interviews, calling elected officials, public art, community groups, conferences, demonstrations, and now many online activities are ways people have worked to move progress on UBI.

No one ever thought of doing a Public Service Announcement (PSA). Until 2021. Until Gisèle Huff.

I remember PSAs when I was a kid. They were short and to the point. They helped people understand important community problems, and solutions. They appealed to our desire to be a community. There was one to remind kids to be kind to seniors; one to remind people how to cross the street (“cross at the green, not in-between”); to be a good friend (include the new kid at recess); to pick up your trash (“don’t be a litterbug!”) and to guard against prejudice (we need to bring that one back).

Gisèle Huff’s project to create a PSA for a Universal Basic Income began more than a year ago. Her late son, Gerald Huff, was a proponent of UBI for many years before his death in 2018.

The grief Gisèle endured and her desire to continue Gerald’s legacy led to her declaration that she would continue to work for the world Gerald envisioned — one where people’s basic needs were met so they could fully realize their talents and humanity.

Gisèle established the Gerald Huff Fund for Humanity to advance work toward a national UBI.

In conversation, she explained to me how she re-connected with one of her late son’s childhood friends, who is now active in public relations and advertising. They talked about her idea for creating a PSA. This led to introductions to a marketing team that was excited to work on a PSA as Gisèle envisioned it.

The PSA launched Thursday, January 14th and has reached almost 3 million viewers during its broadcast across the digital space, which has included airtime on news organizations sites like The Wall Street Journal, Buzzfeed, Vice and more.

Who are the target demographics for this PSA? “Young people, and people of modest incomes or low-incomes with children are some of the people who most need to see this and hear its message,” Gisèle said. “Also, people who have so-called ‘good jobs,’ because over the past several decades, job security has eroded. The person with a ‘good job’ is more and more finding themselves on the losing end of the employer-employee equation. A Universal Basic Income will provide the income security that will matter as traditional job security disappears, exacerbated by increasing automation.”

The second group of people who need to see it, Gisèle explained, are politicians. “Our biggest problem is our leadership. They are stuck in the 20th century and they can’t seem to climb out on their own.” The PSA will help politicians and leaders connect our current economy to the experience of the American people and help them think about “earned” income in new ways.

“With COVID, workers in low-paying jobs, who were previously thought of as expendable, are now recognized as ‘essential,’’ Gisele continued. “A Universal Basic Income is a great way to recognize worker value with tangible cash to meet their own needs.

“When we look at our economy in highs and lows, every single person is essential. We need to start demonstrating that we know this through our economic policy.”

Gisèle is 84, with a lot of lived experience. She emigrated to the U.S. from France as a child with her mother, after living under Nazi occupation during WWII. They came knowing no English and with $400 to their name. From that humble beginning, as Gisèle explains, “it was possible for me to climb the economic ladder as the epitome of the American Dream.”

“Back then, the economy was very different. A worker was able to advance with relative security. I was able to succeed in that economy. But we are telling today’s workers a lie — that that model of work and economic reward is still the foundation of America’s economy. It isn’t that way anymore.”

Despite the disastrous toll that COVID-19 has had on the world economy, there continue to be those in power who insist the traditional job market is still intact. Resistance to cash relief by some in Congress is proof that many leaders are so detached from ordinary people that they do not see the economy clearly. The PSA invites people to undergo a “mind shift” in how they think of their own worth, and the worth of everyone else, friends, neighbors, even strangers.

The PSA says simply that Universal Basic Income is the way forward for American society.

“We must communicate that the way to show that our society is really one that values people is to legislate it,” said Gisèle, “with a Universal Basic Income.”

Recurrent, direct payments should be a permanent part of the U.S. recession-fighting arsenal.

Opinion by Mark Blyth

Early in the COVID-19 pandemic last year, just one month after dropping out of the U.S. presidential race, Sen. Bernie Sanders (I-VT) took a clear and bold stance for families:

$2,000 monthly checks until the crisis is over.

Sanders’s fight for direct checks is right, as checks are a much needed lifeline for families in the midst of the COVID-induced recession. But there’s more that must be done.

So let’s ask the bigger questions here. Why on Earth in the year 2021 are we relying on checks? And why do we have a political bun-fight over this issue every time it happens?

First, checks. Really? Practically every American has a smartphone. There are tons of banking apps from Paypal to Zelle to Venmo. The U.S. Treasury has a website called Treasury Direct that allows anyone to set up an account to buy Treasury bills and bonds.

The government could simply reverse the direction of those transactions and send cash from the Treasury to those account holders.

No holdups in the mail. No missing addresses. Best of all, we could make it recurring.

We have all heard about the “K-shaped” economic recovery that the U.S. is experiencing. The top 20% of U.S. society commands 80% of the wealth. Whenever that is threatened by a market crash or a pandemic, the Fed swings into action to provide “support” for those markets. What that really means is buying lots of bonds and flooding banks and businesses with cash to stabilize them. The Fed can even promise to buy certain types of assets, such as corporate bonds, to stabilize their price.

The Fed is able to do this because its “pipes” flow from the Fed to the big banks and then out to big firms. The Treasury, what the rest of us rely on, has no pipes, hence the checks.

This is not only unfair — boosting the price of assets held by society’s richest citizens while telling the vast majority to wait for a check is a first-rate inequality booster.

It’s also harmful and needlessly expensive. Recognizing this, we should rethink our financial plumbing and the purpose of our pandemic response. Not just for this crisis, but for the future.

Let’s start with the basics. Can we please stop calling them stimulus checks? That makes them sound like a party drug. They are not. They are better thought of as insurance checks. Why? Because by insuring families against job and income loss, you stop an already bad recession from becoming a deeper crisis.

It simply makes sense to insure society against depressions and families against bankruptcies.

Second, rather than pumping hundreds of billions of dollars into the banking and corporate sectors, somehow hoping that this will impact employment, let’s make these insurance payments electronic, automatic and targeted at families up to the 60th percentile of the income distribution.

Congress can set an employment target such that when U.S. unemployment reaches a certain level the Treasury automatically sends out checks. When the target goes back to its pre-recession peak, the checks automatically stop. This would impact families directly, and given that they will spend what they receive it will not all end up pumping up an asset bubble and ever greater inequality with it. This would be far cheaper than what we currently do and far more effective. It would give the Fed less to do and target Treasury resources far more effectively. Worried about cost or even future inflation? Easy. Once we return to the target, raise taxes. Both problems are solved.

Direct payments to families are effective. The first check issued in the spring of 2020 was a primary reason that U.S. poverty fell at the start of the recession.

But as the money ran out, up to 8 million people were forced into poverty. As chair of the Senate Budget Committee, Sanders has the opportunity to continue to lead the fight to get money to those most impacted by the pandemic — and make sure it continues until the crisis is over.

But Sanders should push his Senate colleagues and President Joe Biden to make recurrent electronic payments to the bottom 60% of American families a permanent part of the U.S. recession-fighting arsenal. This is the 21st Century, so why are we using a 19th Century technology (the check) to fight today’s economic problems? That’s politics — and it’s politics America can do without.

_____

Mark Blyth is the William R. Rhodes ’57 Professor of International Economics; The Watson Institute for International and Public Affairs, at Brown University.

Giving people money is a proven, fast, equitable strategy to spur economic recovery. The truth is, we need recurring stimulus checks in addition to established progressive policies.

The hole America faces is deep and getting deeper every day as COVID-19 cases mount and the economy struggles to restart. Which is why Washington must think bigger for the recovery package. The biggest danger right now is doing too little, rather than too much. President Biden’s leadership on bold relief comes at a crucial time.

The idea of $2,000 stimulus checks has exploded in popularity over the past few months. Georgia Senators Jon Ossoff and Rev. Raphael Warnock ran, and won, in large part on checks. President Joe Biden committed to introducing legislation for additional direct payments to families.

While a one-time stimulus check is critical to help people in the midst of the pandemic, for a real and sustainable recovery, we’ll need recurring checks until the crisis is over.

Giving people money is a proven, fast, equitable strategy to spur economic recovery. The truth is, we need recurring stimulus checks in addition to established progressive policies—like unemployment insurance and the Child Tax Credit and Earned Income Tax Credit—that uplift all Americans, especially communities of color, until this pandemic is over.

The jobs crisis is severe and worsening: According to recent data, US employers cut 140,000 jobs in December. All were held by women, while men gained employment. On top of that, women ended 2020 with 5.4 million fewer jobs than they had in February, before the pandemic began, while men lost 4.4 million jobs over that same time period.

And beneath this gender disparity was another problematic difference in job loss; Black and Latinx workers lost more jobs in December than their white counterparts. That’s a major blow, considering that Black and Latinx households are twice as likely to have difficulty paying their bills. They also face higher levels of food insecurity, COVID-19-related mortality, and business closures than their white counterparts.

Families experiencing economic hardship need relief that is both fast—the IRS can get money into most Americans’ bank accounts in a matter of days—and sustained. Bills keep coming, and the checks need to keep coming too: Data suggests the CARES Act checks ran out for many families after a couple of months. The programs we already have are essential to expand but we need to do more — and faster. Expanding unemployment insurance essential, lifesaving for workers who get it, but it’s not reaching most of the people who have lost income. Urban Institute estimates that regular checks could keep 3.5x more people out of poverty than unemployment insurance alone. In other words, while these essential programs complement direct checks, they are not alternatives.

Alongside unemployment insurance, a relief proposal at the scale of the crisis should include the promised $2,000 check, followed by additional checks of $1,000 or more, monthly or at least quarterly, until employment approaches pre-pandemic levels. We can target this relief to families who need it and will spend it – to help those who are struggling and drive the recovery.

The Urban Institute research shows that just one more $1,200 stimulus check could keep 8 million Americans out of poverty, while two more checks could save 14 million from falling into poverty.

Imagine what monthly checks could do for struggling American families. Direct checks targeted to the bottom income earning half of households would also ensure those same families aren’t left behind, and would disproportionately benefit Black and Brown families hit hardest.

If relief is big enough, Brookings analysis confirms, direct payments would have a greater impact on our GDP in the immediate term than many other major policies under consideration.

We’ve learned this lesson before. The Obama-era 2009 Recovery Act was too small, and a decade later many Americans still struggled. Many economists agree that the Recovery Act fell short of delivering a speedy recovery and the decisive political win that would have come with it, because it wasn’t sustained enough or visible enough to everyday Americans (and thus was often viewed as a corporate bailout).

President Biden appears to understand: we must avoid that mistake this time and “failure to do so will cost us dearly.” Checks make government support visible to Americans. We must not underestimate the power of putting money in people’s pockets at a time when so many are barely scraping by.

The economic conditions facing most Americans are getting worse, not better. We should target checks to those who need help most and who will spend it to spur the economic recovery. But a one-time check will only last people a couple of months, at most. To truly build back better, we need recurring payments until the crisis is over. People who are going without food, medicines and electricity cannot afford to be held hostage to political games in Washington. They need steady and regular relief, and it is the duty of our president and Congress to provide it to them. It’s good economics and the moral thing to do.

_____

Foster is the co-founder and co-chair of the Economic Security Project, an organization focused on cash-based policies, guaranteed income and curbing corporate power.

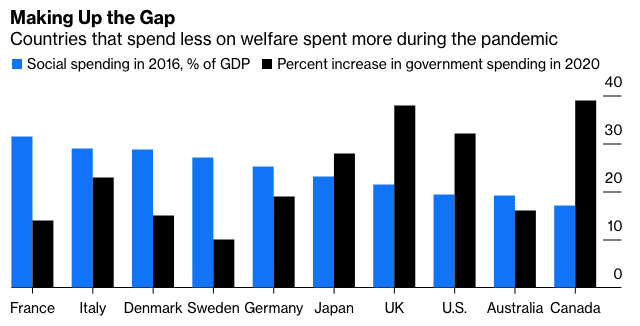

Americans are strongly in favor of a very large Covid-19 relief bill. It seems likely that this enthusiasm reflects more than just anxiety over the pandemic; many Americans are fed up with decades of a stingy welfare state, and in this crisis they finally see an opportunity to make back some lost ground.

A recent report by McKinsey & Co. found that countries that generally spend less on social welfare ended up increasing their government spending by more during the pandemic. A look at the data shows this relationship fairly clearly:

Source: OurWorldinData.org

The Anglosphere countries — the U.S., U.K., Australia and Canada — tend to do substantially less social spending than European countries like France, Germany and Sweden in normal times. But the U.S., UK, and Canada boosted their spending much more in 2020 than those other countries (Australia did less, but probably just because it wasn’t hit as hard by the virus).

Thus, the pandemic relief package was so big precisely because it had to be — there was not as much of a pre-existing safety net to catch Americans when they lost income due to the pandemic.

Not surprisingly, a recent Quinnipiac Poll showed 68% in support of President Joe Biden’s new $1.9 trillion relief proposal.

The most popular spending measure, according to a recent YouGov survey, is the broadest one: a one-time payment of $2,000 per family member. Biden’s actual proposal calls for an additional $1,400 on top of the $600 already allocated in the December relief bill.

Although some on the political left are demanding much more, $2,000 per person is actually a lot of money. Real income per capita in 2020 was only $2,300 lower than in 2019. Thus, a $2,000 payout to every person in America, combined with the previous $1,200 payout in the Cares Act, would more than cancel out the entire 2020 income loss from the pandemic, on average.

Of course that’s just an average. Many people have suffered far worse drops in income, usually as a result of unemployment. But remember that the cash handouts are far from the only form of relief.

There’s also the special pandemic unemployment benefit, which was so generous that poverty actually fell during the darkest early days of the pandemic. There were also supports for businesses to keep workers on payroll, as well as various other forms of aid. Globally, the U.S. has been above average in its generosity with overall aid during the pandemic, and Biden’s bill would move us further up the rankings.

The very generosity of the Cares Act seems to have awakened something in the American psyche. It was the most transformative, effective government social program since the creation of Medicare in 1966. And it was so simple: the government just gave people a bunch of cash. It appears to have vindicated the refrain of those who have been calling for the U.S. to increase the welfare state by adding direct cash benefits rather than expanding the typical thicket of vouchers and conditional aid.

People want more.

After decades of cuts to welfare programs, austerity in the middle of recessions, and hectoring lectures about how the American people don’t deserve government bailouts, the Covid-19 relief effort has finally helped Americans to realize that the government can just send them cash, and that this makes their life better.

They’re not ready to stop at a measly $1,200.

And yet while helpful in the short run, cutting Americans $2,000 checks won’t fix the underlying problem of the welfare state. If the U.S. is going to add cash benefits to the current mix of government rograms, it needs to add them on an ongoing basis. This is what Biden’s child tax credit proposal and Senator Mitt Romney’s even more generous counter-proposal are all about.

Though it’s not quite a universal basic income, these cash payments — $3,000 to $4,200 per year for each child in a family — would be very widely targeted.

They represent the country’s best shot at the dream of a bigger but simpler welfare state. So one-time $2,000 checks are fine, but child tax credits would be a much more enduring way of giving Americans a boost.

As Congress debates a new COVID-19 aid package, millions of Americans are struggling to pay for rent, groceries, utilities and medical bills, or to keep their small businesses from shutting down.

We know their needs are both large and urgent because they tell us about them.

Since March, an American has started a COVID-related fundraiser on GoFundMe every two minutes. It’s not something they do lightly. Asking for help is difficult. People do it when their needs are dire and they have nowhere else to turn.

In fact, when the pandemic began, 1 in 3 fundraisers on GoFundMe were related to COVID-19, and the activity has persisted at an alarmingly high rate.

Their pleas have turned GoFundMe into a leading indicator of the biggest pandemic-related hardships. Even before the weekly jobless claims, the monthly unemployment numbers and the quarterly gross domestic product reports tell us the state of the economy, we at GoFundMe learn firsthand about the real struggles Americans face.

Surge of people asking for help

It will surprise no one, then, that in the past year, we’ve seen an unprecedented surge in fundraisers of all kinds, as the economy tanked, millions lost their jobs and nearly 1 in 4 families faced food insecurity.

From March 1 to Aug. 31 alone, people started more than 150,000 fundraisers for COVID-related assistance on our site, and the requests for help have yet to abate. Last month, even after Congress passed a second relief bill in December, the number of new fundraisers on GoFundMe was higher than in May during the first wave of the pandemic.

The situation is nothing short of a national emergency. Congress should treat it as such by quickly passing a large relief bill whose generosity is commensurate with the need.

We’ve known for years that most Americans don’t have $500 to spare to cover unexpected emergencies, like a car breakdown. Now, it’s as if their entire lives are breaking down again and again and again. The scale and variety of the fundraisers we see point to the level of desperation among Americans and give us a window into where the relief could be most helpful.

Monthly bills. In October, after seeing a steady rise in fundraisers from people struggling to pay bills like rent and utilities, we created a new category for those on our site. In just a few months, it has grown into one of the largest categories on the platform, accounting for 13% of fundraisers.

A new round of stimulus checks would help scores of needy families, like that of Martha Zepeda of Houston. While Zepeda, a single mom who has struggled to make ends meet throughout the pandemic, has been out of a job for three months, she didn’t tell her daughter, Alondra Carmona, a high-school senior. By the time Carmona found out earlier this month, they were two months behind on rent and faced a likely eviction in March. Carmona, who has been accepted to prestigious Barnard College, decided to put the entirety of her college savings to support her family. “As much as I dream of going to Barnard College, it is not looking promising right now,” Carmona wrote on GoFundMe, as she sought to raise the money she needs to make that dream a reality.

Restaurants and small businesses. During 2020, fundraisers seeking donations for small businesses — previously a rarity — became commonplace: 3 of every 5 COVID-related fundraisers in the United States sought to support small businesses and their employees, with restaurants alone accounting for tens of thousands of fundraisers. After ebbing during the summer months, fundraisers for struggling restaurants spiked anew toward the end of the year.

Many are small family-owned businesses like Ray’s Ice Cream, which has served its community in Royal Oak, Michigan, for 63 years, employing thousands of local youngsters along the way. Last year, as sales to restaurants flatlined and COVID-19 restrictions forced Ray’s to close, it faced the prospect of having to lay off its employees. “I would love to make payroll for all these great kids that work for me,” owner Tom Stevens wrote on GoFundMe.

Food. It’s no secret that hunger and food insecurity have risen sharply during the pandemic. As millions turned to food banks across the nation, we also saw a sharp increase in fundraisers from people seeking help to cover their next meal. After spiking in April, the fundraisers for food leveled off at rates that are far higher than typical. In January, for example, they were 45% higher than a year earlier.

These are hardly the only areas of need. We’ve seen high-profile appeals for support for renters facing eviction, front-line workers who need personal protective equipment and a never-ending stream of fundraisers aimed at supporting students, classrooms, charities and more. The surge in these types of fundraisers is a direct result of government programs coming up short.

We are pleased that the fundraisers for Ray’s Ice Cream and Alondra Carmona resonated with the GoFundMe community. Donations to Ray’s topped $78,000, allowing Stevens to make payroll and keep the store open. And in just a few days, Carmona easily surpassed her goal of raising $75,000 so she can pursue her dreams of a STEM education at Barnard.

They’re not alone in benefitting from the kindness of relatives, friends, neighbors and even strangers. Someone makes a donation on GoFundMe every second.

Much of it comes from regular folks: 70% of donations are for less than $50. And we’re stepping up, too, donating millions to family and business relief efforts through our charitable arm.

We are proud of the role that GoFundMe plays in connecting those in need with those who are ready to help. But our platform was never meant to be a source of support for basic needs, and it can never be a replacement for robust federal COVID-19 relief that is generous and targeted to help the millions of Americans who are struggling.

Last spring more than 50 members of the Senate of Canada urged the federal government to implement a guaranteed basic livable income program. At the same time, a special committee of the Prince Edward Island legislature called on Ottawa to join the province in creating a guaranteed livable basic income (GLBI).

Doubters suggested a GLBI would be too costly, and too complicated. They’d prefer tinkering with the status quo. The GLBI idea seemed stalled.

Faced with this hurdle, a group of Island Senators has written Premier Dennis King and Prime Minister Justin Trudeau to suggest a way to end the stalemate. Why not start with a small pilot project in Prince Edward Island?

In our letter we reminded Mr. Trudeau that Prince Edward Island’s modern economy is a result of an innovative 1969 federal-provincial program called the “P.E.I. Comprehensive Development Plan.” Ever since, successive governments have used P.E.I. (population ~150,000) as a “test bed” for important innovations in agriculture, fisheries, energy from waste, wind energy and so on.

Now out of the economic disruption caused by COVID-19, P.E.I. and the federal government have another historic opportunity for social innovation. The arguments for a GLBI are well-known and are persuasive, especially in an economy like PEI’s with an ageing demographic.

Last week the British Columbia government stepped away from the GLBI idea because of the plan’s perceived potential shortcomings. A pilot project in P.E.I. would test those concerns and allow the program to be adjusted as needed.

Critics may argue against an incremental approach, but we should not forget that medicare, our most successful social program, began incrementally, one province at a time starting with Saskatchewan.

In 1984, the Macdonald Royal Commission recommended a GLBI as a counterbalance to the negative effects of free trade with the United States. The Mulroney government passed free trade, but ignored the rest of Macdonald’s report.

Mr. Trudeau now has an opportunity to finish that work and, in so doing, turn the page on the economic devastation caused by COVID-19 and build a brighter future for P.E.I., and one hopes, eventually for millions of Canadians.

The government response to the economic disruption caused by the pandemic was a scramble, with some covered and others not. Had a Guaranteed Livable Basic Income been in place, Canadians would have been automatically protected.

We closed our letter by urging Mr. Trudeau to begin Canada’s post-pandemic recovery with a pilot GLBI program in Prince Edward Island, the birthplace of Confederation.

A guaranteed livable basic income truly is – an idea whose time has come!

_____

Diane Griffin, Brian Francis and Mike Duffy are Senators for Prince Edward Island.

When governments in developed countries like the U.S. and Britain provide extra support for low-income people through tax credits and more generous unemployment benefits, individuals’ mental health and wellbeing generally improve, according to a new paper by a group of U.K. researchers.

By contrast, however, introducing benefit restrictions like work requirements and time limits generally worsen mental health.

The conclusion, which is based on a comprehensive review of published quantitative observational studies over decades, has increased importance as the coronavirus pandemic and accompanying economic turmoil has led governments around the world to overhaul social assistance programs.

“Changes to social assistance policies, reductions in those, were a very common policy that was studied, and were mostly related to detrimental outcomes in terms of mental health,” said lead author Julija Simpson, a Ph.D. student at Newcastle University.

Simpson wrote the paper, which will be published in the March 2021 issue of Social Science & Medicine, alongside Newcastle University colleagues Viviana Albani, Zoe Bell, Clare Bambra and Heather Brown.

The paper comes as U.S. lawmakers consider overhauling the child tax credit system, and the U.K. is mulling additional austerity measures that would cut unemployment benefits, possibly sending hundreds of thousands of British children into poverty.

Simpson said the mental health implications of these policies must be considered alongside other health and economic concerns.

“We’re all vulnerable to what happens, and it could be the global pandemic or it could be your own life circumstance, but we all need social security,” said Simpson. “If you’re always concerned with survival, then you can’t really do much else.”

The paper was the first review to systemically examine the effects of social security reforms on mental health, meaning the researchers synthesized a variety of past quantitative studies on the topic rather than conducting their own.

To do this, they searched several academic databases for studies on the topic between January 1979 to June 2020, coming up with more than 20,000 results. They then used screening criteria to narrow the sample down to just 38 studies.

“Because I tried to be quite careful not to exclude any relevant studies, the search terms were relatively broad,” said Simpson.

Out of the studies, 21 examined social welfare expansions and 17 evaluated contractions.

Eight of the studies examined the Earned-Income Tax Credit — or EITC — in the U.S., a policy that subsidizes earnings for low-income families. Four of the studies found that expanding the EITC significantly improved mental health outcomes. An additional study found that introducing a high-rate state EITC reduced the annual age-adjusted suicide rates by nearly 4%. Another study on suicides, however, contradicted this claim.

Two studies also examined an EITC-like “welfare-to-work” program from the U.K. that expanded support for low-income families by providing more generous tax credits. Both studies showed a positive effect on mental health for low- income people.

“They were generally found to improve mental health for the recipients,” said Simpson of both the U.S. and U.K. policies, adding that tax credits are “a good way to improve both employment outcomes and health outcomes.”

The researchers also examined seven studies on 1990s welfare reform in the U.S., in which the federal government replaced the Aid to Families with Dependent Children program with a far more limited program called Temporary Assistance for Needy Families, which contained restrictions like work requirements and benefit time limits. Single mothers were most severely impacted by the changes, Simpson said.

The seven studies were mixed, with some showing a significant deterioration in mental health and others showing no effect.

“Those studies mostly showed that [the reforms] had negative effects on mental health,” Simpson said.

The researchers also examined studies on disability and retirement benefits and mental health, though with much smaller sample sizes.

In aggregate, the studies have a clear message, the researchers found: Expanding social welfare benefits improves mental health.

The review comes amid a rapidly growing academic interest in examining secondary and potentially unintended effects of social safety net policies. For example, University of Strathclyde economist Otto Lenhart has recently found that raising the minimum wage is associated with a drop in teen births and that providing paid family leave reduces child hunger.

Simpson said she plans to focus further research on ongoing social security reforms in Britain. She’s also interested in conversations around universal basic income in the U.S.

The paper, titled “Effects of social security policy reforms on mental health and inequalities: A systematic review of observational studies in high-income countries,” is forthcoming in the March 2021 issue of Social Science & Medicine and was made available online Jan. 18. The authors are Julija Simpson, Viviana Albani, Zoe Bell, Clare Bambra and Heather Brown of Newcastle University. Simpson is lead author.

The most visible—and popular—pieces of economic relief Congress has approved over the past year have been relief payments and enhanced jobless benefits.

The initial $1,200 payment, combined with the $600 weekly boost to jobless benefits, lowered poverty rates in the midst of a pandemic and worst economic crisis in 100 years.

Surveys of the American people throughout the past year have been consistent—there is overwhelming support for a stronger safety net—in the form of simple, straightforward relief—in the midst of a pandemic.

The American people recognize that their neighbors are experiencing unprecedented financial challenges through no fault of their own.

As Democrats move forward with President Biden’s American Rescue Plan, the income thresholds for relief checks are still being debated.

President Biden has proposed beginning to phase out the checks at $75,000 for an individual and $150,000 for a couple, which I also support. Let me explain why this is the right approach.

Families who have not experienced job loss are still struggling due to fewer shifts, less business, and new child care responsibilities.

Picture a couple with two children in elementary school. They made $140,000 prior to the pandemic. Dad made $75,000 and Mom made $65,000. Mom was able to work from home and managed work, remote school, and child care for months into the pandemic, but quit her job in October when she could no longer manage it all. That’s been the experience for millions of working women.

Now they are trying to make ends meet with half their previous income. Mom is hoping to begin looking for work when school reopens, but her children have fallen behind in school and she’s spending much more time helping them with their work.

This family would have received a relief payment in January and is surely counting on another one to help pay their bills and relieve some of the stress of their new situation.

While the IRS would use their 2020 income if they file early when determining whether they receive a relief payment, even their 2020 income does not reflect their current circumstances.

I agree with my colleagues that “high income” families should not receive help, but I don’t think they would consider the family described above as “high income.”

While they aren’t facing the same struggles as other families who have lost jobs, they clearly need more help.

New polling from Data for Progress and Groundwork Collaborative shows strong support for prioritizing getting relief out the door quickly, over even further targeting of payments—77 percent of Democrats, 61 percent of independents, and even 46 percent of Republicans—support getting checks out the door quickly and aren’t too concerned about whether families with a bit more of a financial cushion get additional relief.

The bottom line is that the American people recognize the unprecedented nature of this crisis. They know that families are experiencing their own unique challenges, which is why they strongly support being more generous with relief, not less.

_____

Senator Ron Wyden is the Democratic Chair of the Senate Finance Committee.

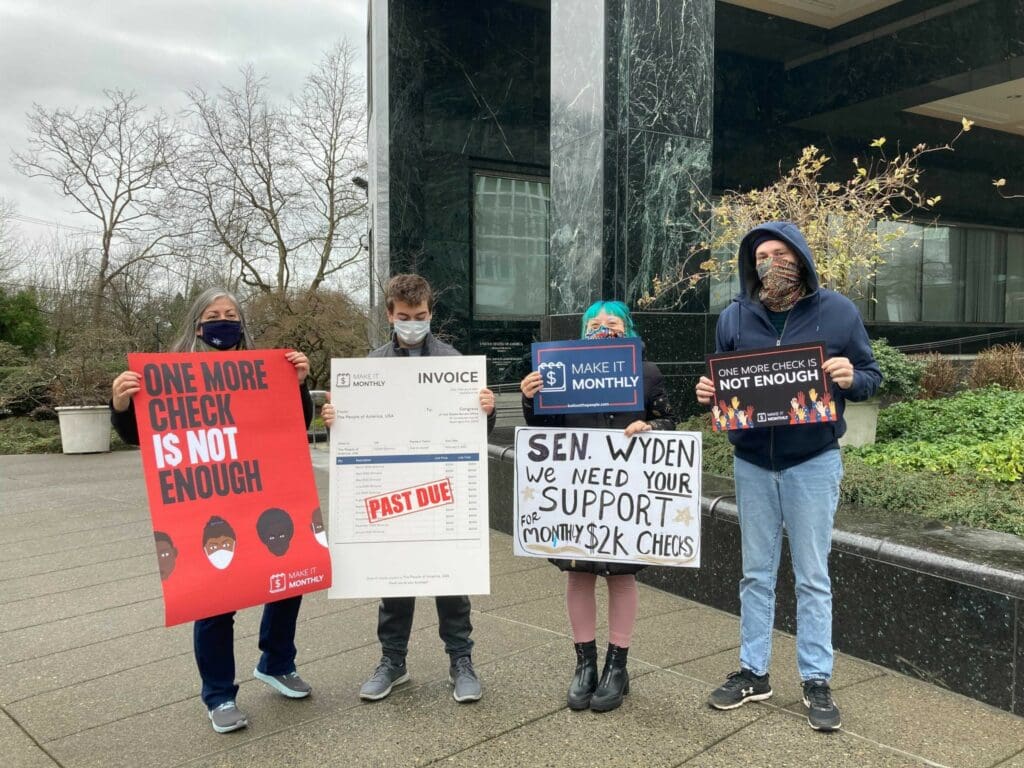

Members of Congress, mayors, organizers, small business owners, and individuals impacted by the pandemic participated in events across the country on Thursday, February 6th as part of a nationwide Day of Action demanding that Congress pass recurring $2,000 checks.

Recent polling shows that more than 80% of the public supports $2,000 checks, including 74% of Republicans. And 60% support recurring monthly payments of $2,000 until the pandemic is over.

The “Make it Monthly” Day of Action, organized by Economic Security Project Action, Change.org, Income Movement, and The People’s Bailout, included events in 12 states; a live, national conversation with Members of Congress, our very own Natalie Foster, and restaurant owner Stephanie Bonin; an ad in TIME from 33 mayors.

“Past Due” Events

The delivery of $2,000 “past due” invoices to 19 Members of Congress in 12 states by grassroots organizers and individuals impacted by the pandemic. The invoices contained the names of more than two million people who signed a Change.org petition asking Congress to authorize $2,000 monthly checks.

In Irvine, CA, activists met with staff of Congresswoman Katie Porter who accepted the invoices, and listened to stories from some UCI students and a constituent who had to close his business.

In Hanford, CA, Lemoore resident Aurora González delivered a message to Congressman David Valadao: Congress must include monthly stimulus checks in the next COVID relief bill. Oralia Vallejo of the Kings County Latino Roundtable noted that government COVID relief has not been sufficient, especially for the low-income residents who have lost their jobs as well as farmworkers.

“We really need this support so we can improve the lives of everybody.”

In Orlando, FL, organizers Erica Wright and Stacey Rutland from Income Movement delivered petitions representing 154,000 signers to the office of Senator Marco Rubio.

In Portland, ME, Lewiston resident Gina Morin, a volunteer with the Maine People’s Alliance, helped deliver 6,000 invoices to the office of Senator Collins.

In delivering the petitions, Morin said, “I know what it’s like to have been forced onto the street, and I’ve been working with other volunteers to help folks here in Lewiston but there’s only so much we can do.”

In Las Vegas, NV, organizers delivered petitions to the offices of Senator Catherine Cortez Masto. Nick Rampone with Humanity Forward said, “People just need [checks]. Our belief is that recurring cash stimulus, direct to the people, is the most effective way to do that.”

Live Conversation with The Appeal

Congresswoman Ilhan Omar (D-MN), Congressman Tim Ryan (D-OH), former Stockton Mayor and Founder of Mayors for a Guaranteed Income Michael Tubbs, Economic Security Project Co-chair Natalie Foster, and restaurant owner and Change.org petition organizer Stephanie Bonin, joined a live conversation hosted by The Appeal and NowThis, about how one stimulus check isn’t enough, and they should be recurring.

Congresswoman Ilhan Omar: “Every single day, our office is inundated with voicemails, emails from people who are desperately struggling to put food on the table, to keep a roof over their heads, just to survive…

“Many of us who have, unfortunately, known what real struggle looks like, which unfortunately isn’t that much here in Congress, can attest to the dire struggles that people are faced with, the anxiety that they’re living with, the desperation in their voices as they leave voicemails for us. And we have to do everything that we can.”

Congressman Tim Ryan: “This has been an issue from before the pandemic. We’ve seen income inequality continue to be exacerbated by globalization, by automation, by huge tax cuts over the past 20 years that went primarily to the top 1%. This has led to the level of income inequality that has been unsustainable for so many families.. The economy is clearly on the wrong track for 80% of the American people, and this is an opportunity to highlight that, to talk about investments into families.”

ESP co-chair Natalie Foster: “Direct cash payments are the best, fastest way to put relief into people’s hands. Because rent comes every month, the bills come every month, putting food on the table happens every month, and so should the checks… It will be hard to do, but we can do hard things. And we have to do hard things.

“There are now 35 mayors across the country who have called for a federal guaranteed income, and many of them are demonstrating the idea in their cities, from St. Paul, to Columbia, SC, to Atlanta, GA.

“There is a groundswell of support for monthly checks.”

Former Stockton Mayor and MGI Founder Michael Tubbs: “There always seems to be a lot of hand wringing and heart wrenching discussion about how to help the majority of people. But just four years ago, we passed $2 trillion in tax cuts — not in the pandemic, in regular times — to the richest among us, which is even more than President Biden is proposing with his $1.9 trillion package.

“This is a question of values, a question of who we are as a country, and a question of do we want to not just recover, but do we want to build back better from where we were.”

Restaurant Owner and Change.org petition organizer Stephanie Bonin: “What people are spending the checks on is different, whether it’s diapers, or being able to make our rent, or being able to make up for reduced hours, it’s all different. But what we have in common is that we’re all trying to be survivors of COVID-19, and in doing that, we need help. And that’s what we’re calling on.”

— Mayors for a Guaranteed Income (@mayorsforagi) January 21, 2021

While everyone was coming out for the Day of Action, mayors were also speaking out for checks. Mayors for a Guaranteed Income, representing 33 mayors from cities and towns across the country, ran an ad in TIME calling for recurring checks until the end of the pandemic.

Billboard for Recurring Checks in West Virginia

Income Movement put up a billboard in West Virginia urging Democratic Sen. Joe Manchin to back $2,000 stimulus checks, garnering several local news stories and a response from Sen. Manchin indicating his openness to targeted direct checks.

More Perfect Union joined in on the local efforts, interviewing West Virginians who would be the most affected by austerity measures.

In their own words, families and workers asked Sen. Manchin to “come to the people of West Virginia, and tell our people why we don’t need this money.”

We sponsored this billboard to call out @JoeManchinWV for not supporting stimulus checks. What a great video by @MorePerfectUS to give voice to the People of West Virginia and how they feel about higher min wage & $2k Checks @JoeManchinWVpic.twitter.com/5rrhNH3BCK

— Income Movement #MakeItMonthly (@income_movement) February 4, 2021

A new report from AARP’s Public Policy Institute explores how the coronavirus pandemic has amplified chronic problems in long-term care, as nursing homes became COVID hotspots and hiring home health aides was complicated by shortages and the need to isolate. More family caregivers have stepped in to provide help for their loved ones over the past year, at significant personal financial cost, due to lost wages and spending to cover needs.

The report finds that expanding state programs that compensate family caregivers for some of the assistance they provide to their family and friends can be an important solution – during COVID and beyond – for providing caregiving needs in a cost-effective way that also meets many families’ desires to be there for their loved ones.

In the past year, 15 additional states have expanded their self-directed programs to allow hiring of family members.

Many people prefer to hire someone they know, such as a family member, friend or neighbor, and a majority (65%) of those caring for an adult have said a program under which they were paid for at least some of their caregiving hours would be helpful.

“The vast majority of older adults want to stay in their homes as they age, and allowing them to pay a friend or family member to help with their daily needs can make that possible,” says Susan Reinhard, Senior Vice President of AARP’s Public Policy Institute.

“The pandemic provided a push for states to expand this option, and we hope many of them will make their policy changes permanent. Paying family caregivers is a solution that saves states money and meets the growing need for long-term care.”

The report also looks at possible cost savings from providing more home and community-based care. According to a multi-state analysis from Public Partnerships, participants in self-directed care programs received an average monthly budget of $1,774 in 2019, compared to a monthly cost of $6,175 for a Medicaid-funded semi-private room in a nursing home. Most programs that allow family members to be paid for caregiving are operated under Medicaid, with a smaller number funded by individual states or the Veteran-Directed Care program.

This paper is the fourth in the AARP Public Policy Institute’s LTSS Choices initiative – a series of reports, blogs, videos, podcasts, and virtual events that seeks to spark ideas for immediate, intermediate, and long-term options for transforming long-term services and supports. Click here to learn more.

_____

AARP is the nation’s largest nonprofit, nonpartisan organization dedicated to empowering people 50 and older to choose how they live as they age. With a nationwide presence and nearly 38 million members, AARP strengthens communities and advocates for what matters most to families: health security, financial stability and personal fulfillment. AARP also produces the nation’s largest circulation publications: AARP The Magazine and AARP Bulletin. To learn more, visit www.aarp.org, www.aarp.org/espanol or follow @AARP, @AARPenEspanol and @AARPadvocates, @AliadosAdelante on social media. Source: AARP

In 2019, Mitt Romney became the first Senate Republican to endorse a form of child allowance, where all low- and middle-income parents would get a cash benefit to help raise their kids, regardless of whether or not they’re able to work. At the time, the plan was modest, amounting to only $1,500 a year for kids under 6 and $1,000 for kids 6-17.

But on Thursday, Romney went further and proposed the Family Security Act, one of the most generous child-benefit packages ever, regardless of political party. The plan completely overhauls the current child tax credit and turns it from a once-a-year bonus to massive income support, paid out monthly by the Social Security Administration. (The bill text isn’t final, but you can read the Romney team’s summary here.)

Romney’s plan would replace the child tax credit, currently worth up to $2,000 per child and restricted to parents with substantial income (it doesn’t fully kick in until you reach an income of over $11,000), with a flat monthly allowance paid out to all parents:

Parents of kids ages 0 to 5 would get $350 per month, or $4,200 a year

Parents of kids ages 6 to 17 would get $250 per month, or $3,000 a year

Parents with multiple kids could get a maximum of $1,250 per month or $15,000 a year; that translates to five kids between the ages of 6 and 17. Very large families would be somewhat penalized, but many families with three or four kids will get the full benefit.

Just like the current child tax credit, Romney’s proposal would phase out for wealthy parents — the benefits begin phasing out for single filers with $200,000 and joint filers with $400,000 in annual income.

But the phaseout would be implemented on the back end, through the tax code — even the richest parents would still get their $250-$350 per-kid checks in the mail every month; they’d just return the money on April 15.

That helps ensure the benefit is truly available to all eligible people and not delayed due to concerns of “overpayment.”

If you’re a liberal reading this and wondering if there’s a catch, there is — but it’s not necessarily a huge one. Romney doesn’t want his plan to add to the deficit, and he wants to simplify the set of child-related benefits the government currently offers. So his plan would pay for the child allowance by eliminating a number of other programs, including some that mostly benefit the poor (more on those below).

They estimate that poverty as they measure it would fall by nearly 14 percent across the board (lifting 5.1 million people out), and by one-third for children. The effects would be even more pronounced for extreme poverty, defined as living under half the poverty line. Some critics argue the poverty line Niskanen uses is too low, but the point remains: This plan would do an awful lot to chip away at poverty in the United States. (You can read Niskanen’s full report on the plan here.)

Poverty effects of the Mitt Romney child allowance plan.

That poverty effect, Niskanen concedes, is smaller than the effect of Joe Biden’s proposed one-year child tax credit expansion would have during that one year. But that’s only because the Romney plan curtails tax breaks and cuts spending, including getting rid of other programs for low-income people that the child allowance renders redundant.

The upside of Romney’s plan being fully paid for, however, is that it would allow Congress to make the measure permanent under budget reconciliation rules, whereas the Biden proposal that relies on deficit funding is a temporary one-year measure.

The Romney plan also has some advantages over the Biden plan as currently presented, even beyond being permanent. Checks are sent in a truly universal manner, which makes for easier monthly payments. As of this writing, the Biden administration hasn’t commented on whether or not its plan will include monthly payments, though some Democratic offices in Congress have told me on background they are pushing for monthly payments. A White House spokesperson told me, “We are working with Congress and the Treasury Department to determine the best way of getting families this relief in the American Rescue Plan.”

The Romney plan has already earned praise from surprising quarters.

Matt Bruenig, the leftist writer and founder of the People’s Policy Project think tank who writes frequently about child benefits, told me:

“Among the child benefit policies that have been proposed so far, Romney’s is the best. It has the highest benefits and the simplest administration. I’d like to see Romney get rid of his proposal’s benefit phaseout and child cap, which create hassle without meaningful savings, but otherwise it’s a pretty solid proposal.”

Sharon Parrott, president of the left-leaning Center on Budget and Policy Priorities, which pushes for expanded benefits for low-income people, was more skeptical. “This proposal shows growing bipartisan support for expanding the child tax credit, but it’s misguided to undercut the policy’s poverty-reducing impact by using deep cuts in other critical forms of support for low-income people to pay for it,” Parrott told me.

“They want to talk about it as consolidation, but they are massive cuts. Their own document shows an EITC cut of $47 billion.”

In its current form, the Romney plan may not be able to make it through Congress, for reasons Parrott highlights and detailed further below. But if the Biden administration embraces it and tweaks it, it could hit on a rare achievement: a truly bipartisan expansion of the social safety net that permanently reduces poverty in America.

The background to Romney’s proposal