Medicare is a successful and treasured government program that provides health care for seniors, for those with disabilities and for those with end-stage renal disease. The Traditional Medicare (TM) approach provides quality and necessary health care with administrative costs that are far lower than that of private health care insurance such as Medicare Advantage (MA). However, this highly valued public program is now at risk of being turned into just another cash cow for Wall Street investors and the private health insurance industry at the public’s expense.

The CMMI

How is this happening? Well, the 2010 Affordable Care Act established the Center for Medicare and Medicaid Innovation (CMMI). This Center’s goal was identifying “ways to improve healthcare quality and reduce costs in the Medicare, Medicaid, and Children’s Health Insurance Program (CHIP) programs.”

Importantly, this Innovation Center was granted the authority to test alternative payment and service delivery models on a national scale without congressional approval. Being able to avoid Congressional politics makes sense as long as there is assurance that these public programs won’t be undercut.

CMMI’s record

Initially the CMMI focused on relatively small pilot projects. In a December 2021 article, Ryan Grim of The Intercept addressed the CMMI and its projects. Grim quoted from a February 2021 article by Brad Smith, who became the CMMI director in January 2020. Smith wrote: “the vast majority of the Center’s models have not saved money, with several on pace to lose billions of dollars. Similarly, the majority of models do not show significant improvements in quality.” Smith identified “inflated benchmarks” — in which providers wildly overestimate what they expect a patient will cost — and providers’ ability to “game” the payment models as key drivers of losses for the government. Smith’s concern about inflated benchmarks and gaming the system likely also apply to the private MA plans that cost more than the TM approach.

Direct Contracting

Former President Trump’s appointees to lead the CMMI greatly extended the scope of the pilot project idea and focused on a direct contracting entities (DCEs) model. According to Physicians for a National Health Program (PNHP), these DCEs are essentially third-party middlemen that receive a capitated monthly payment from the Centers for Medicare & Medicaid Services (CMS) for covering some defined portion of each enrollees’ medical expenses — and may keep what they don’t pay for in care. PNHP added: “Virtually any company can apply to be a DCE, including investor-backed startups that include primary care physicians, [Medicare Advantage] plans and other commercial insurers, accountable care organizations (ACOs) or ACO-like organizations, and for-profit hospital systems.”

This profit-based incentive model could threaten the health of enrollees as well as quickly lead to the privatization of this vitally important public program. This privatization has been a long-held dream of many conservative ideologues as well as Wall Street.

The Biden Administration and DCEs

I had hoped that President Biden’s administration would have stopped the implementation of the DCE models. However, according to PNHP, the CMS Innovation Center’s chief strategy officer said in late October 2021 that the agency “envisions a future where every Medicare beneficiary and most Medicaid beneficiaries are in an accountable care relationship by 2030,” signaling their intention to rapidly expand the DCE program to cover all TM beneficiaries in the next 8 years. Note that this change would likely be without the understanding or consent of TM beneficiaries. However, the Biden administration did delay the worst type of the proposed DCE models, but two other types are going forward.

PNHP added: “Currently, the pilot involves 53 DCEs in 38 states, D.C., and Puerto Rico, covering 30 million of the 36 million TM beneficiaries. … A majority of DCEs (28 of 53 total) are controlled by investors — not providers — and most have ties to MA commercial insurers.” This is hardly a pilot project.

What you can do

PNHP asks that you call your member of Congress at (202) 224-3121 and request that they demand Health and Human Services end this Medicare DCE program; hold hearings on DCEs; establish Congressional oversight of the Center for Medicare and Medicaid Innovation; and sign its petition at pnhp.org.

As the Federal Reserve signals it will raise interest rates in March, we talk to Christopher Leonard, author of the new book The Lords of Easy Money, about how the Federal Reserve broke the American economy. He details the issues with quantitative easing, a radical intervention instituted by the federal government in 2010 to encourage banks and investors to lend more risky debt to combat the recession. “The Fed’s policies over the last decades have stoked the world of Wall Street,” says Leonard. “It has pumped trillions of dollars into the banking system and thereby inflated these markets for stocks, for bonds. And that drives income inequality.”

TRANSCRIPT

This is a rush transcript. Copy may not be in its final form.

AMYGOODMAN: This is Democracy Now! I’m Amy Goodman, with Nermeen Shaikh.

Amidst growing concerns about inflation in the U.S., the Federal Reserve announced Tuesday it will start hiking interest rates in March. To look at what this will mean for working people and everyone beyond the 1%, we’re joined by Christopher Leonard, longtime business reporter. His new book is out this week, The Lords of Easy Money: How the Federal Reserve Broke the American Economy.

Welcome to Democracy Now! It’s great to have you with us, Christopher. If you can start off with a Federal Reserve 101: What does it mean to lift interest rates? And why do you say it’s broken, the American economy?

CHRISTOPHERLEONARD: Yes. Thank you. Great question. And, you know, the Federal Reserve can seem like this very kind of obscure and highly technical institution that only matters to Wall Street, but I really think that’s not the case. It is critical to understand what this central bank does and how it has affected our economy. You know, one of my central preoccupations as a business reporter is trying to understand growing income inequality in the United States and why we live in this sort of funhouse-type economy where we can see stock markets breaking records, corporate debt markets breaking records, while the middle class is really treading water with stagnant wages and falling further behind. What the Federal Reserve has done over the last decade helps explain why this is happening.

So, you know, at the root level, we created the Federal Reserve as the central bank to do one key thing: It creates our currency. The Federal Reserve literally creates and manages our currency. That thing we call a U.S. dollar is in reality a Federal Reserve note. So, the central bank’s job is to make sure that the dollar retains its value. So that’s why you always hear this talk about, you know, the Federal Reserve hiked interest rates today, or it cut interest rates today. What they’re doing is expanding or contracting the supply of money.

So, why does that matter? Well, here’s why. Over the last decade, the Fed has really moved itself to the center of American economic life. The Fed has engaged in an unprecedented series of experiments in printing new money. Let me put it this way: In the first century of its existence, the Fed expanded the pool of base money — you know, what the economists called the monetary base. The Fed expanded that pool of money to about $900 billion. So, that’s a trillion dollars in printing money over a century. But then, after the crash of ’08, between 2008, 2014, the Fed prints $3.5 trillion. So that’s three-and-a-half centuries’ worth of money printing in a few short years.

Now, that money is not a neutral force. When the Fed creates new dollars, it doesn’t create them in the checking account of normal people, right? It creates new dollars — specifically and by design, it creates new dollars on Wall Street in the bank accounts of 24 select institutions. And they’re the folks you’d suspect: you know, JPMorgan, Goldman Sachs, Wells Fargo. That’s where the Fed is creating these new dollars. So the Fed’s policies over the last decades have stoked the world of Wall Street. It has pumped trillions of dollars into the banking system, and thereby it’s inflated these markets for stocks, for bonds. And that drives income inequality, because, you know, just the tiny 1% at the top of our wealth ladder controls 40% of all the assets, whereas the bottom half of Americans, you know, those of us who earn a living by getting a paycheck rather than by owning assets — the bottom half of Americans only own about 5% of all the assets. So the Fed’s policies have enriched the very rich, the biggest of the big banks, while leaving the middle class behind.

And now we find ourself in this position, that’s really actually quite a dangerous moment, in 2022, where we’re seeing price inflation start to increase dramatically. So, the Fed is being forced to tighten the money supply and to try to back off these stimulus programs it’s created. The real risk here, I think, for everybody in America is that as the Fed does this, as it hikes rates and pulls back on the stimulus, it’s going to cause those asset markets to fall. And, you know, to put that in common parlance, it’s risking creating a financial market crash as the Fed is forced to hike interest rates. And again, to me, one of the key problems with this is that over the decade of these easy money policies, the middle class has really been left out. And once again, it will be the middle class that’s going to have to pay the bill if we see another financial market crash.

NERMEENSHAIKH: Well, Chris, could you respond to what we see everywhere in the media, namely that inflation rates now are almost at 7%, higher than they’ve been since the 1980s? I mean, that level of inflation also impacts the vast majority of Americans adversely. What other steps could be taken to reduce inflation?

CHRISTOPHERLEONARD: So, it’s just fascinating. And one key thing I would really like to point out, that I learned while reporting this book, is that we should, I think, think about two kinds of inflation. There’s inflation of prices, which is what we’re talking about right now, that really sharp increase in the price of food, fuel, television sets, cars. That’s price inflation. But then you’ve got inflation of assets, which is what the Fed has been pushing so hard for decades. So, that’s a rise in the value of homes and stocks and corporate bonds. So we’ve actually had runaway asset inflation for a decade, but we haven’t seen price inflation. And we’re starting to see it now.

And as you point out, price inflation can just, frankly, be devastating for the middle class, if wages don’t keep up with the increase in prices — which, unfortunately, is exactly what we’re seeing now. So, wages are kind of creeping up a little bit, but we’re seeing this runaway increase in prices, which presents us with a terrible dilemma. And to be blunt, the Federal Reserve is responsible for the price inflation, at least to a certain degree, by pumping all of this money into the economy.

So, you know, your question is: How can you fight it, and what can you do?

AMYGOODMAN: We have 30 seconds.

CHRISTOPHERLEONARD: Quite unfortunately, one of the few ways to do this is to hike interest rates, which is going to create damage to our economy. Many other important measures will take a lot of time, such as improving the supply chain or cracking down on monopolies. So, we’re going to see interest rates hiked, and it’s going to be a bumpy ride.

AMYGOODMAN: Well, we clearly have to come back to this conversation, Christopher Leonard, business reporter and author. New book out this week, it’s called The Lords of Easy Money: How the Federal Reserve Broke the American Economy.

And that does it for our show. I’m Amy Goodman, with Nermeen Shaikh. Remember, wearing a mask is an act of love.

In the lead-up to recent climate talks in Glasgow, Scotland, some were calling COP26 the “Finance COP.” This was, in part, because Mark Carney, the former governor of the Bank of England, had been working tirelessly to secure new climate commitments from financial institutions across the globe.

Carney finally had his big moment in Glasgow when he announced that over 450 of the world’s largest financial institutions — including banks, insurers, pension funds and asset managers — had joined theGlasgow Financial Alliance for Net Zero (GFANZ) and committed to achieving net zero emissions by 2050. “The architecture of the global financial system has been transformed to deliver net zero,”stated Carney as he unveiled the news.

There were, however, two key words missing from the financial sector’s big moment. Not once in the 1,349-wordpress release proclaiming the financial industry’s new-found dedication to climate action did the words “fossil fuels” appear. To say that this is problematic is an understatement.

One study calculated that 71 percent of all of history’s greenhouse gas emissions come from just 100 fossil fuel companies. Not only that, but fossil fuel corporations have spent 40 yearsfunding climate denial andwaging war against even incremental proposals for climate action.

To tackle the climate crisis without confronting fossil fuels is like trying to put out a fire without doing anything to stop the people pouring gasoline on the flames. But that appears to be the approach that the financial sector is taking. Nowhere is this more obvious than on Wall Street.

In the five years after the Paris Agreement was signed in 2015, just six U.S. banks — JPMorgan Chase, Citigroup, Wells Fargo, Bank of America, Morgan Stanley and Goldman Sachs — have loaned a little shy of$1.2 trillion to the fossil fuel industry. To give that some context, consider that $1.2 trillion is more than double the current share market value of ExxonMobil, Chevron and BP combined.

In spite of their deep ties with the fossil fuel industry, every major U.S. bank has signed on to the Glasgow Financial Alliance for Net Zero and committed to achieving net zero emissions by 2050. Yet none of them have committed to ending their support of the industries that are most driving the climate crisis. Indeed, they seem intent on doing the opposite. Goldman Sachs CEO David Solomon recentlyvowed to continue providing finance to the oil and gas industry; Chase CEO Jamie Dimon has expressedsimilar sentiments.

A few months before the start of COP26, JPMorgan Chase, the world’s largest funder of fossil fuels, became the first major U.S. bank to set 2030 climate targets. Unfortunately, rather than actually reducing the overall greenhouse gas emissions associated with its lending, Chase chose to reusea convoluted accounting trick often used by Big Oil known as “carbon intensity,” pledging that by 2030, it will achieve a 15 percent reduction in the “carbon intensity” of the oil and gas firms it finances.

Here’s how Chase’s carbon intensity commitments work: Imagine you are the CEO of an oil firm. Your company owns 1,000 oil wells. You receive a $10 billion loan from Chase. You use that loan to buy 400 additional oil wells and 400 windmills. This means you are digging up and burning more oil than ever before; your overall contributions to climate change have gone up significantly. But because you are now also profiting from wind power, the “carbon intensity” of your company has gone down — an accounting trick that allows your oil company to expand oil production and banks like Chase to meet their greenwashed climate targets.

During COP26, Morgan Stanley became the second U.S. bank to release 2030 climate targets,announcing a plan to slash emissions in the energy, auto and manufacturing sectors. Unfortunately, Morgan Stanley’s targets are only a half-step better than Chase’s.

Thepress release announcing Morgan Stanley’s 2030 targets claims that the company’s targets are based on the International Energy Agency’s (IEA)Net Zero by 2050 pathway. However, a key part of the IEA’s recommendations was that “there is no need for investment in new fossil fuel supply in our net zero pathway.” Unsurprisingly, a promise from Morgan Stanley, the world’s largest funder of new LNG terminals, to immediately end support for the expansion of the oil and gas industry was not forthcoming.

Given the collective failures of Carney, Chase and Morgan Stanley, it’s understandable that many activists denounced COP26 as nothing more than a “greenwashing festival.” This failure also makes it clear that we need the federal government to regulate financial institutions that are unwilling to do what’s necessary to curtail catastrophic climate change.

There have been some small first steps toward reigning in Wall Street’s ability to wreck our climate. In May 2021, President Biden issued the first-ever Executive Order on Climate-Related Financial Risk, directing federal regulators to analyze and mitigate the risk that climate change poses to the economy.

In response, the Financial Stability Oversight Council (FSOC), the federal government’s most powerful financial regulator, released a report outlining what the climate crisis should mean for the financial sector. Unfortunately, although FSOC affirmed that U.S. financial regulators do, in fact, have the authority and obligation to address the climate crisis, it failed in several key regards. Most importantly, the report didn’t even mention that U.S. banks are actively driving the climate crisis by financing the continued expansion of the fossil fuel industry.

Of greater hope is the Fossil Free Finance Act. Introduced by Representatives Mondaire Jones, Rashida Tlaib and Ayanna Pressley last fall, the Fossil Free Finance Act would prohibit the funding of new fossil fuel projects by 2022 and the funding of all fossil fuel projects by 2030. It is legislation that meets the scale and urgency of the climate challenge — which is, of course, exactly what is required.

Yet so far, only 22 Members of Congress have signed on to co-sponsor the Fossil Free Finance Act. If our elected officials are at all serious about addressing the climate crisis, that number must grow dramatically in 2022.

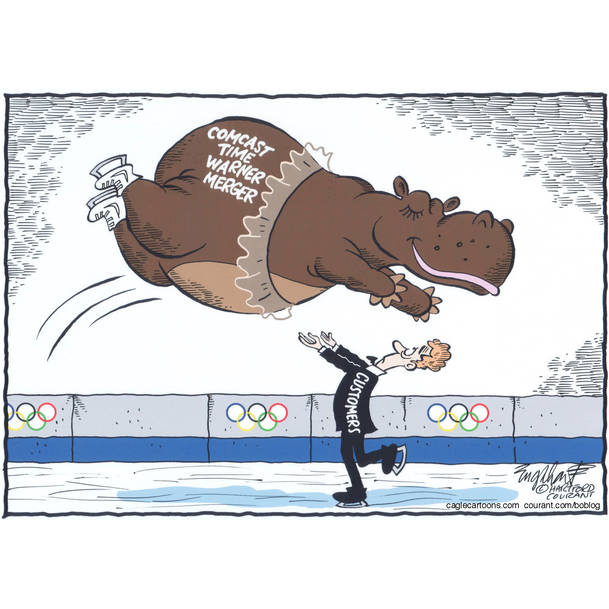

In the face of massive support for Medicare for All and the failure of the U.S.’s for-profit health care system, the inevitable fall of the medical-industrial complex can be predicted, if not with precision, with certainty. Everyone is aware of the impending demise, none more so than those in charge of the for-profit health care system and their supporters in Congress, as evidenced by the frenetic activity at the Centers for Medicare and Medicaid Services (CMS) to transfer the traditional Medicare program to the insurance industry as fast as humanly possible. Given this urgency, physicians representing Physicians for a National Health Program delivered a petition signed by 13,000 individuals, including 1,500 physicians, to Health and Human Services Secretary Xavier Becerra this week demanding the end to the privatization of Medicare.

Privatization, the transfer of a public good to private, for-profit entities, is already true for over 40 percent of Medicare in the form of Medicare Advantage, private insurance plans that have been persistently and pervasively overpaid by Medicare for decades. As Kip Sullivan recently described in “Single Payer Health Care Financing,” this fraud has been going on for decades.

In 1995, the U.S. General Accounting Office (GAO) warned Congress that Medicare was overpaying Health Maintenance Organizations (HMOs), the precursors to Medicare Advantage plans, by 6 to 28 percent compared to what it would have paid had all those HMO enrollees remained in traditional Medicare because most HMOs benefited from “favorable selection,” meaning, healthier patients enrolled in HMOs. In 1999, the GAO again warned Congress that Medicare spent more on beneficiaries enrolled in HMOs than it would have had those beneficiaries been enrolled in traditional Medicare. The following year, the GAO told Congress that it was largely excess Medicare payments to HMOs, not their efficiencies, that allowed plans to attract large numbers of beneficiaries, again exceeding costs expected under the traditional program, adding billions to Medicare spending.

Twenty-six years later, in its 2021 report to Congress, the Medicare Payment Advisory Commission wrote, “The Commission estimates that Medicare currently spends 4 percent more for beneficiaries enrolled in MA [Medicare Advantage] than it spends for similar enrollees in traditional fee-for-service (FFS) Medicare.” This low number is difficult to square with the profit that insurance companies are making and the extra benefits that they offer. What has been clear to Congress for decades, is that Medicare Advantage, which inserts a middleman to “manage” care between CMS and doctors and hospitals, costs more than traditional Medicare, which does not require a middleman between the senior and the provider. From 1972 to 2004, overpayment by Medicare to HMOs was the rule and due mostly to favorable selection. After 2004, overpayment persisted for Medicare Advantage plans (formerly known as Medicare + Choice) for two reasons: favorable selection (“cherry picking,” or selecting healthy patients, as well as “lemon dropping,” or getting rid of sick patients, perfected by HMOs) and upcoding.

What is upcoding? When a doctor bills the insurance company or Medicare for a patient, the doctor uses a diagnosis code. For example, a patient who is seen for pneumonia will be billed with the diagnosis code for pneumonia. But what if instead of just billing for pneumonia, the physician also coded for shortness of breath, hypoxia (low oxygen level), productive cough and exposure to tuberculosis, some of which might or might not be accurate, but could certainly be present in someone with pneumonia? This would be upcoding and would be considered fraud, but in the Medicare Advantage world, upcoding is known as risk-score gaming, and it is perfectly legal.

Risk-score gaming is how Medicare Advantage has been drawing serious overpayments since its full implementation in 2006. Medicare Advantage does this by submitting diagnosis codes that create more CMS Hierarchical Condition Categories (HCCs) for each patient. For example, a 76-year-old female with obesity, type 2 diabetes, major depression and congestive heart failure has an HCC risk score of 1.03. For this patient, CMS pays a Medicare Advantage plan that does not upcode $9,000.

If however, the Medicare Advantage plan upcodes — same patient, same medical conditions but more codes: morbid obesity instead of obesity, diabetes with retinopathy instead of diabetes; a mild, single episode of major depression instead of unspecified major depression; chronic obstructive lung disease instead of asthma and a stage 3 ulcer instead of ulcer — her risk score jumps to 3.63, and CMS pays the Medicare Advantage plan for the same patient $32,000. The plan reaps obscene profits, some of which goes to marketing, some of which goes to improve benefits driving up the number of new members, but most of which go back into profits, all the while draining the Medicare trust fund, driving up Part B premiums (monthly payments made by beneficiaries to Medicare) and diverting taxpayer funds from other social services.

For each 0.1 increase in risk score at current enrollment levels, there are $15 billion in overpayments ($13 billion from CMS, and $2 billion from Part B beneficiaries) and the Medicare Advantage plan takes $3.5 billion in profits. Risk-score gaming is the business model for Medicare Advantage and creates a major transfer of wealth to Medicare Advantage from taxpayers and traditional Medicare recipients.

All evidence points against using the multibillion-dollar health insurance industry to improve outcomes and save money. But evidence is no match for profit. In 2019, the Medicare budget approached $800 billion, and by 2026, it is projected to be $1.35 trillion. This amount of taxpayer money keeps capitalists up at night, especially the medical-industrial complex types, scheming up ways to grab some for themselves. Lucky for these capitalists, CMS is continuing its march towards privatization, or what is known in the parlance of health economists, “de-risking” all of Medicare, meaning eliminating the risk of providing health insurance to seniors by having someone else bear the risk. But the truth is the exact opposite: These overpayments are allowing the insurance industry to pretend they bear risk when in fact it’s the taxpayer who is bearing risk.

There is much profit to be gained by “bearing the risk” for Medicare through favorable selection and upcoding, as evidenced by the outsized profits for insurers in Medicare Advantage compared to margins in the group or individual market. There should be little surprise, then, that the industry is chomping at the bit to “bear the risk,” that is, be overpaid to insure the remaining 60 percent of seniors who have deliberately chosen not to enroll in Medicare Advantage, those that are safely (or so they thought) enrolled in traditional Medicare.

But safe they are not, and every enrollee in traditional Medicare should take note: A program known as the Global and Professional Direct Contracting model in a little-known government agency known as the Center for Medicare and Medicaid Innovation (“The Innovation Center”) is already moving them, without their knowledge or consent, to “risk-bearing,” for-profit middlemen known as Direct Contracting Entities (DCEs). The goal: to end what’s left of traditional Medicare.

The Innovation Center was created under the Affordable Care Act (ACA) in 2010 with a mandate to test “innovative” payment and service delivery models for Medicare that would decrease costs, and if not improve, at least not worsen care. The ACA gave full authority to the Innovation Center to scale up any model it deemed fit, to all of Medicare without congressional approval. In the past 10 years, 54 models have been developed, 50 of which failed and all of which continue to use market-driven models of care. Not one model has been developed to test out single-payer, which actually would decrease costs and save lives. The latest demonstration project, created in the waning days of the Trump administration and greenlighted by the Biden administration, is the DCE model, which is being rolled out to traditional, fee-for-service Medicare beneficiaries without congressional approval or anyone’s vote.

What is a Direct Contracting Entity? Simply put, it is a “risk-bearing,” for-profit middleman to manage health care for traditional Medicare beneficiaries, just like Medicare Advantage plans are for seniors who have signed up for Medicare Advantage plans. The difference is that while 26 million seniors have voluntarily signed up for a middleman when they chose Medicare Advantage, the 38 million seniors in traditional Medicare have not.

How do you get seniors who have specifically chosen traditional Medicare to switch to a non-traditional Medicare-Advantage-like plan with a mysterious name like “Direct Contracting Entity”? You don’t tell them! You lure their primary care providers to participate in a DCE by promising the doctors much better Medicare reimbursement rates and more time with their patients, and once the doctors sign up with a DCE, all their patients are automatically “aligned” by CMS with the DCE the doctor has chosen. The DCE sends patients a letter they are likely not going to read or understand, and presto! Millions of seniors previously on traditional Medicare now belong to a DCE. That’s how DCEs leverage and monetize the doctor-patient relationship for the profit of corporations.

DCE middlemen accept capitated payments for seniors in traditional Medicare just like Medicare Advantage plans, “cherry pick and lemon drop,” deny care, upcode, spend as little as 60 percent on health care for beneficiaries (compared to Medicare Advantage’s 85 percent), and keep the rest as profit. The playbook is an old one, and it works.

There are 53 DCEs in 38 states and Washington, D.C., mostly owned by for-profit, private equity firms, investor-owned primary care practices, Accountable Care Organizations(a network of doctors and hospitals that is jointly accountable for the health of a group of Medicare patients and that receives financial incentives from Medicare to save money on patient care while meeting certain quality metrics) and Medicare Advantage plans. Many DCEs are owned by publicly traded corporations straight out of Wall Street. These are the corporations that will potentially manage the care of up to 30 million seniors who thought they were free of insurance companies. Instead, their health will be weighed against profit. And in a market-driven, for-profit health care system, the bottom line always wins.

But the most important question still remains: Why the urgency to “de-risk” (privatize) Medicare, no matter the cost? Enter Liz Fowler, architect behind the ACA, an industry darling who ensured health insurance companies would reap billions every year under the ACA, the new director of the Innovation Center brought in by the Biden administration to oversee the full privatization of Medicare. Industry giants and Washington insiders can read the writing on the wall as well as anyone else. They are acutely aware that a majority of Americans say it is the government’s responsibility to provide health care for all. They know that a pandemic has shined a light on the inefficiencies, inequities and indifference of our health care system. They know that Americans died in greater numbers and at increased rates compared to countries with universal health care systems in place. In the face of this inevitability, what would the medical-industrial complex and Congress do? Sell off Medicare, and fast, before Americans actually get Medicare for All.

Health and Human Services Secretary Becerra, a supporter of Medicare for All, and CMS Administrator Chiquita Brooks-Lasure have the authority to terminate the Direct Contracting model program. Congress has the power to hold hearings on the Innovation Center and pass legislation to provide congressional oversight to the Center’s pilot programs. The Innovation Center has put a hold on new DCE applications, to the consternation of industry, but all signs point to the continuation of using DCEs to privatize traditional Medicare. The Innovation Center will put a pretty bow around DCEs and talk about “equitable outcomes” and “person-centered care” but we should not be fooled: The end of Medicare is near. It is up to us to demand DCEs, not Medicare, be ended.

On Monday, the White House announced that President Joe Biden is planning to nominate Republican Jerome Powell for his second term as chair of the Federal Reserve, one of the most influential positions in Washington.

Alongside Powell, Biden will nominate Lael Brainard as vice chair. Brainard is the only Democrat on the seven-person Fed board and was previously being considered by the White House as a leading candidate to replace Powell.

The two appointments will then go to the Senate, where progressive lawmakers will likely put up a fight against Powell’s nomination — particularly Sen. Elizabeth Warren (D-Massachusetts), who has called Powell a “dangerous man” due to his record over his first four-year tenure.

Since Powell’s original nomination by Donald Trump, he has been panned by progressive advocates and lawmakers for not being strict enough when it comes to regulating banks and Wall Street. He has also been criticized for his ignorance on climate issues.

In a statement announcing the nomination, the White House noted the administration’s belief that it is important to have steady leadership at the Fed as the pandemic continues.

“Fundamentally, if we want to continue to build on the economic success of this year we need stability and independence at the Federal Reserve — and I have full confidence after their trial by fire over the last 20 months that Chair Powell and Dr. Brainard will provide the strong leadership our country needs,” said Biden. There are three remaining nominations to the Fed board that the president has yet to announce.

Biden bucked progressive recommendations in nominating Powell for a second term, perhaps as an attempt to appeal to bipartisanship. That appeal may have serious consequences, as economics experts have warned that Powell’s record is alarming during an unstable time for the U.S. economy.

“[A] Powell renomination raises serious concerns simply based on his record,” Gerald Epstein wrote for Truthout in September. While Powell has rightly earned praise for his support of maximum employment and his handling of economic turmoil during the early months of the pandemic, Epstein wrote, “supporters who focus only on these areas are ignoring another crucial component of the Fed’s job — financial regulation and financial stability — where Powell has a much more problematic record.”

As Fed chair, Powell rolled back financial regulations that were put in place after the Great Recession, including Dodd-Frank, legislation that was implemented to prevent predatory mortgage lending and to curb the excessive risk-taking that led to the crisis. Many of the moves Powell made early in the pandemic were only necessary because of existing weaknesses in the financial system, Epstein noted.

The Fed has been embroiled in several scandals during Powell’s tenure — one including Powell himself. Last year, just before the stock market crashed in October, Powell sold between $1 million and $5 million in stock. Vice Chair Richard Clarida made a similar stock transaction in February of 2020, just before new pandemic policy changes were announced.

Wall Street investors have hit the jackpot. Soon they’ll be able to buy, own, and dictate The Commons, public lands, the world of Mother Nature. In fact, a pilot project is already in the works with ecosystems up for sale as Wall-Streeters anxiously prepare to gobble up the valued benefits of Mother Nature.

According to the NYSE PR Dept. they’ll IPO nature: “To preserve and restore the natural assets that ultimately underpin the ability for there to be life on Earth.” What? Really?

And, according to NYSE COO Michael Blaugrund: “Our hope is that owning a natural asset company is going to be a way that an increasingly broad range of investors have the ability to invest in something that’s intrinsically valuable, but, up to this point, was really excluded from the financial markets.”

Then, does this mean that neoliberal capitalism is becoming nature’s beneficent caretaker so environmentalists can stop wringing their hands about the horrendous loss of wild vertebrate life, down a whopping 68%, and loss of wetlands and loss of huge chunks of rainforests these past few decades, all of which echoes a guttural sound of impending extinction? Answer: Don’t count on it.

For starters, there’s something extraordinarily distasteful and downright disgusting about Wall Street buying control of nature’s resource capabilities. It bespeaks of an upside down world where the ludicrous becomes acceptable, but is it really acceptable? Is it?

The main character in this new scheme to own the world is a new asset class with a very plain name that says it all: Natural Asset Company or NAC. Yes, if you are a billionaire, get ready to buy up to 30% of the world’s natural resource beneficence to society. It’s going to be offered on the biggest auction block of the world, the New York Stock Exchange under the cover of sustainability of nature and protection of biodiversity, wink, wink!

Of course, this prompts a series of questions, headlined by when does Mother Nature morph into a tollbooth?

In simplest of terms, NACs allow for the formation of specialized corporations the hold the rights to the ecosystem services produced on a given chunk of land. The services might be sequestration of carbon or clean water or possibly rare Tibetan mountain air or maybe a lake teeming with trout in the wilderness. The possibilities are endless when auctioning off major chunks of an asset as big as the planet.

The NAC will maintain, manage and grow the natural asset that it has commoditized, working towards maximizing the profit potential of the natural asset, although, of course, this is not emphasized in the PR material. Nevertheless, it could lead to near-infinite profits. After all, the living Earth does rejuvenate and replenish and service ecosystems on its own accord, a natural process that goes on forever. Why not own it?

If ever there has been a time for the people of the world to drop whatever they are doing and focus on one issue, now is that time. The Commons is for sale! Think long and hard about that proposition, study it, discuss it, and decide whether to agree that Mother Nature should be monetized. If not in agreement, then do something, tell everybody, tell anybody who’ll listen, carry poster boards in the street, join a protest march, bang pots and pans, do something to relieve that breakneck pressure building around your temples!

The Intrinsic Exchange Group, in partnership with the NYSE, is currently working with the Costa Rica government on a pilot project of NACs in the country in order to institute its protocol for ownership of forests, lakes, waterfalls, mountains, meadows, caves, wetlands, in essence, all of nature. Costa Rica is the proving grounds for ownership of Mother Nature, whether she likes it or not.

First, NAC identifies a natural asset, like a forest, for example, which is quantified using special protocols that have already been developed by various coalitions amongst multinational corporations, which in and of itself is remarkably terrifying. The NAC decides who has the rights to the natural asset’s productivity and how it is to be managed. It is then monetized via an IPO on the stock exchange. Thus, the NAC becomes “the Issuer” to potential buyers of the natural asset that the NAC represents. Essentially, NAC is a real estate agent of Mother Nature. The buyers are institutional investors, or the occasional billionaire, that want to own the rights to the benefits of wetlands or rainforests or natural water springs or rarified mountainous air or hot springs or whatever they want to own. The world is their oyster to buy, own, enjoy, and profit by.

Throughout all human history nature has been The Commons or the cultural and natural resource for all of society inclusive of natural processes like air and water. But now private investors are deleting The Commons with claims of “conservation and sustainability” of 30% of what’s called “protected areas” of our precious worldwide assets.

According to initial calculations, NACs will unlock $4Quadrillion in assets as a new feeding ground for Wall Street investors to buy the rights to clean water and clean air and trout streams and bass-laden lakes and gorgeous picturesque waterfalls and lagoons, an entire forest, or maybe eventually extend into the oceans. Who knows the range of possibilities once nature is transacted on Wall Street.

Monetizing nature!

What’s next, what’s left?

The Commons is property shared by all, inclusive of natural products like air, water, and a habitable planet, forests, fisheries, groundwater, wetlands, pastures, the atmosphere, the high seas, Antarctica, outer space, caves, all part of ecosystems of the planet.

The sad truth is Mother Nature, Inc. will lead to extinction of The Commons, as an institution, in the biggest heist of all time. Surely, private ownership of nature is unseemly and certainly begs a much bigger relevant question that goes to the heart of the matter, to wit: Should nature’s ecosystems, which benefit society at large, be monetized for the direct benefit of the few?

Just in time for the UN’s policy push for “30 x 30” – 30% of the earth to be “conserved” by 2030 – a new Wall Street asset class puts up for sale the processes underpinning all life.

A month before the 2021 United Nations Climate Change Conference (known as COP26) kicked off in Scotland, a new asset class was launched by the New York Stock Exchange that will “open up a new feeding ground for predatory Wall Street banks and financial institutions that will allow them to dominate not just the human economy, but the entire natural world.” So writes Whitney Webb in an article titled “Wall Street’s Takeover of Nature Advances with Launch of New Asset Class”:

Called a natural asset company, or NAC, the vehicle will allow for the formation of specialized corporations “that hold the rights to the ecosystem services produced on a given chunk of land, services like carbon sequestration or clean water.” These NACs will then maintain, manage and grow the natural assets they commodify, with the end goal of maximizing the aspects of that natural asset that are deemed by the company to be profitable.

The vehicle is allegedly designed to preserve and restore Nature’s assets; but when Wall Street gets involved, profit and exploitation are not far behind. Webb writes:

[E]ven the creators of NACs admit that the ultimate goal is to extract near-infinite profits from the natural processes they seek to quantify and then monetize….

Framed with the lofty talk of “sustainability” and “conservation”, media reports on the move in outlets like Fortune couldn’t avoid noting that NACs open the doors to “a new form of sustainable investment” which “has enthralled the likes of BlackRock CEO Larry Fink over the past several years even though there remain big, unanswered questions about it.”

BlackRock is the world’s largest asset manager, with nearly $9.5 trillion under management. That is more than the gross domestic product of every country in the world except the U.S. and China. BlackRock also runs a massive technology platform that oversees at least $21.6 trillion in assets. It and two other megalithic asset managers, State Street and Vanguard (BlackRock’s largest shareholder), already effectively own much of the world. Adding “natural asset companies” to their portfolios could make them owners of the foundations of all life.

A $4 Quadrillion Asset — The Earth Itself

Partnering with the New York Stock Exchange team launching the NAC is the Intrinsic Exchange Group (IEG), major investors in which are the Rockefeller Foundation and the Inter-American Development Bank, notorious for imposing neo-colonialist agendas through debt entrapment. According to IEG’s website:

We are pioneering a new asset class based on natural assets and the mechanism to convert them to financial capital. These assets are essential, making life on Earth possible and enjoyable. They include biological systems that provide clean air, water, foods, medicines, a stable climate, human health and societal potential.

The potential of this asset class is immense. Nature’s economy is larger than our current industrial economy ….

The immense potential of “Nature’s Economy” is estimated by IEG at $4,000 trillion ($4 quadrillion).

Webb cites researcher and journalist Cory Morningstar, who maintains that one of the aims of creating “Nature’s Economy” and packaging it via NACs is to drastically advance massive land grab efforts made by Wall Street and the oligarch class in recent years, including those made by Wall Street firms and billionaires like Bill Gates during the COVID crisis. The land grabs facilitated through the development of NACs, however, will largely target indigenous communities in the developing world. Morningstar observes:

The public launch of NACs strategically preceded the fifteenth meeting of the Conference of the Parties to the Convention on Biological Diversity, the biggest biodiversity conference in a decade. Under the pretext of turning 30% of the globe into “protected areas”, the largest global land grab in history is underway. Built on a foundation of white supremacy, this proposal will displace hundreds of millions, furthering the ongoing genocide of Indigenous peoples.

The UN’s “30 x 30”

The land grab of which Morningstar speaks is embodied in a draft agreement called the “Post-2020 Global Biodiversity Framework,” currently being negotiated among the 186 governments that are signatories to the Convention for Biological Diversity. Part I of its 15th meeting (COP15) closed on October 15, just ahead of COP26 (the 26th UN Climate Change Conference of the Parties) hosted in Glasgow from October 31 through November 12. COP26 focuses on climate change, while COP 15 focuses on preserving diversity. Part II of COP15 will be held in 2022. The draft text for the COP 15 nature pact includes a core pledge to protect at least 30% of the planet’s land and oceans by 2030.

In September 2020, 128 environmental and human rights NGOs and experts warned that the 30 x 30 plan could result in severe human rights violations and irreversible social harm for some of the world’s poorest people. Based on figures from a paper published in the academic journal Nature, they argued that the new target could displace or dispossess as many as 300 million people. Stephen Corry of Survival International contended:

The call to make 30% of the globe into “Protected Areas” is really a colossal land grab as big as Europe’s colonial era, and it’ll bring as much suffering and death. Let’s not be fooled by the hype from the conservation NGOs and their UN and government funders. This has nothing to do with climate change, protecting biodiversity or avoiding pandemics – in fact it’s more likely to make all of them worse. It’s really all about money, land and resource control, and an all out assault on human diversity. This planned dispossession of hundreds of millions of people risks eradicating human diversity and self-sufficiency – the real keys to our being able to slow climate change and protect biodiversity.

How that is to be done is not clearly specified, but proponents insist it is not a “land grab.” Critics, however, contend there is no other way to pull it off. Only about 12% of land and water in the U.S. is now considered to be “in conservation,” including wilderness lands, national parks, national wildlife refuges, state parks, national monuments, and private lands with permanent conservation easements (contracts to surrender a portion of property rights to a land trust or the federal government). According to environmental expert Dr. Bonner Cohen, raising that figure to 30%, adding 600 million acres to the total, “means putting this land and water (mostly land) off limits to any productive use in perpetuity. To accomplish this goal, the federal government will have to buy up – through eminent domain or other pressures on landowners making them ‘willing sellers’ of their property – millions of acres of private land.”

This requires restricting a land area the size of the State of Nebraska every year, each year, for the next nine years, or in other words a landmass twice the size of Texas by 2030.

This goal is especially radical given that the President has no constitutional authority to take action to conserve 30% of the land and water.

The Real Threat to Mother Nature

The federal government may have no constitutional authority to take the land, but a megalithic private firm such as BlackRock could do it simply by making farmers and local residents an offer they can’t refuse. This ploy has already been demonstrated in the housing market.

According to a survey reported in The Guardian on October 12, 2021, nearly 40% of U.S. households are facing serious financial problems, including struggling to afford medical care and food; and 30% of lower income households (those earning under $50,000 per year) said they had lost all their savings during the coronavirus pandemic. In the first quarter of 2021, 15% of U.S. home sales went to large corporate investors including BlackRock, which beat out families in search of homes just by offering substantially more than the asking price. Sometimes whole neighborhoods were bought up at once for conversion into rental properties.

BlackRock’s chairman Larry Fink is on the board of the World Economic Forum, which until recently featured a controversial promotional video declaring “You will own nothing, and you’ll be happy.”

We all want a clean environment, and we want to preserve species biodiversity. But that includes human biodiversity – acknowledging the rights of rural landowners and Indigenous peoples, the land’s natural stewards. The greatest threat to the land is not the people living on it but those well-heeled investors who swoop in to buy up the rights to it, financializing the earth for profit.

Not just private property but those public lands and infrastructure once known as “the commons” are now under threat. We face an existential moment in our economic history, in which accumulated private wealth is acquiring carte blanche control of the essentials of life. Whether that juggernaut can be stopped remains to be seen, but the first step in any defensive action is to be aware of the threat at our doorsteps.

A month before the 2021 United Nations Climate Change Conference (known as COP26) kicked off in Scotland, a new asset class was launched by the New York Stock Exchange that will “open up a new feeding ground for predatory Wall Street banks and financial institutions that will allow them to dominate not just the human economy, but the entire natural world.” So writes Whitney Webb in an article titled “Wall Street’s Takeover of Nature Advances with Launch of New Asset Class”:

For weeks, conservative Democrats in Congress have prevented the passage of the Build Back Better Act and the Freedom to Vote Act. Congressmember Ilhan Omar of Minnesota has been a vocal critic of Senators Joe Manchin of West Virginia and Kyrsten Sinema of Arizona, who have stalled the bills and forced President Biden to radically scale back the price tag of his agenda. “All Democrats are essentially on board,” Omar says, “except for these two, who are essentially doing the bidding of Big Pharma, Big Oil and Wall Street.” The Build Back Better Act, which began at $3.5 trillion when Biden introduced the bill, has reportedly been lowered to half the original amount due to resistance in Congress. Progressive initiatives that are in danger of being dropped include free community college, extended paid family leave and lower prescription drug prices.

TRANSCRIPT

This is a rush transcript. Copy may not be in its final form.

AMYGOODMAN: We begin today’s show looking at how key elements of President Biden’s domestic agenda are in jeopardy. On Wednesday, Senate Republicans blocked passage of the Freedom to Vote Act. Not a single Republican supported the bill. Senate Democrats could pass the sweeping voting rights legislation, but only if they voted to end the filibuster. However, two conservative Democrats — Senators Joe Manchin of West Virginia and Kyrsten Sinema of Arizona — oppose doing so.

Manchin and Sinema have also forced President Biden to radically scale back the Build Back Better Act, which began as a proposed $3.5 trillion spending bill over 10 years to vastly expand the social safety net and combat the climate crisis. Biden has reportedly lowered the topline price tag on the package to $1.75 trillion — half the original bill. Manchin wants the bill to be even smaller, pushing for $1.5 trillion over 10 years. Initiatives that could be dropped include free community college, extended paid family leave and an initiative to lower prescription drug prices. Manchin has also demanded Democrats strip out funding for the Clean Electricity Performance Program, a critical climate initiative to replace coal- and gas-fired power plants with renewable energy sources. Democrats are also moving away from proposals to increase the tax rate on the rich and corporations.

On Wednesday, Mother Jones magazine reported Manchin has been privately telling associates he’s considering leaving the Democratic Party and declaring himself a, quote, “American Independent” if he doesn’t get his way in slashing the size of the Build Back Better Act. Manchin rejected the report.

We go now to Washington, where we’re joined by Congressmember Ilhan Omar of Minnesota, who’s been a vocal critic of Senator Manchin’s efforts to obstruct passage of both the Build Back Better Act and the Freedom to Vote Act. After the voting rights bill failed in the Senate Wednesday, Congressmember Omar tweeted, “The filibuster—and the Democratic Senators who continue to uphold it—are killing our democracy.”

Congressmember Ilhan Omar, welcome back to Democracy Now!

REP. ILHANOMAR: Great to be with you, Amy.

AMYGOODMAN: You have to wonder at this point, when we talk about “President Joe,” if we’re talking about President Joe Biden or President Joe Manchin. He is one senator but holds so much power. Though the $3.5 trillion spending — the $3.5 trillion spending bill, talking about scaling it back to $1.7 trillion, that’s only a bit over the $1.5 trillion that this one senator has demanded. Can you talk about the significance of his power and also how it is related to him being the number one recipient of oil, gas and coal money in the U.S. Senate?

REP. ILHANOMAR: Well, thank you so much, Amy, for having me.

I think it is really important for people to understand just the level of obstruction that this one senator is causing to the agenda of the president and everything we are trying to accomplish as Democrats on behalf of the American people. You know, so, for so long people have said, “Washington is corrupt. You know, they’re not watching out for the interests of the people.” And what’s playing out right now with these senators really is giving people a front-row seat to what they have always talked about.

And we have to get past this. We have to be able to bring these senators on board. We have to be able to accomplish this agenda, because, truly, what is on the line? It’s investment in child care. It’s investment in expanding paid family leave. It’s an agenda to try to get vision, dental and hearing paid for for seniors. It’s trying to address the climate crisis so that there is something for the future generation. It’s, you know, trying to do everything that we can so that people in our communities can feel the impact of their government. And as you said, you know, all Democrats are essentially on board, except for these two, who are essentially doing the bidding of Big Pharma, Big Oil and Wall Street.

NERMEENSHAIKH: Representative Omar, how do you think that these senators — you said it’s essential to bring them on board. What can Democrats do to persuade them to get on board?

REP. ILHANOMAR: We have to continue talking. You know, this agenda is too big to fail. We’ve made these promises to the American people for a really long time. Investment in child care, paid family leave, in home and community-based care, these are things that are not just going to help particular communities, but it will help all communities across this country. And if we do not continue to have this conversation to move them along so that we can get it done, then we will not only fail to get our agenda done, but we would have failed the American people.

AMYGOODMAN: Congressmember Omar, I wanted to continue on this issue of Senator Manchin’s power by talking about his business holdings in West Virginia. The intercept recently published a report headlined, “Joe Manchin’s Dirty Empire.” It says, quote, “For decades, Manchin has profited from a series of coal companies that he founded during the 1980s. His son, Joe Manchin IV, has since assumed leadership roles in the firms, and the senator says his ownership is held in a blind trust. Yet between the time he joined the Senate and today, Manchin has personally grossed more than $4.5 million from those firms, according to financial disclosures. He also holds stock options in Enersystems Inc., the larger of the two firms, valued between $1 and $5 million.” So, maybe this isn’t a matter so much of ideology, but, straightforward, the amount of money that he stands to make or lose based on this Build Back Better Act. He has demanded the stripping out of the section on renewable energy. Can you talk about this and if this is raised in dealing with him, and what it would mean if he did leave the Democratic Party? Or do you think it’s an empty threat?

REP. ILHANOMAR: I think it is important for these connections to be made, and certainly for his constituents to recognize this. You know, we have a representative democracy, where you elect someone to represent your interests, not the interests of corporations and not their own interests. This, to me, sounds like legalized corruption. And if it was happening, you know, anywhere else in the world, we would be appalled by it. But the fact that it continues to happen, not just with Manchin but so many others, you know, begs the question: How are we going to continue to have the kind of democracy that we can be proud of, and talk about transparency, accountability and ending corruption to other parts of the world, when we allow it to happen within our own country? You know, the devastation economically that is visible in West Virginia, when you talk about all kinds of measures, it’s the bottom of the 50 states almost always. And to have a senator that isn’t focusing on creating the kind of investments that will uplift the communities that he represents is something that we need to seriously address.

AMYGOODMAN: So, let’s talk about what’s in the act and what’s not in the act, and what are lines in the sand, if you will. I mean, you’ve got the proposed cuts being cutting free community college for two years, cutting the Clean Electricity Performance Program, reducing paid family leave — now at the federal level, there isn’t paid family leave, but it would go from 12 weeks to four weeks — child tax credit, funding for home care. Can you talk about those that are now threatened, but also what remains, like universal pre-K, like Medicare expansion, etc., and what you think is significant here, and how much power the Progressive Caucus has? You’re the largest caucus in Congress.

REP. ILHANOMAR: So, first of all, I just will say, you know, it’s not done until it’s done. Nothing has been agreed to by all parties, so I can’t really say what is in and what is out at the moment. You know, we’re obviously still negotiating. We’re obviously still having these conversations. Some of the things that you had mentioned would be some red lines for some of our members within the Progressive Caucus, and they have raised those concerns. And so, we’re still at the drawing board and trying to finalize a deal that can get the support of the Progressive Caucus and can have the support of these senators, so that we are able to actually pass this piece of legislation.

What we are arguing for is that four principles should be used by Congress in the final package. We want to make sure that there is — there are transformative investments, that whatever piece of legislation we end up voting on touches people’s lives immediately, that they provide universal benefits, and that they keep the president’s commitment to racial equity. And so, whether we end up cutting the duration of the investment or not, you know, we will see. But right now things are still up in the air, and conversations are still taking place. So, I wouldn’t say this is out, this is in, just yet.

NERMEENSHAIKH: Representative Omar, we’d like to move on now to the Freedom to Vote Act. On Wednesday, Senate Republicans blocked debate on the Freedom to Vote Act, and you tweeted in response, quote, “The filibuster—and the Democratic Senators who continue to uphold it—are killing our democracy.” Could you talk about what happened and elaborate on what you said?

REP. ILHANOMAR: Yeah. We know, obviously, that our democracy is under threat. And if we do not address the kind of challenges that are posed to our democracy with legislation, we are — you know, we are going to fail our democracy. And we’re seeing Democrats in the Senate not understand that urgency. We have these two senators that are beholden more to this filibuster, that is Senate procedure and not codified in our Constitution, that are willing to uphold that and not uphold the resiliency and health of our democracy so that it could continue to flourish.

NERMEENSHAIKH: And, Representative Omar, another issue on which you’ve been vocal has to do with the increasing reports of what’s being called modern-day slavery in Libya: the widespread abuse of migrants in detention centers there. You wrote in a press statement, quote, “The U.S. needs a comprehensive strategy to address the ongoing human trafficking and modern day slavery crisis in Libya.” Could you talk about what you know of what’s happening, and what strategy you’re proposing the U.S. pursue?

REP. ILHANOMAR: Yeah. Thank you so much for that question. What’s happening in Libya is truly heartbreaking. As someone who comes from one of the countries in Africa where people are being enslaved in Libya, I and so many others have, you know, personally been touched. We know family members, we know friends, we know people who are personally impacted in Libya. We have seen routine reports of rampant abuse, torture, sexual violence, extortion of migrants in Libya from sub-Saharan African countries. It is really painful that it is not getting the attention and response that it needs. And, you know, instead of welcoming thousands of refugees fleeing violence and instability, the Libyan Coast Guards hand migrants over to militias who systematically torture, rape, abuse and enslave them. The European Union is making it worse by turning away migrants and, instead, arming these same militias that are committing these abuses.

The United States hasn’t had a comprehensive strategy to engage and to address this ongoing human trafficking crisis and this modern-day slavery. I’ve met with representatives from United Nations orgs that are dealing with this situation. And what they’re asking for is for the United States to step up, for us to help create a strategy, and for us to have a conversation with the European Union, because, you know, what’s taking place in Libya is a human rights crisis. It’s a human tragedy. It’s not something that we should allow to happen today. And it is something that needs the attention of the United States and other countries, as well.

AMYGOODMAN: Two questions, one about vaccine equity in the world, what some call vaccine apartheid. As you heard in our headlines, you know, the FDA is quickly approving vaccines for children and also boosters to people as young as 40 years old. Can you talk about the issue of vaccine availability in the world? While the Western nations are massively vaccinating their populations, in some places, particularly the continent you come from, from Africa, we’re looking at 1% and 2% and 5% of the population vaccinated, not because of choice, but because they don’t have access. While President Biden has supported the TRIPS waiver at the WTO, it’s a question of expending political capital to force other countries, like Germany and Britain, where the pharmaceutical companies are based that are making billions, do the same. Can you talk about what has to be done?

REP. ILHANOMAR: Yes, you’re right. We do have to spend political capital on this. This is, you know, a catastrophe. Vaccine apartheid is real. There are so many people across the world who are celebrating, you know, 5%, 10%, 20% vaccination, because that is the best that they can do with the limited resources that they have, while their wealthy counterparts are not doing their part, and providing not just an overall vaccination, but even boosters, as you said, which is happening here in the United States, and which will rapidly expand. Booster shots are not just going to be available for those who are at risk and older than 40. We’re going to provide it to everyone soon. And we are even providing vaccinations to young children now, when so many people around the world can’t even vaccinate their most vulnerable members of their communities.

So, yes, it is the right thing for the United States to spend its political capital, to say, “Let’s come together as a world and address this pandemic,” that doesn’t recognize boundaries and doesn’t recognize that someone is wealthy and someone is poor. Everyone has suffered from it. And, you know, as you know, I’ve lost my father to COVID-19. There are so many people who have been tragically touched by this pandemic. And we are now at a moment where we can help those within our borders and extend that aid to others in different countries.

AMYGOODMAN: And our deep condolences again on the loss of your father. Do you think that the U.S. should be requiring Moderna to release its recipe, given how heavily subsidized, publicly subsidized their research was?

REP. ILHANOMAR: Yes. And I’ve said that from the start. But at this moment, Amy, it is going to take a long time for that recipe to be utilized, and a lot of these countries don’t have those resources. So what we’re asking for is for the excess amounts that exist in some of the wealthiest countries, including ours here in the United States, to be donated and for that transfer to happen in an urgent matter to every corner of the world.

AMYGOODMAN: Finally, Congressmember Omar, you’re calling on President Biden to intervene in the construction of the Enbridge Line 3 pipeline in your state, in northern Minnesota, and to protect Indigenous sovereignty and the environment. In this last week, more than 600 people, overwhelmingly Indigenous, were arrested in Washington, D.C., in this Native American-led climate protest. You also have The Guardian newspaper revealing that Enbridge paid Minnesota police $2.4 million in reimbursements, all costs tied to the arrests and surveillance of hundreds of water protectors. Can you talk about this and what needs to happen now?

REP. ILHANOMAR: The president has to intervene. I have called on the president to intervene to stop this pipeline. Just yesterday, the president addressed our Boundary Waters and talked about tribal sovereignty and treaty rights. And it was astonishing, really, to hear these statements coming in regards to the wilderness and the Boundary Waters, when we are not using a similar statement in regards to Line 3 and what it means for the northern — for northern Minnesota and our Indigenous brothers and sisters, and what it means for their tribal sovereignty, what it means for the treaty rights, which are supreme laws in this land, and what it means for their livelihood, what it means in regards to their wildlife. I mean, the Anishinaabe communities in Minnesota say it is their culture, that they were told to go where food grows on water, and wild rice is their life. It’s their culture. It’s their tradition. It’s basically their existence. And we don’t have this president addressing the urgency of stopping this pipeline, that will essentially destroy their land and ultimately pollute everybody that has access to the Mississippi.

AMYGOODMAN: Well, Congressmember Ilhan Omar, we want to thank you so much for being with us, Minnesota congressmember representing the 5th Congressional District. Her memoir is titled This Is What America Looks Like: My Journey from Refugee to Congresswoman. You can go to democracynow.org to see our extended interview with Congressmember Omar about her memoir.

And a quick correction in our Guantánamo Bay headline: Asadullah Haroon Gul is the first prisoner in 10 years, not two years, to win a habeas corpus argument. He is the Guantánamo prisoner.

Next up, we look at Senator Joe Manchin’s “dirty empire” in West Virginia. Stay with us.

It seems that everywhere you look in America you see homelessness. Rarely, though, do you hear that Wall Street is helping cause it.

Thirty-two percent seems to be the magic threshold, according to new research funded by the real estate listing company Zillow. When neighborhoods hit rent rates in excess of 32 percent of neighborhood income, homelessness explodes. And we’re seeing it play out right in front of us in cities across America because a handful of Wall Street billionaires want to make a killing.

Housing prices have gone out of control since my dad bought his house in 1957 when I was six years old. He got a Veteran’s Administration-subsidized loan and picked up the brand-new 3-bedroom ranch house my brothers and I grew up in, in suburban south Lansing, Michigan. It cost him $13,000, which was about twice what he made every year working a good union job in a tool-and-die shop.

When my dad bought his home in the 1950s the median price of a single-family house was around 2.2 times the median American family income. Today, the Fed says, the median house sells for $374,900 while the median American income is $35,805 — a ratio of more than ten-to-one between housing costs and annual income.

As the Zillow study notes:

“Across the country, the rent burden already exceeds the 32 percent [of median income] threshold in 100 of the 386 markets included in this analysis….”

And wherever housing prices become more than three times annual income, homelessness stalks like the grim reaper.

And it’s true that we haven’t been building enough new housing, particularly low income housing, as 40 years of Reaganism have driven down wages and income for working class people relative to all of their expenses.

But that’s not what’s been uniquely driving housing prices into the stratosphere — and, as a consequence, the crisis in homelessness — over the past decade. You can thank speculation for much of that.

As the Zillow-funded study noted: “This research demonstrates that the homeless population climbs faster when rent affordability — the share of income people spend on rent — crosses certain thresholds. In many areas beyond those thresholds, even modest rent increases can push thousands more Americans into homelessness.”

“Unusual high appreciation of the aforementioned urban centers is due to the ever growing influx of foreign buyers — mostly wealthy Chinese — who view American residential real estate as the safest investment commodity. … According to a National Realtors Association survey, the Chinese spent $22 billion on U.S. housing in 12 months through March 2014…. [Other foreign buyers include primarily include] Canadians, British, Indians and Mexicans.”

But foreign investment has been down for the past few years; what’s taken over and is really driving home prices today are massive, multi-billion-dollar funds that sweep into neighborhoods and buy everything available, bidding against families and driving up housing prices.

As noted in a Wall Street Journal article titled “Meet Your New Landlord: Wall Street,” in just one suburb (Spring Hill) of Nashville, “In all of Spring Hill, four firms … own nearly 700 houses … [which] amounts to about 5% of all the houses in town.”

This is the tiniest tip of the iceberg.

“On the first Tuesday of each month,” notes the Journal article about a similar phenomenon in Atlanta, investors “toted duffels stuffed with millions of dollars in cashier’s checks made out in various denominations so they wouldn’t have to interrupt their buying spree with trips to the bank…”

The same thing is happening in cities and suburbs all across America; the investment goliaths use fine-tuned computer algorithms to sniff out houses they can turn into rental properties, making over-market and unbeatable cash bids often within minutes of a house hitting the market.

After stripping neighborhoods of homes families can buy, they then begin raising rents as far as the market will bear.

In the Nashville suburb of Spring Hill, the vice-mayor, Bruce Hull, told the Journal you used to be able to rent “a three bedroom, two bath house for $1,000 a month.” Today, the Journal notes, “The average rent for 148 single-family homes in Spring Hill owned by the big four [Wall Street investor] landlords was about $1,773 a month…”

Ryan Dezember, in his book Underwater: How Our American Dream of Homeownership Became a Nightmare, describes the story of a family trying to buy a home in Phoenix. Every time they entered a bid, they were outbid instantly, the price rising over and over, until finally the family’s father threw in the towel.

“Jacobs was bewildered,” writes Dezember. “Who was this aggressive bidder?”

Turns out it was Blackstone Group, now the world’s largest real estate investor. At the time they were buying $150 million worth of American houses every week, trying to spend over $10 billion. And that’s just a drop in the overall bucket.

In 2018, corporations bought 1 out of every 10 homes sold in America, according to Dezember, noting that, “Between 2006 and 2016, when the homeownership rate fell to its lowest level in fifty years, the number of renters grew by about a quarter.”

This all really took off around a decade ago, when Morgan Stanley published a 2011 report titled “The Rentership Society,” arguing that snapping up houses and renting them back to people who otherwise would have wanted to buy them could be the newest and hottest investment opportunity for Wall Street’s billionaires and their funds.

Turns out, Morgan Stanley was right. Warren Buffett, KKR and The Carlyle Group have all jumped into residential real estate, along with hundreds of smaller investment groups, and the National Home Rental Council has emerged as the industry’s premiere lobbying group, working to block rent control legislation and other efforts to control the industry.

As John Husing, the owner of Economics and Politics Inc., told The Tennessean newspaper, “What you have are neighborhoods that are essentially unregulated apartment houses. It could be disastrous for the city.”

Meanwhile, as unionization levels here remain among the lowest in the developed world, Reagan’s ongoing war on working people continues to wipe out America’s families.

At the same time that housing prices, both to purchase and to rent, are being driven through the roof by foreign and Wall Street investors, a new survey published this month by NPR, the Robert Wood Johnson Foundation and the Harvard TH Chan School of Public Health found that American families are in crisis.

“Thirty-eight percent (38%) of [all] households across the nation report facing serious financial problems in the past few months.

“There is a sharp income divide in serious financial problems, as 59% of those with annual incomes below $50,000 report facing serious financial problems in the past few months, compared with 18% of households with annual incomes of $50,000 or more.

“These serious financial problems are cited despite 67% of households reporting that in the past few months, they have received financial assistance from the government.

“Another significant problem for many U.S. households is losing their savings during the COVID-19 outbreak. Nineteen percent (19%) of U.S. households report losing all of their savings during the COVID-19 outbreak and not currently having any savings to fall back on.

“At the time the Centers for Disease Control and Prevention’s (CDC) eviction ban expired, 27% of renters nationally reported serious problems paying their rent in the past few months.”

These are not separate issues, and they are driving an explosion in homelessness.

“Communities where people spend more than 32 percent of their income on rent can expect a more rapid increase in homelessness.

“Income growth has not kept pace with rents, leading to an affordability crunch with cascading effects that, for people on the bottom economic rung, increases the risk of homelessness.

“The areas that are most vulnerable to rising rents, unaffordability and poverty hold 15 percent of the U.S. population — and 47 percent of people experiencing homelessness.”

The Zillow study makes grim reading and is worth checking out. In community after community, when rent prices exceed 32 percent of median home income, homeless explodes. It’s measurable, predictable, and is destroying what’s left of the American working class, particularly people of color.

The loss of affordable homes also locks otherwise middle class families out of the traditional way wealth is accumulated — through home ownership: over 61% of all American middle-income family wealth is their home’s equity. And as families are priced out of ownership and forced to rent, they become more vulnerable to homelessness.

Housing is one of the primary essentials of life. Nobody in America should be without it, and for society to work, housing costs must track incomes in a way that makes housing both available and affordable.

If ever there was a time to solve to this problem — and regulate corporate and foreign investment in American single-family housing — it’s now.

“Polarization” is the word most associated with the positions of the Republicans and Democrats in Congress. The mass media and the commentators never tire of this focus, in part because such clashes create the flashes conducive to daily coverage.

The quiet harmony between the two parties created by the omnipresent power of Big Business and other powerful single-issue lobbyists is often the status quo. That’s why there are so few changes in this country’s politics.

In many cases, the similarities of both major parties are tied to the fundamental concentration of power by the few over the many. In short, the two parties regularly agree on anti-democratic abuses of power. Granted, there are always a few exceptions among the rank & file. Here are some areas of Republican and Democrat concurrence:

1. The Duopoly shares the same stage on a militaristic, imperial foreign policy and massive unaudited military budgets. Just a couple of weeks ago, the Pentagon budget was voted out of a House committee by the Democrats and the GOP with $24 billion MORE than what President Biden asked for from Congress. Neither party does much of anything to curtail the huge waste, fraud, and abuse of corporate military contractors, or the Pentagon’s violation of federal law since 1992 requiring annual auditable data on DOD spending be provided to Congress, the president, and the public.

2. Both Parties allow unconstitutional wars violating federal laws and international treaties that we signed onto long ago, including restrictions on the use of force under the United Nations Charter.